The Auditing and Attestation (AUD) section of the CPA exam often emerges as a mixed bag of perceptions — some candidates find it deceptively easy, while others deem it particularly challenging.

Personally, I think it can be uniquely tricky.

EllAytch put it this way: “AUD was my easiest exam by a long shot, though I have no audit experience. The conceptual questions just worked better for my brain. Many people feel the opposite and prefer the calculation-heavy questions of the other exams. So it really just depends on how the content works in your brain!”

This is why I underscore the importance of thoroughly understanding what it entails. At the heart of the difficulty isn’t the audit material itself but the nuanced nature of the exam questions. Each question is crafted to test not just your knowledge but also your ability to apply it by carefully discerning what is being asked. This nuanced challenge demands your utmost attention and strategic thinking, making a deep dive into the AUD content more crucial than ever.

Let’s explore what the AUD exam section of the CPA exam includes (newest update) together. I’ve even included some first-hand accounts from CPA candidates who have taken the AUD exam recently.

Key Takeaways

- Broad Scope of Content: The AUD section encompasses a wide range of topics, including audit engagements, attestation engagements, and accounting and review service engagements, testing candidates on a broad spectrum of auditing and attestation principles and practices.

- Strategic Preparation is Key: Effective preparation for AUD goes beyond mere memorization, requiring a deep understanding of professional ethics, a thorough grasp of the audit process, and proficiency in technology and data analytics within the context of auditing.

- Detail-Oriented Approach to Questions: Success in the AUD section demands meticulous attention to the nuanced nature of exam questions, emphasizing the application of knowledge and critical thinking to choose the most appropriate answer among seemingly correct options.

- Emphasis on Professional Ethics and Skepticism: The AUD section places significant emphasis on ethics, independence, and professional responsibilities, highlighting the importance of integrity and public trust in the audit profession, along with a critical application of professional skepticism.

Core Insights into the AUD CPA Exam

The AUD CPA exam section will test you on a broad selection of topics related to auditing and attestation engagements.

Understanding the essence of these topics is crucial to passing the CPA AUD exam:

- Audit Engagements: These include financial statement audits, compliance audits, and audits integrated with an audit of financial statements.

- Attestation Engagements: This includes assertion-based examinations, direct examinations, and agreed-upon procedure engagements.

- Accounting and Review Service Engagements: Covers preparation, compilation, and review engagements.

The questions on the AUD CPA exam are a mixture of multiple-choice questions and task-based simulations (SIMS).

Content Areas and Weight Allocation

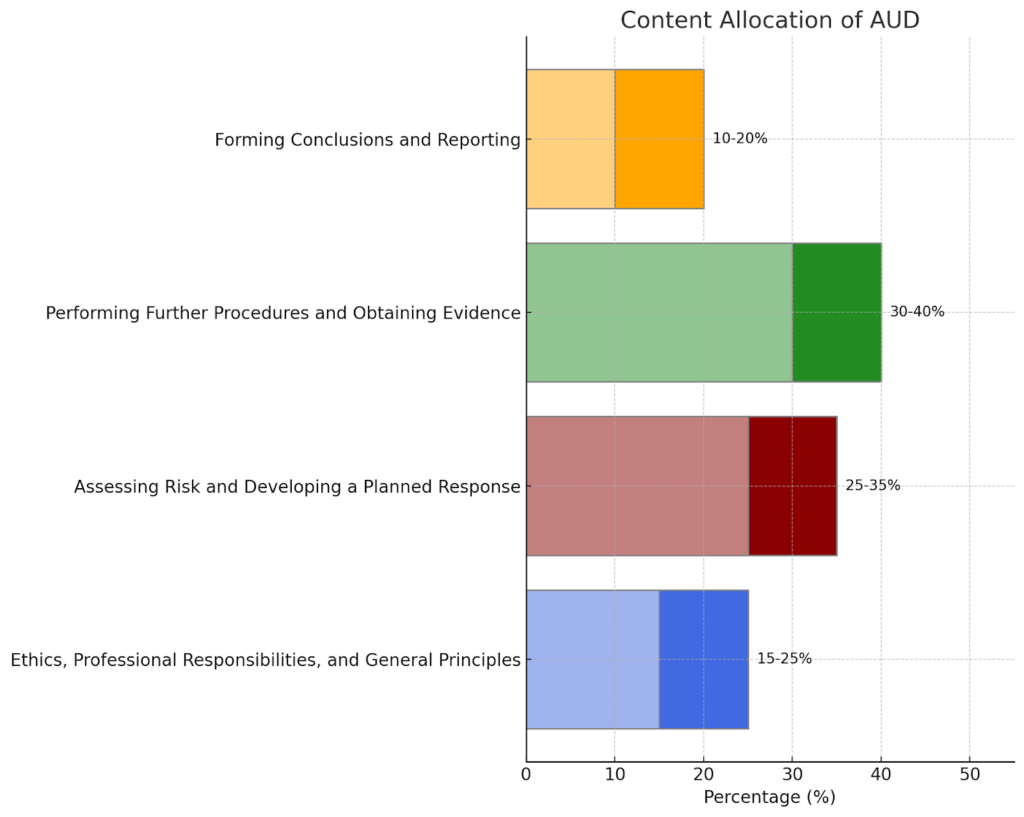

The AUD CPA Exam is meticulously organized into four main content areas:

- Ethics, Professional Responsibilities, and General Principles (15–25%)

- Ethics and independence, including the AICPA Code of Conduct and SEC, PCAOB, GAO, and DOL requirements.

- Professional skepticism and judgment.

- Engagement preconditions and documentation.

- Assessing Risk and Developing a Planned Response (25–35%)

- Engagement strategy and planning.

- Understanding entity and environment, including internal and external factors.

- Materiality and risk assessment.

- Performing Further Procedures and Obtaining Evidence (30–40%)

- Use of data analytics in obtaining evidence.

- Evidence collection techniques and sampling.

- Special audit considerations, such as accounting estimates and subsequent events.

- Forming Conclusions and Reporting (10–20%)

- Audit reporting principles.

- Attestation and review service reporting.

- Compliance and other reporting considerations.

Emphasis on Skills

The AUD section evaluates candidates across all skill levels of Bloom’s Taxonomy:

- Remembering and Understanding (30–40%): Fundamental concepts in auditing and attestation.

- Application (30–40%): Practical application of auditing principles.

- Analysis (15–25%) and Evaluation (5–15%): Higher-level interpretation and judgment.

“Failed it once because I underestimated it. There’s almost always 2 good answers for MCQ, and the English itself is just tricky.”

GaspChamber

What Makes the AUD CPA Exam Section Unique?

Although it is one of three Core CPA exam sections, to pass AUD, you’ll need to keep these considerations in mind:

Focus on Auditing Processes and Principles: AUD is dedicated to the intricacies of auditing, attestation, and the principles governing these areas, unlike sections that are more focused on taxation, business law, or financial accounting.

Assessment of Internal Control Systems: A deep understanding of an entity’s internal control mechanisms is essential for success in AUD, highlighting the importance of evaluating controls within an audit context.

Emphasis on Ethical Standards: There’s a significant focus on ethics, independence, and the professional responsibilities that are central to the role of auditors, reflecting the profession’s commitment to integrity and public trust.

Professional Judgment and Skepticism: This section uniquely tests the candidate’s ability to apply professional skepticism and judgment, which is crucial for evaluating evidence and making audit decisions.

Complex Question Scenarios: AUD questions often involve complex scenarios requiring candidates to distinguish between closely related auditing standards and principles to identify the most accurate answer. As a Guardfatherbjj observed, ‘hard in application for test day SIMs.’

Lowest Score Bump: The uniqueness of the AUD section lies in its challenge and application, historically noted for the lowest score bump, suggesting a stringent evaluation of candidates’ grasp on auditing standards. As Reddit user begentlewithme insightfully put it, success in AUD demands more than relying on a score bump, highlighting the necessity for a solid understanding over hopeful gambles seen in sections like FAR.

Preparing for the AUD Section of the CPA: How to Pass

Achieving success in the AUD section of the CPA exam demands a well-rounded and strategic study plan that emphasizes both theory and practice:

- Deep Dive into Professional Ethics:

- Delve into the ethical standards and professional responsibilities that are the backbone of the audit profession. Understand the AICPA Code of Professional Conduct, independence requirements, and the ethical guidelines set by regulatory bodies. Utilize case studies and ethical dilemmas to sharpen your ability to navigate complex ethical situations.

- Technology and Data Analytics:

- Embrace the role of technology in modern auditing by mastering the use of data analytics and understanding the IT controls within an entity’s environment. Explore how automated tools and techniques are applied in auditing processes, from risk assessment to evidence collection, and develop the skills to evaluate the reliability and relevance of data.

- Audit Process Mastery:

- Gain a comprehensive understanding of the audit process, from initial planning and risk assessment through to the execution of audit procedures and final reporting. Break down each phase of an audit engagement, familiarizing yourself with the objectives, tasks, and decision-making involved at every step.

- Practice Makes Perfect:

- Dive into practice exams, quizzes, and task-based simulations to build and test your knowledge. Focus on applying auditing standards to various scenarios, and use these practice tools to improve your ability to analyze and solve complex problems under exam conditions.

AUD CPA Exam Day Strategy

Approaching exam day with a clear strategy is crucial to navigating the AUD section effectively:

- Know the Format:

- Ensure you’re well-versed in the exam’s structure, including the balance of multiple-choice questions and task-based simulations. Understanding the format will help you manage your time and approach each question type with confidence.

- Time Management:

- Develop a strategy for allocating your time across the exam, ensuring that you can thoroughly address each question without rushing. Practice pacing yourself during study sessions to build a sense of timing that will serve you well on exam day.

- Stay Calm and Focused:

- Maintain a level head and a focused approach throughout the exam. Read each question carefully, applying elimination strategies to narrow down your choices, and remember to breathe and stay composed, even when faced with challenging scenarios.

“Studying for it is easier than the other tests imo, but the actual exam itself was extremely tricky, if that makes sense. My tip – read the question at least 3 times before answering.”

lilmisscpa

A recent CPA candidate shared their experience taking the AUD section, offering insights into the preparation and exam day strategies that could benefit future test-takers. They started with a tight schedule, cramming with Becker after taking FAR, which they felt provided adequate preparation.

MCQs and SIMs Breakdown

- The difficulty of the Multiple-Choice Questions (MCQs) mirrored Becker’s practice questions closely, without the tricky “one-word difference” answer choices. The candidate emphasized the importance of understanding SSARS/SSAE thoroughly, pointing out that the exam covered a broad spectrum of topics. Single Audits were highlighted as an area for scoring “easy points,” especially if one remembers the significance of the $750,000 threshold.

- Task-Based Simulations (TBS) presented a different challenge. Without going into specifics, the test-taker mentioned managing up to 5-6 exhibits in some simulations, which were short and manageable with efficient time management and a solid grasp of the material.

Test-Taking Strategy

This individual described themselves as a fast test taker, preferring not to dwell too long on any single problem to avoid second-guessing. Their strategy paid off, allowing them to finish with about 50 minutes to spare, even after intentionally slowing down by the fourth testlet.

Engagement and Response

The thread where this account was shared also prompted further discussion on SSARS/SSAE, with contributors clarifying the distinctions between various engagement types and the levels of assurance provided. This underscores the exam’s focus on practical application and understanding of auditing and attestation standards.

Another participant echoed the sentiment that while AUD study material seemed more straightforward than FAR or BEC, the actual exam questions and simulations demanded a deeper level of comprehension and application, particularly highlighting the easier nature of TBS compared to MCQs.

Conclusion

The Auditing and Attestation section of the CPA exam is a blend of challenge and opportunity, reflecting the diverse perceptions among candidates—some find it straightforward, others daunting.

The crux of the challenge lies not in the audit material itself but in the nuanced and detailed nature of the questions, which test not just knowledge but the ability to apply it critically. Each answer choice might seem correct for slight variations of the question, emphasizing the need for a meticulous, detail-oriented approach.

Success in AUD hinges on a deep understanding of auditing principles, professional ethics, and the strategic application of concepts, underscoring the importance of thorough preparation and focused attention.

FAQ

AUD emphasizes auditing processes, professional ethics, and the application of judgment and skepticism more than other sections, focusing on evaluating evidence and internal control systems.

Extremely important. The AUD section tests your ability to use data analytics and understand IT controls within auditing processes, reflecting modern auditing practices.

Yes, partial credit is available for task-based simulations, and candidates are encouraged to answer each part as accurately as possible.

Carefully read each question to understand what is being asked and apply a detail-oriented approach, focusing on the specifics of auditing standards and principles.

Balance your study between ethical standards, technology, data analytics, and core auditing principles. Dedicate significant time to practice exams and task-based simulations to enhance your application and analysis skills.