Are you preparing to take the EA exam? This comprehensive three-part exam, facilitated by Prometric Test Centers on behalf of the IRS, is the first step for professionals aiming to specialize in tax law and representation practices.

But passing it, not so simple.

If you’re feeling overwhelmed by the thought of reading all 33 pages of the Treasury Department Regulations Governing Practice before Circular No. 230 to understand more about the Enrolled Agent exam questions? Don’t worry—you don’t have to wade.

I’ve broken it down into simpler, more digestible parts. Here’s a guide to help you prepare effectively without getting bogged down by the details.

Key Takeaways

- Exam Structure and Format: The exam consists of three parts, each containing 100 multiple-choice questions and allowing 3.5 hours for completion plus an additional 30 minutes for a mandatory computer tutorial. Questions vary in format, including direct queries, incomplete sentences, and “all of the following, except” types.

- Confidentiality of Exam Questions: Official EA exam questions are not released to the public, which means accurate past exam questions are not easily found online. This maintains the integrity and security of the exam content.

- Advantages of EA Prep Programs: Engaging with a top-rated EA prep program can provide a realistic test experience and help build confidence. These programs offer practice exams and mock tests that are invaluable for understanding the exam’s demands and improving time management skills under simulated conditions.

All About Enrolled Agent Exam Questions

The EA exam, also known as the IRS Special Enrollment Examination (SEE), is crafted to evaluate a candidate’s comprehension and application skills across a broad spectrum of tax-related topics. It covers individual taxation, business taxation, and representation practices, thoroughly testing your ability to navigate complex tax laws.

Key Areas Covered in the EA Exam

- Individual Taxation: This section focuses on diverse income types, various tax credits including the American Opportunity Credit, and nuances such as the Net Investment Income Tax and the implications of the Affordable Care Act.

- Business Taxation: This part requires a solid understanding of business entities, Schedule C filings, and other pertinent tax issues affecting businesses.

- Representation, Practices, and Procedures: This section tests knowledge of dealing with the IRS, managing installment agreements, conducting background checks, and other aspects of tax representation and procedures.

Special Enrollment Exam Format and Scoring

The EA exam is divided into three sections, each comprising 100 multiple-choice questions. Candidates have 3.5 hours to complete each section, with an additional 30 minutes allocated for a mandatory computer tutorial. The questions may be formatted as direct queries, incomplete sentences, or asking to select the correct answer from a list, often using the format “all of the following, except.”

Detailed Section Breakdown

- Part 1 – Individuals: Includes preliminary work with taxpayer data, income and assets, deductions and credits, taxation advice, and specialized returns.

- Part 2 – Businesses: Covers business entities, business financial information, and specialized returns.

- Part 3 – Representation, Practice, and Procedures: Focuses on practices and procedures, representation before the IRS, specific types of representation, and the completion of the filing process.

Availability of EA Exam Questions and Preparation Resources

One important aspect to consider while preparing for the Enrolled Agent (EA) Exam is the availability of official exam questions. The IRS does not release actual exam questions to the public, which means that you won’t find exact copies of past questions available online for free. This ensures the integrity and confidentiality of the exam content, making each testing experience unique and secure.

Why You Won’t Find Actual Exam Questions Online

Since the EA exam questions are kept confidential, any free resources claiming to offer actual exam questions should be approached with caution. These are likely not accurate and may not provide a reliable means of preparation. The secrecy of the questions helps maintain the exam’s standard and prevents any unfair advantage.

Using Official Prep Resources

For those seeking to prepare thoroughly, the best approach is to engage with trusted and reputable preparation resources. Many professional education platforms offer practice questions that are crafted to mimic the style and rigor of the actual exam. These practice materials are designed by experts familiar with the EA exam’s focus and format.

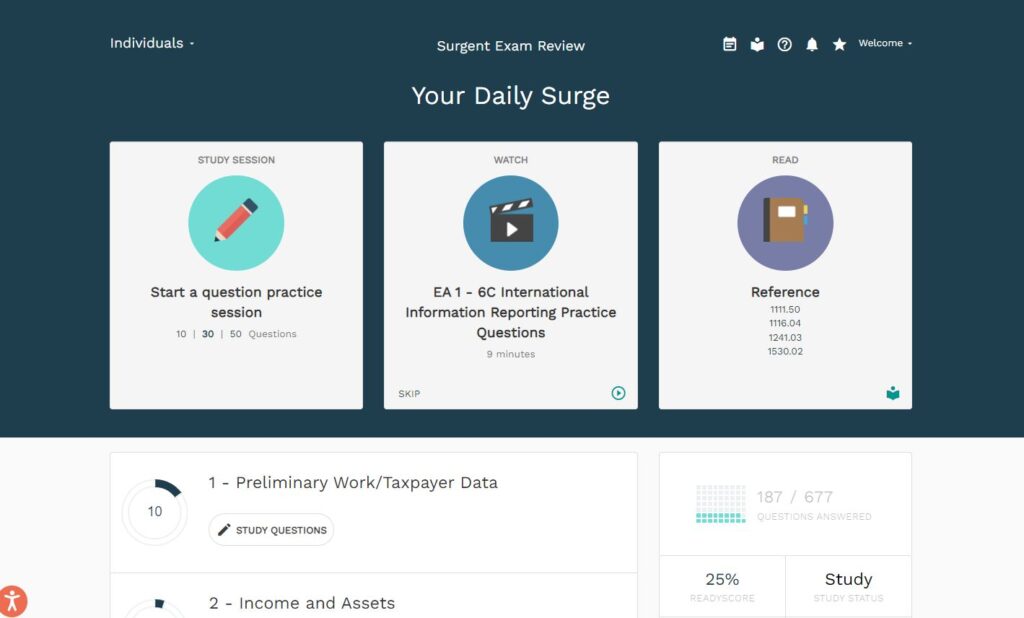

Take a Test Drive of One of the Best EA Prep Programs

To get a realistic sense of what to expect and to evaluate your readiness for the actual exam, you can take a test drive of one of the best EA prep courses. These programs often offer a mix of practice questions, mock exams, and comprehensive study materials tailored to cover all the key areas of the EA exam. Taking a test drive of such programs not only prepares you for the type of questions to expect but also helps build confidence and improve time management skills under exam conditions.

“I used Surgent. I passed each part first try by just doing the multiple choice questions and reading the explanations. Just find what works for you and allows you to understand the content.”

u/DocShocks2

Enrolled Agent Exam Questions for Test Candidates

Using some of the IRS-released practice questions, I’ve created a few of my own so that aspiring Enrolled Agents can see how they are structured.

Education Credits for Recently Married Taxpayers

Question: A couple married late in the year on November 30. In that year, one spouse enrolled in an accredited college to advance his career and received a Form 1098-T for tuition paid. The other spouse, with an income of $45,000, covered these educational expenses. They did not have any other income sources during the year. What is the appropriate way to claim an education credit under these circumstances?

- A) They need to file jointly to be eligible for any education credit.

- B) Their combined income is too high to qualify for any education credit.

- C) Only the spouse who incurred the education expenses directly can claim the credit.

- D) The spouse who paid for the education should separately claim nonqualified education expenses using Form 8863.

Claiming the American Opportunity Credit for Dependent Students

Question: A taxpayer supports a child under 24 who is a full-time college student in their sophomore year. The student incurred $8,000 in tuition and $4,000 in room and board expenses, partially offset by a $5,000 scholarship designated for tuition and an additional $2,500 scholarship for any college expense. The taxpayer paid the remaining tuition amount of $4,500. How should the American Opportunity credit be claimed?

- A) The student should claim $3,000 as tuition expenses on their own return after reporting the extra $2,500 scholarship as income.

- B) The taxpayer should claim $3,000 for tuition expenses on their return after the student declares the $2,500 scholarship as income.

- C) The taxpayer can claim $3,000 for tuition expenses on their return without reporting the additional $2,500 scholarship as income by either party.

- D) The taxpayer should claim $3,000 for tuition expenses on their return and report the additional $2,500 scholarship as income.

Understanding Form 1095-A and Premium Tax Credits

Question: Which statement accurately describes the use of Form 1095-A, Health Insurance Marketplace Statement?

- A) Form 1095-A is not required to fill out Form 8962, Premium Tax Credit, for reconciling advance payments or claiming the premium tax credit.

- B) Form 1095-A is issued to taxpayers who have employer-sponsored insurance throughout the year to help complete Form 8962.

- C) Taxpayers use Form 1095-A to fill out Form 8962, Premium Tax Credit, for reconciling advance payments of the premium tax credit or to claim it on their tax returns.

- D) Form 1095-A must be attached directly to the tax return to reconcile or claim any premium tax credits.

Eligibility and Use of Form 8995 for QBI Deduction

Question: Who should use Form 8995, Qualified Business Income Deduction Simplified Computation?

- A) Corporations are advised to use Form 8995 to apply for the QBI deduction on their corporate tax returns.

- B) The IRS provides Form 8995 directly to taxpayers identified as eligible for the QBI deduction.

- C) An individual with qualified business income, whose taxable income is below the set threshold, should utilize Form 8995 to claim the QBI deduction.

- D) Partnerships must attach Form 8995 to their tax returns to claim the QBI deduction.

Correct Answers to the Example Enrolled Agent Exam Questions

- A

- B

- C

- C

Final Thoughts

Successfully navigating the EA exam requires a thorough understanding of tax laws and representation procedures. This guide has detailed the structure and content of the exam, emphasizing the importance of high-quality preparation resources and robust EA prep programs. By strategically utilizing these tools, you can enhance your performance, manage your time effectively, and increase your confidence. Equip yourself with the right knowledge and resources to ace the EA exam and advance your career as an Enrolled Agent.

FAQ

The Enrolled Agent exam consists of three types of multiple-choice questions: direct questions, incomplete sentences, and all-of-the-following-except questions. Preparation should include understanding the format and practicing with sample questions that mimic these types. Utilizing EA prep courses and reviewing IRS publications and tax codes related to the exam content are also effective strategies.

The Enrolled Agent exam is offered during three testing windows each year. These windows are from May 1 to June 30, September 1 to October 31, and November 1 to December 31. Testing centers are closed outside of these periods.

Yes, if you do not pass a section of the EA exam, you can retake it. However, you must wait a mandatory cooling-off period of 24 hours before scheduling your next attempt, and you can only attempt each part a maximum of four times during a single testing window.

The EA exam covers three main areas: Part 1 focuses on Individual Taxation, Part 2 on Business Taxation, and Part 3 on Representation, Practices, and Procedures. Each part consists of 100 multiple-choice questions, evenly weighted across various subtopics pertinent to each section.

Each section of the Enrolled Agent exam is independently scored on a scale from 40 to 130. A score of 105 or higher is required to pass each part. The score is based on the total number of correct answers, so it is advantageous for candidates to answer every question, as there is no penalty for guessing.

A PTIN is required to register for the Enrolled Agent exam. Candidates must obtain a PTIN from the IRS, which involves filling out an online application on the IRS website. Once issued, the PTIN allows you to officially schedule and take the EA exam.

The term Internal Revenue Service Key typically refers to specific guidelines, codes, or procedures established by the IRS to ensure compliance and facilitate the administration of tax laws. It can also relate to digital access keys or authentication methods used for secure communication with the IRS’s online services. This might include access for filing returns, checking the status of refunds, or communicating securely with IRS representatives.