You’ve finally found the perfect laptop for work and school, but it’s $800. At checkout, you’re offered a choice: pay in full, or break it into four $200 payments over six weeks, interest‑free. That’s buy now, pay later (BNPL) in action — a way to ease big purchase pressure.

With 31% of U.S. back‑to‑school shoppers expected to go into debt this year—and 13% of them relying on BNPL—this kind of flexibility is becoming a popular budgeting tool.

So, what is buy now, pay later exactly, and how does it work? In this short overview, I’ll give you the 411 on BNPL loans, whether they report to the credit bureaus, and more.

Key Takeaways

- Split Payments, No Interest: Buy now, pay later breaks a purchase into smaller, manageable, often interest-free payments.

- Trusted Names in the Space: Top BNPL lenders include Sezzle, Klarna, Affirm, and Afterpay.

- Helps You Budget Smarter: Installment loan options (BNPL) can ease the strain of larger purchases if used with a plan.

- Credit Building Is Expanding: Some services, like Sezzle Up, offer opt-in credit reporting—and new credit scoring models are starting to include BNPL data.

- Missed Payments Have Consequences: Late or missed payments can lead to additional fees, account holds, or a negative credit score impact.

What Is Buy Now, Pay Later?

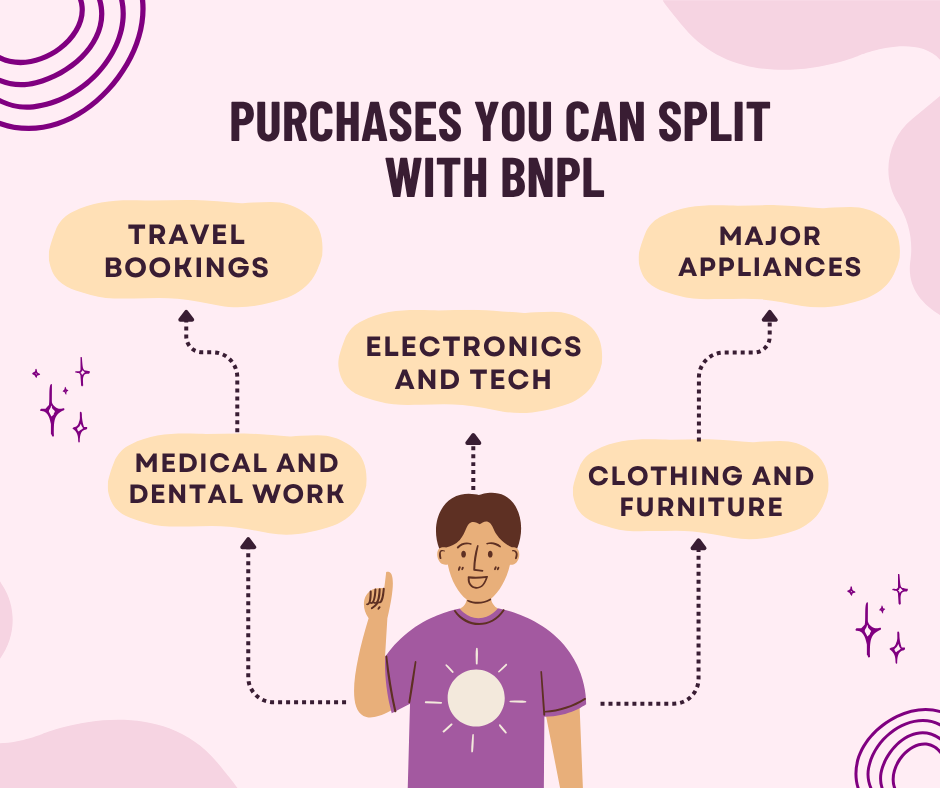

Buy now, pay later is a financing tool that breaks your total cost into multiple installments — often four, spaced every two weeks. It’s commonly used for:

- Tech and electronics

- Clothing and furniture

- Travel bookings

- Medical or dental bills

- Back-to-school and holiday shopping

- Major purchases like appliances or home upgrades

Let’s say you’re buying a $600 sofa. Instead of paying all at once, you choose a BNPL option like Sezzle. You pay $150 today, and the rest is automatically charged over the next few weeks. There is no interest, no late-night credit card stress, just interest-free installments or payment plans.

Some services offer longer monthly payments (3–12 months), sometimes with interest, depending on your purchase amount, credit profile, or repayment terms.

Is BNPL Too Good to Be True?

Not necessarily. BNPL is legit and growing fast, especially among Gen Z and Millennials. The key is using it intentionally, not impulsively.

Here’s what to love:

- You avoid interest charges (if paid on time)

- You don’t need a traditional consumer credit account

- It’s fast, easy, and often integrated directly into your favorite online shopping platforms

But there are trade-offs:

- Late fees on BNPL loans can add up quickly if you don’t pay monthly or as agreed

- If you miss payments, your account may be frozen or sent to a collections agency

- Juggling too many BNPL apps at once can lead to financial issues

I’ve used a BNPL myself to split up a last-minute vacation, so I get the appeal. I think that if you’re looking for a tool to enhance budgeting, BNPL can help. However, if you’re using it to delay financial reality, it might backfire. The takeaway? BNPL users should consider these pay-later loans as a financial tool, not a shortcut.

Where BNPL Stands Out — and Where It Doesn’t

BNPL works best when you need short-term breathing room, without getting stuck in revolving debt on outstanding loans.

| Use Case | BNPL Strength ✅ | Better Alternatives ❌ |

|---|---|---|

| Splitting big purchases | Yes — keeps it manageable | Credit card with points |

| Building credit history | Sezzle Up, Affirm | Traditional credit cards |

| Emergency expenses | Maybe — if budgeted | Personal loans or savings |

| Impulse shopping | No — risk of overspending | Waiting or budgeting ahead |

How to Use Buy Now, Pay Later: A Quick Walkthrough

- Shop like normal: Add items to your cart online or shop in-store at a participating retailer.

- Choose a BNPL provider at checkout: Select a payment method like Sezzle, Afterpay, or Klarna.

- Get approved instantly: Most providers do a soft credit check (or none) and give you a quick approval decision.

- Make your first payment: You’ll usually pay 25% upfront—the rest is split into equal installments. Some providers charge interest, so keep that in mind.

- Pay automatically: Once you’re set up, the money gets pulled from your debit card or bank account like clockwork. Before agreeing, check the fine print for processing fees.

- Stay on track: Pay on time to avoid fees. Some platforms (like Sezzle Up) offer opt-in reporting of on-time payments, and with FICO’s upcoming BNPL-inclusive scores, that could matter more soon.

Final Thoughts

Buy now, pay later can be a smart way to handle purchases — whether it’s an upgrade you’ve planned for or a necessity you can’t delay. Services like Sezzle have made it easier to shop responsibly, even offering paths to credit building without the risk of traditional debt or high interest rates.

As long as you know your budget, automate your payments, and avoid overextending yourself, BNPL can be a helpful option, not a trap — especially when used with flexible payment options that fit your financial flow.

FAQs

BNPL options allow you to buy something now and pay it off in smaller installments — usually interest-free — over a short period of time. These are often referred to as pay-in-four loans or short-term loans.

Some, like Sezzle Up, offer opt-in reporting of on-time payments, and with new FICO scores including BNPL data, responsible use may start to influence your credit profile.

You could face late fees, account holds, or even reporting to a collections agency, depending on the provider. Set up auto-pay to protect your credit score.

Many BNPL services work both online and in-store. Sezzle, for example, partners with brands across both online and in-person shopping.

When comparing BNPL vs credit cards, BNPL may offer more transparency and zero interest on monthly payments, but credit cards often come with rewards, credit limits, and revolving options. Choose the best fit for you based on repayment terms.

There are tons of small and large payment items you can use with BNPL, like booking flights or hotels, PS5 or Xbox, iPads or iPhones, furniture, groceries, laptops, concert tickets, jewelry, clothing, shoes, TVs, and all types of electronics. More companies, products, and websites are adding more BNPL options as a convenient way to shop.