I’ve tested just about every buy now, pay later app out there—Sezzle, Klarna, Affirm, Zip, even Splitit. Most of them follow the same formula: sign up, get approved, split your purchase, and pay over time.

But Sezzle and Splitit? They couldn’t be more different.

One is simple, transparent, and genuinely helpful when life throws you a bill you didn’t plan for. The other felt like trying to open a digital door that doesn’t exist. If you wonder about these payment method options, installment plans, and how to make four payments with zero interest, keep reading.

BNPL Services: Which One Should You Choose?

The buy now, pay later market has exploded, giving shoppers dozens of installment payment options. But not all services are built the same. Some, like Sezzle, focus on everyday affordability and credit-building. Others, like Splitit, try to serve shoppers with high credit limits.

Choose Sezzle if:

- You want interest-free payments split into predictable installments.

- You like having flexible payment options and the ability to reschedule.

- You want to build credit history with Sezzle Up.

- You prefer a simple, mobile-friendly platform for everyday purchases and bills.

Choose Splitit if:

- You already have strong credit and want to avoid any new soft credit checks.

- You only shop occasionally with major retailers that still support it.

Keep reading to learn more about both of these BNPL options.

What Is Sezzle?

Sezzle is one of the best options on the BNPL market. It lets you split purchases into four interest-free installment payments over six weeks. You pay 25% upfront, and the rest in equal payments every two weeks.

The best part? It’s quick to set up, doesn’t require a hard credit check, and you can use it for both online and in-store purchases, from groceries to gifts to travel expenses. Have a limited credit history? You may still be able to be approved for Sezzle.

There are lots of things to love about the buy now, pay later option, but here is what makes Sezzle stand out for me: accessibility and transparency.

This means that:

- There are options to reschedule a payment once per order for free.

- The app integrates with Apple Wallet and Google Pay for easy tap-to-pay options.

- It offers Sezzle Up, a free opt-in feature that reports your payments to credit bureaus, helping you build credit history while avoiding traditional debt.

- You can see everything in one clean dashboard: upcoming payments, total spending, and due dates.

Sezzle felt seamless, like Venmo with a built-in safety net. This is something I appreciate in BNPL services.

Save $15 on Your First Amazon Purchase via Sezzle App

What Is Splitit?

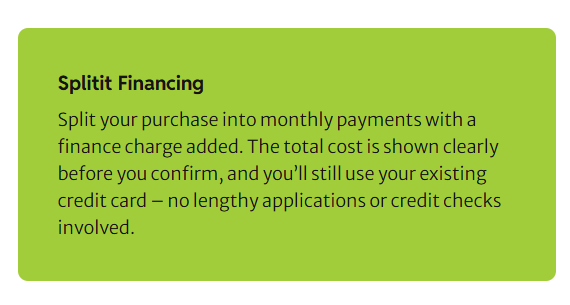

Splitit takes a very different approach. Instead of giving you a new line of credit, it uses your existing credit card to divide your purchase into smaller monthly payments.

In theory, that sounds convenient: no new account, no extra debt. But in practice, it’s confusing.

When I tested Splitit, I couldn’t even create an account. There was no sign-up button anywhere on their website, just a “Manage My Account” link that only works if you already have one. Their FAQ even says they can’t assist with checkout and that you’ll need to contact the merchant instead.

You also can’t browse where it’s accepted. Splitit is available only through certain merchants (like luxury goods or electronics stores), and even that’s hit or miss. For example, NewEgg was listed as a partner—but when I went to check out, Splitit wasn’t an option at all.

Here’s the biggest catch: Splitit requires that your credit card have the full amount of the purchase available for authorization. So if you buy a $1,000 laptop, your card needs $1,000 of open credit before you even start.

That authorization hold stays in place and adjusts with each payment, which means your available credit stays tied up until the last installment clears. It’s marketed as a “smart financing solution,” but it feels like something built for businesses, not financial flexibility or consumer needs.

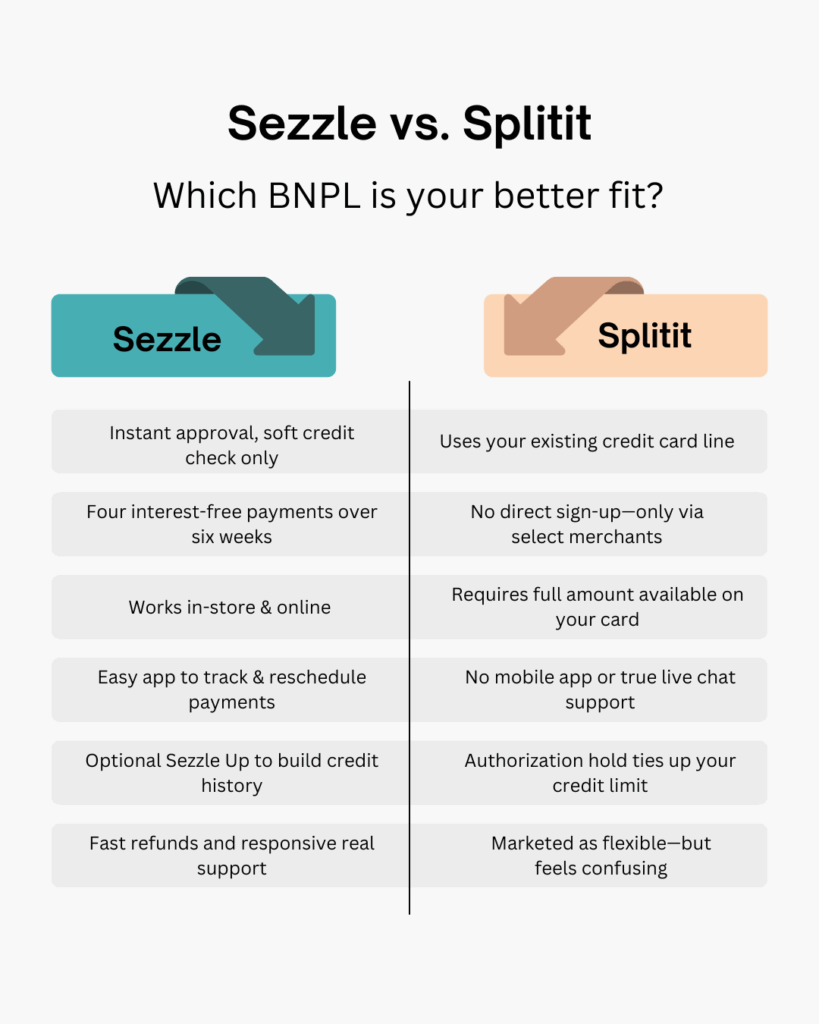

Sezzle vs Splitit: Key Differences

Here’s a quick side-by-side breakdown of how these two BNPL platforms really compare:

| Feature | ||

| Approval Type | Instant approval with soft credit check | Uses your existing credit card |

| Interest / Fees | 0% if paid on time; small service fee on some orders | 0% on Retail Plans, but card authorization can limit spending |

| Credit Reporting | Optional with Sezzle Up | No credit reporting |

| Availability | 47,000+ merchants; in-store + online | Limited merchants, mostly electronics or luxury |

| App & Access | Full-featured app; easy to track and manage | No app; must use merchant websites |

| Ease of Setup | Create an account instantly | No direct sign-up process through the website |

| Payment Flexibility | Reschedule one payment for free | Tied to your credit card issuer’s billing cycle |

| Best For | Everyday purchases, budgeting, and building credit | People with large credit limits who hate new accounts |

Real Purchase Comparison

To test how each platform works in real life, I ran both through a real-world scenario. I used Sezzle to pay for my car insurance, a nontraditional purchase that’s not even retail. I wanted to see if it would actually process for another article I was writing.

Spoiler alert: it worked. The payment plan is split evenly across six weeks, with a small fee attached. The app updated instantly, sent reminders before the monthly payments, and tracked my balance in real time. It wasn’t totally free, but it worked. And for people juggling paychecks or needing short-term flexibility, that small fee is worth it.

Then I tried Splitit. I attempted a mock purchase at NewEgg, one of their advertised partners, for a midrange gaming PC. Splitit wasn’t listed as a payment option—anywhere. No app integration, no checkout button, nothing.

Even if it had worked, I’d have had to free up my entire credit limit just to hold the purchase. In other words, it’s not a buy now, pay later; it’s “freeze your funds now and hope it works later.” The difference was night and day. Sezzle let me handle a real bill in minutes. Splitit left me searching Google for proof it even existed.

App Experience and Customer Support

Sezzle’s app feels intuitive and trustworthy. You can check your schedule, adjust dates, and get automated reminders. Even with large purchases, everything’s visible in one clean dashboard. When I had a small login issue from an old account, a customer service representative fixed it in under 15 minutes and followed up by email to confirm.

Even better, when a flight I booked through Sezzle was canceled before it was fully paid off, I filed a dispute directly through the app. The refund was processed quickly and automatically; no endless calls or waiting for a human to intervene. Within a few days, my payments were reversed and my balance was cleared. That kind of reliability made me trust the platform even more.

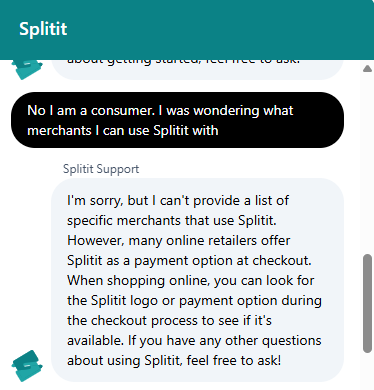

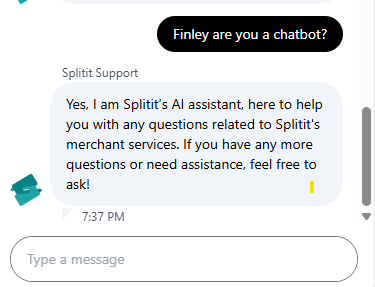

Splitit, by contrast, doesn’t have an app at all. The only support option is a “live chat” on their website, which turns out not to be live at all. When I messaged their support, I learned I was actually talking to an AI assistant named Finley. I don’t mind AI help (clearly), but labeling it as live feels misleading.

The chatbot couldn’t even provide a list of stores that use Splitit, only vague directions to “look for the logo at checkout.” It left me feeling like the company was set up to talk to merchants, not real shoppers.

Sezzle clearly invests in customer experience. Splitit seems to rely on automated systems and merchants to fill in the gaps—and that’s not the kind of reliability you want when your money’s involved.

Bottom Line

After testing both apps, the difference wasn’t just about tech — it was about trust. Sezzle felt like a real financial partner that respects your time, budget, and circumstances. Splitit, meanwhile, reminded me of those tools built for companies that never stop to ask what the shopper actually needs.

If you’ve ever stared at your bank balance trying to figure out how to stretch it a little further, Sezzle gives you breathing room without the shame or the stress. It’s flexible enough for emergencies, transparent enough for everyday budgeting, and stable enough to rely on month after month. At the end of the day, that’s what flexible payment solutions should do: make your life easier, not harder.

Get $15 Off Your First Target Purchase w/ Sezzle App

FAQs

Splitit is one of the Sezzle alternatives that lets you split a purchase using your existing credit card, without opening a new loan or credit account.

No interest on standard retail plans if you keep up with payments, but your full purchase amount must be available as an authorization hold on your card upfront.

No. Splitit does not perform hard credit checks or report to credit bureaus, so it neither builds nor harms your credit rating directly.

In most cases, no. You must shop at a participating merchant that offers Splitit as a payment option. There is no direct consumer sign-up process.

Splitit works with major cards like Visa, Mastercard, and Discover, depending on the retailer’s support and terms. It does not work with debit cards like other BNPL options.

For most consumers, no. While Splitit uses your existing card and avoids new credit lines, it lacks easy merchant access, reporting features, and flexibility. Sezzle is more user-friendly and transparent for everyday use.