I’ll be honest: when I first started using buy now, pay later (BNPL) services, I didn’t think about how those companies made money. I just wanted the flexibility to split up purchases without maxing out my credit card. But over time, I realized some BNPLs were eating me alive with high interest charges on longer-term loans.

That’s when I looked into Sezzle.

What stood out was its focus on interest-free installments, making it one of the most consumer-friendly options available. Of course, Sezzle is still a financial technology company, and like any business, Sezzle makes money. But how does Sezzle make money? The difference is that with a little responsible spending, you can get all the benefits of Sezzle payments without ever paying extra.

Key Takeaways

- Merchant Fees Drive Revenue: Sezzle makes most of its money by charging merchants a transaction fee for each order.

- Consumer Fees Exist but Are Avoidable: Late fees, rescheduling fees, and service charges can add up, but responsible spending keeps them off your plate.

- Premium Services Add Value: Products like Sezzle Premium and Sezzle Anywhere create extra revenue while offering users more flexibility.

- No Interest on Pay-in-4: Sezzle’s signature product remains interest-free installments, setting it apart from other BNPL providers.

- Responsible Spenders Are Safe: Sezzle is transparent, and responsible users don’t have to worry about the unpleasant surprise of hidden fees and extra costs.

The Core of Sezzle’s Business Model: Merchant Fees

The majority of Sezzle’s revenue actually comes from merchants, not consumers.

When a shopper uses Sezzle at checkout, the merchant pays Sezzle a transaction fee (often around 6% of the transaction amount) plus a small flat fee. This is how Sezzle charges merchants for giving customers the option of interest-free payments.

Why do merchants agree to this?

Because Sezzle helps them increase sales and customer retention. By allowing buyers to split payments, merchants close more deals at the point of sale, particularly with younger consumers who value financial flexibility.

You’ll see Sezzle offered across a wide range of retailers, from fashion and beauty brands like Kylie Cosmetics and Nasty Gal, to electronics and lifestyle shops such as GameStop and Bass Pro Shops. Even niche businesses—think local furniture stores, fitness equipment retailers, and jewelry brands—integrate Sezzle to attract shoppers who might not have purchased without flexible payment options.

For example:

- A clothing retailer might see a $300 cart abandoned if a customer can’t pay all at once. With Sezzle, that cart is more likely to convert since it breaks down into $75 installments.

- An electronics store selling headphones or laptops can secure bigger-ticket sales by giving buyers the option of paying over six weeks.

Small businesses benefit, too. By adding Sezzle, they can compete with larger companies that already offer financing. I’ve even thought about adding Sezzle as an option for my own small business.

Consumer Fees: Late Payments and Rescheduling

But back to the question at hand: how does Sezzle make money? Although Sezzle’s Pay-in-4 option is interest-free, they do charge a few consumer fees:

- Service Fee: This fee depends on the amount of your order and ranges from $4.49 to $7.99.

- Late Payment Fees: Up to $16.95 if you miss a scheduled payment.

- Late Saver Fee: A smaller $1.99 charge if you reschedule before your payment bounces.

- Rescheduling Fee: After one free reschedule, Sezzle charges a fee to adjust your payment schedule again.

These aren’t hidden fees—Sezzle is upfront about them. And importantly, they’re avoidable if you make your Sezzle payments on time. This is where responsible spending comes in: use Sezzle as a tool for financial flexibility, not as a crutch.

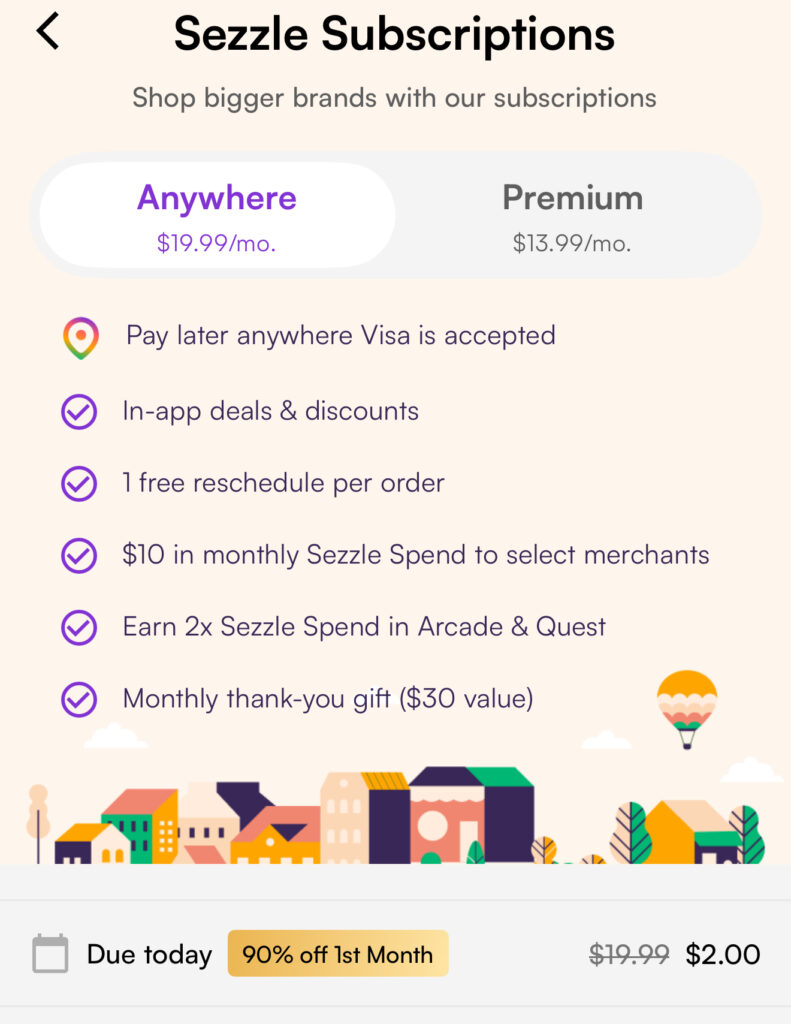

Premium Services: Sezzle Anywhere & Sezzle Premium

In addition to merchant and consumer fees, Sezzle also earns revenue through its subscription plans:

- Sezzle Anywhere ($19.99/month): Unlocks the ability to use Sezzle anywhere Visa is accepted with a reusable virtual card, plus perks like bonus Sezzle Spend and an extra free reschedule.

- Sezzle Premium ($13.99/month): Focused on in-app shoppers, this plan offers exclusive brand discounts, monthly Sezzle Spend, and additional perks for frequent users.

These subscriptions give Sezzle a steady revenue stream while offering shoppers more flexibility and rewards. And while the monthly cost might seem a little steep, they often offer discounted sign-ups and come with perks that make it feel like a tradeoff.

Longer-Term Loans and Interest

Although Sezzle is best known for its interest-free Pay-in-4, like other apps and services in the BNPL market, Sezzle has explored offering longer-term payment solutions. In those cases, interest fees may apply—similar to Affirm or Klarna.

This is standard in the financial technology industry, but it’s not Sezzle’s main focus. Sezzle continues to emphasize short-term, interest-free payments as its core product, keeping it different from BNPLs that rely heavily on charging consumers interest.

Other Revenue Streams

Like many in the BNPL service space, Sezzle has additional ways to monetize:

- Interchange Fees: When you use a Sezzle Card, Sezzle earns a percentage from Visa/Mastercard networks.

- Strategic Partnerships: The Sezzle team partners with merchants and fintech companies to integrate Sezzle into more payment options.

- Operational Efficiency: By scaling across markets, Sezzle lowers costs while boosting revenue.

These strategies help Sezzle grow while keeping interest-free installments available to everyday shoppers.

The Bottom Line: How Sezzle Makes Money

So, how does Sezzle make money? By combining:

- Merchant fees (their biggest revenue driver).

- Consumer fees (late payments, reschedules, service fees).

- Premium programs (Sezzle Premium and Sezzle Anywhere).

- Strategic partnerships and interchange fees.

And here’s the part I love: unlike other BNPLs that rely on charging consumers interest, Sezzle’s model puts most of the cost on the merchants. If you use your account wisely—paying on time and avoiding unnecessary reschedules—you’ll never pay more than the original transaction amount. Sezzle aims to give shoppers financial flexibility while staying transparent about where its money comes from. And from my own experience, that’s a much better deal than the “free at first, expensive later” loans that other BNPLs run.

Now that you know the fine print, sign up with Sezzle today and start taking advantage of buy now, pay later.

FAQs

Sezzle’s biggest revenue source is merchant fees. Merchants pay Sezzle a percentage of each transaction in exchange for increased sales and customer retention.

Yes, but only in certain situations. Late fees (up to $16.95), rescheduling fees, and service charges like the $7.99 Sezzle Anywhere fee apply if you miss or adjust payments.

Sezzle Premium is a subscription service offering higher limits, flexible payment schedules, and perks. It’s another way Sezzle earns money while offering extra value to frequent users.

Only on certain longer-term loans. Sezzle’s main product, Pay-in-4, is always interest-free.

Sezzle may charge a late fee (up to $16.95).