If you’re prepping for the bar exam, there’s a good chance you’re not working full-time—or at all. You’re studying long hours, bar review fees are piling up, and you might even be relocating for the exam itself. All of that costs money. And if you’re not financially backed by family or sitting on a pile of savings, you might be wondering how you’re supposed to pay for any of it.

90% of law students use financial aid to fund their education, and one common type of that funding is bar exam loans.

But what are they? And are bar loans the right choice for you?

Let’s break down what bar exam loans are, how they differ from regular student loans, what to expect during the bar loan application process, and how to decide if one is right for you.

Key Takeaways

- Bar Loans Are Private: These loans are not part of federal aid and are offered by private lenders to cover bar exam-related expenses.

- You Can Use Funds Flexibly: Bar loan funds go directly to you and can cover everything from prep course fees to rent and groceries.

- Credit Matters: Since bar loans are not need-based, they require a solid credit score or a co-signer for approval.

- Compare Before You Borrow: Look at interest rates, origination fees, and repayment terms to find the best deal for your situation.

- Only Borrow What You Need: It can be tempting to take the full amount, but limiting your loan keeps your future payments more manageable.

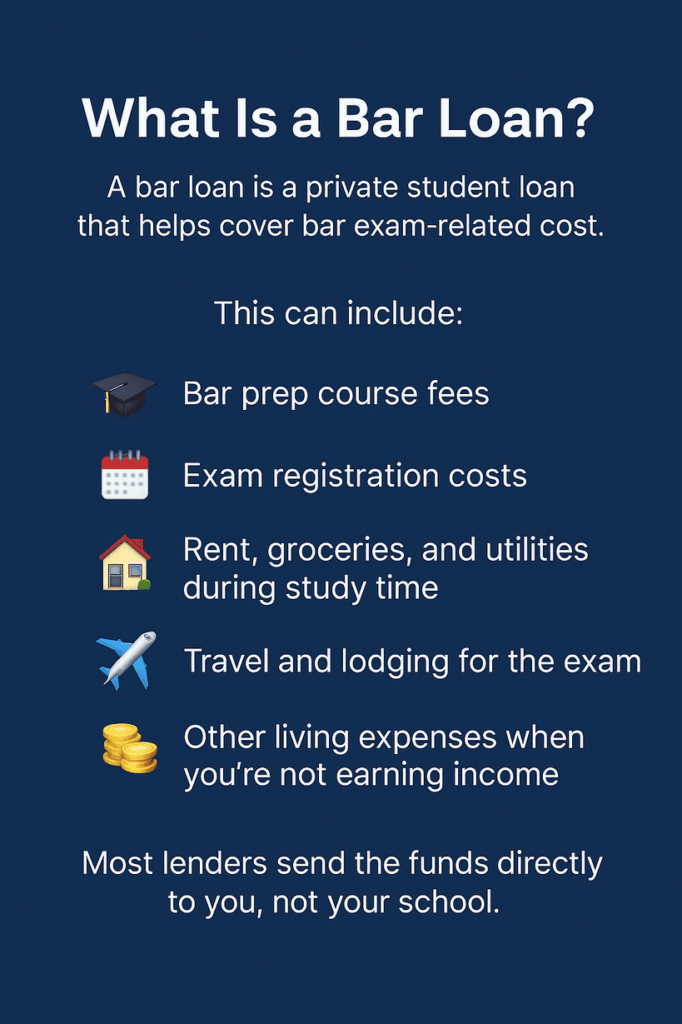

What Is a Bar Loan?

A bar study loan is a private loan that helps cover bar exam-related expenses. They’re not federal loans, and they’re not part of your academic year financial aid. Instead, they’re a specific kind of private student loan offered by banks and lenders to assist graduating law students in covering costs tied directly to the bar exam.

This can include:

- Bar prep course fees

- Exam registration costs

- Rent, groceries, and utilities during study time

- Travel and lodging for the exam

- Other living expenses when you’re not earning income

Most lenders send the bar loan funds directly to you, not your school. That makes it flexible, but it also means the responsibility is entirely yours.

Who Can Apply for a Bar Loan?

Bar loans are typically available to law students who are in their final year or have recently graduated from an ABA-accredited law school. While each lender is a little different, most have requirements like:

- Being enrolled in or graduating from law school

- Taking the bar exam within 12 months

- U.S. citizenship or permanent residency

- Passing a credit check (or having a co-signer)

Keep in mind that credit approval is an essential part of the process. If your credit isn’t great, you’ll likely need someone with a stronger credit history to co-sign.

How to Apply for a Bar Loan

The bar loan application process is usually done online and takes less than an hour if your paperwork is ready. Here’s a step-by-step of what that usually looks like:

Step 1: Research Your Options

Not all bar loans are created equal. Look at a few different lenders, like Sallie Mae, Discover, or PNC Solution Loan, and compare interest rates, fees, and terms.

Step 2: Gather Your Documents

If you’re applying solo, you’ll likely need proof of enrollment or graduation, an ID, your Social Security number, and income information.

Step 3: Complete the Application

You’ll enter your personal and financial information and possibly your school details. If you’re applying with a co-signer, they’ll need to provide their information, too.

Step 4: Wait for Approval

Approval can happen quickly—sometimes the same day. Once approved, you’ll review the terms, sign electronically, and choose when you’d like the funds disbursed.

Key Terms to Understand

Before you take out a bar loan, there are a few terms you’ll want to understand fully. Here’s what to keep an eye on:

Interest Rates

Bar loans typically come with higher interest rates than federal loans. You’ll often see fixed or variable rates. A fixed rate stays the same over time, while a variable rate can change—sometimes a lot. Some lenders offer an interest rate discount if you set up autopay.

Origination Fees

Some lenders charge a percentage just to process the loan. Others don’t. Make sure to ask about origination fees up front.

Interest-Only Payments

Most bar loans don’t require full monthly payments while you’re in school or within a grace period. Some allow interest-only payments, which means you won’t pay down the loan balance yet, but you can avoid ballooning interest.

Pros and Cons of Taking a Bar Loan

Every loan comes with trade-offs, so let’s break down the good and not-so-good sides of bar study loans.

Pros

- Covers a financial gap during one of the most expensive times in law school

- Lets you focus entirely on studying instead of working

- Fast application and flexible fund use

- Helps cover things that federal loans often don’t

Cons

- Not part of the federal loan program, so no income-driven repayment plans or loan forgiveness

- Usually comes with a higher interest rate

- Requires good credit (or a co-signer)

- Adds to your overall debt load

When a Bar Loan Makes Sense

I’ll be honest—bar loans aren’t for everyone. But they can be incredibly helpful in specific situations. You might consider one if:

- You’ve used up your federal loans for the year

- You need to pay for a bar prep course or exam fees out of pocket

- You don’t have income lined up and need help covering rent or utilities

- You’re not eligible for other aid through your financial aid office

Just remember: a bar loan is debt. It’s worth taking only if it genuinely helps you stay afloat during bar prep—and if you’re confident you’ll be able to pay it back.

Are Bar Loans Worth It?

Here are some real-world experiences from students who either took out a bar loan themselves or have seen how it affected their peers.

“A friend of mine opened a new credit card with a zero-interest promotion for the first 12 or 24 months and used that to pay for living expenses during bar prep. Then paid it off once he started working in October.

I would caution against this method if you don’t have post-bar plans already in place because the interest does snowball pretty quickly if you’re unable to pay off the balance within the promotional period and missing payments can destroy your credit (and in some jurisdictions substantial credit card debt may delay admission to the bar).”

DJDrizzleDazzle

“Yes, unfortunately, I took out Sallie Mae. It was my only choice if I didn’t work during bar prep. If I could go back in time, I would not do this. I would have worked and studied part-time for the February bar. If you can work and study part-time, it might be worth it in the long run, even if you have to wait to take the test.”

Sunny_Horizons

“Took out a loan specifically for bar prep. The rates weren’t bad. Search for “bar loans” and research your options. Couldn’t have done it without it. Your focus should be on bar prep, not working unless you absolutely can’t avoid it.”

v_rose23

How to Save Money If You Take One

If you do take out a bar loan, there are ways to make it work better for your budget.

- Use only what you need: Just because you’re approved for $15,000 doesn’t mean you have to borrow all of it.

- Set up auto-pay: Many lenders offer an interest rate discount if you make automatic payments.

- Start interest-only payments early: If you can, pay the interest while you’re studying. It’ll save you money long-term.

- Avoid late fees: Stay on top of repayment dates, especially after any grace period ends.

Final Thoughts

The exam is stressful enough without money worries hanging over your head. A bar loan can help bridge the gap during bar prep, especially if you’re without income or facing a mountain of bar-related expenses. But it’s not free money—so be thoughtful, do your research, and know what you’re signing up for.

If you’re still unsure whether a bar loan is right for you, talk to your financial aid office, compare lender offers, and consider other options like temporary work, scholarships, or personal loans from family. The more informed you are, the better prepared you’ll be—not just for the bar exam, but for your financial future too.

FAQs

A bar exam loan is a private loan designed to help law students pay for costs related to the bar exam, like prep courses, exam fees, and living expenses.

You apply through a private lender, get approved based on credit, and receive funds directly. Repayment often begins after a grace period following graduation.

It can be if your credit is poor. Many students apply with a co-signer to improve their chances of credit approval and get better loan terms, like lower interest payments.

Yes—bad credit won’t stop you from taking the bar exam itself. It only affects your ability to get financing, like a bar loan.

You’ll need to be in your final year of law school or recently graduated, be a U.S. citizen or permanent resident, and meet credit or co-signer requirements.