If you think being a mortgage loan originator is mostly about paperwork and calculators, you’re only seeing the highlight reel. The real job happens somewhere between a borrower saying “Oh, I forgot to mention…” and an underwriter asking a very specific follow-up question three days before closing.

On paper, the role looks straightforward: collect financial information, submit loan applications, and move files through the system. In reality, mortgage loan originators operate at the intersection of finance, regulation, and human decision-making.

Before deciding whether this career path makes sense, it’s worth understanding the actual mortgage loan originator skills the job demands, and how different they are from what most people expect.

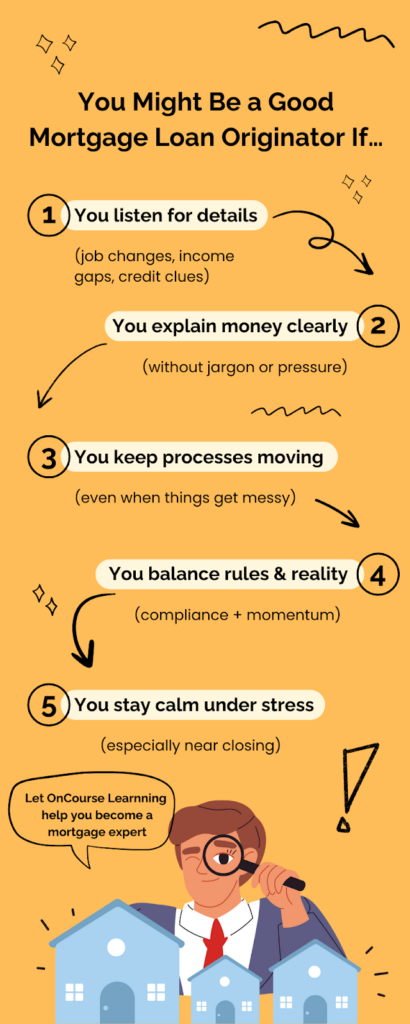

You Might Make a Good Mortgage Loan Originator If…

- You catch important details when people talk, especially around income, credit, or job changes—and know when to ask follow-up questions.

- You can explain financial concepts simply, helping people understand loan options without overwhelming them.

- You stay organized under pressure, even when multiple loan applications and loan process timelines are moving at once.

- You respect rules without slowing everything down, balancing compliance with a smooth borrower experience.

- You stay calm when others are stressed, offering steady guidance as market conditions or deadlines shift within the mortgage industry.

The Mortgage Loan Originator’s Role, Explained

Mortgage loan originators, sometimes called mortgage loan officers, work for banks, credit unions, and mortgage companies to guide prospective borrowers through the loan application process. They help clients navigate home financing, coordinate with loan underwriters, and ensure loan origination complies with federal and state regulations.

While commercial loan officers may focus on business lending, mortgage loan originators concentrate on residential mortgage loans, housing demand, and borrower-specific risk factors like credit checks, debt ratios, and employment stability.

Mortgage Loan Originator Skills That Actually Matter

Translating Risk Into Clear Choices

One of the most critical skills mortgage loan originators develop is the ability to explain complex financial concepts without overwhelming clients. Borrowers rarely struggle because they lack intelligence; they struggle because loan terms, credit intermediation, and underwriting rules aren’t intuitive.

Strong loan originators help clients understand how credit, income, and loan amount interact, turning abstract financial information into clear next steps. This is how trust is established early in the process.

Listening as Risk Detection (Not Customer Service)

Most people think listening is a customer service skill. In mortgage lending, it’s a risk-detection skill.

Many Americans struggle to cover even modest unexpected expenses, according to the Federal Reserve’s Survey of Household Economics and Decisionmaking, which highlights why loan officers’ ability to listen closely and explain financial details can make a real difference in guiding borrowers through decisions under pressure.

Mortgage loan originators spend hours speaking with prospective borrowers about income, employment history, credit issues, and past financial decisions. The most effective loan officers don’t just record answers—they listen for inconsistencies, omissions, and red flags that could derail the loan application process.

For example, when borrowers casually mention:

- A recent job change

- Irregular income

- A past credit issue they “forgot” to include

A skilled loan originator knows these details matter long before underwriting begins. By listening closely, mortgage loan officers can ask clarifying questions early, request the right documentation, and prevent avoidable delays once the file reaches loan underwriters.

This kind of listening also helps loan originators explain complex financial concepts more accurately. When loan officers understand why a borrower is nervous, confused, or resistant, they can tailor explanations about credit checks, loan amounts, or underwriting conditions in a way that actually lands.

Orchestrating the Loan Application Process

The loan application process doesn’t move in a straight line. Mortgage loan officers must manage documentation, timelines, and borrower expectations while coordinating with loan underwriters behind the scenes.

This requires attention to detail and the ability to anticipate questions before they delay underwriting. Loan officers who succeed long-term don’t just submit loan applications—they shape them so underwriters can recommend approval efficiently and confidently.

Regulatory Awareness Without Freezing the Process

Mortgage lending operates under strict fair enforcement standards. Background checks, compliance reviews, and licensing rules are non-negotiable. The skill lies in maintaining accuracy without making the process time-consuming for clients.

Mortgage loan originators who balance compliance with momentum keep their license active, protect their employer, and reduce stress for borrowers navigating an already emotional process.

Relationship Management Across Professionals

Mortgage loan officers work with real estate agents, processors, underwriters, and other professionals across a financial institution. Building relationships isn’t about salesmanship—it’s about coordination.

Clear communication across these roles keeps transactions stable, especially when market conditions or housing demand create pressure on timelines.

Staying Grounded as Market Conditions Shift

Interest rates, underwriting standards, and housing demand fluctuate constantly. Mortgage loan originators must stay informed without overreacting.

Clients rely on loan officers to provide valuable insights grounded in current market conditions—not speculation. This steadiness helps borrowers make decisions they can sustain long after closing.

How to Become a Mortgage Loan Originator

- Meet Education and Eligibility Requirements: In most states, becoming a loan originator starts with a high school diploma. A bachelor’s degree is not required, though relevant experience in finance, real estate, or banking can be helpful.

- Complete Pre-Licensing Education: Aspiring loan originators must complete pre-licensing education through approved real estate education courses. This training covers federal mortgage law, ethics, and loan origination fundamentals and prepares candidates for the MLO exam.

- Pass the MLO Exam and Licensing Process: After completing pre-licensing education, candidates take the MLO exam and submit a licensing application. This process includes credit checks and a background check, and typically takes a few weeks, depending on the state.

Providers like one of my favorites, OnCourse Learning, offer state-specific training designed to meet licensing standards without assuming prior mortgage experience.

Final Thoughts

Mortgage loan originators don’t succeed because they push products or rush borrowers. They succeed because they know how to listen for what matters, translate financial risk into real choices, and keep complex processes moving without losing the human side of the transaction.

If you’re someone who values accuracy, clear communication, and problem-solving under pressure—and you don’t mind being the calmest person in a very stressful room—this can be a genuinely rewarding career path. Not because it’s easy, but because it matters.

And for the right person, guiding someone from uncertainty to closing day never really gets old.

FAQs

Loan officers need the ability to explain complex financial concepts, manage detailed loan applications, maintain attention to detail for compliance, and build trust with borrowers and other professionals throughout the mortgage process.

The 5 C’s are credit, capacity, capital, collateral, and conditions. Mortgage loan originators use these factors to help underwriters evaluate borrower risk and make informed lending decisions.

The 3-7-3 rule refers to regulatory timing requirements: loan estimates must be delivered within three business days, certain waiting periods must be observed before closing, and closing disclosures must be provided at least three days before finalization.

Pay varies significantly by region, employer, and market conditions. Many mortgage loan originators earn a base salary plus commission, with total compensation increasing as experience and client volume grow.

For most candidates, completing pre-licensing education, passing the MLO exam, and finishing the licensing application process takes a few weeks to a few months, depending on state requirements and individual pacing.