When my daughter got her college acceptance letter, I was thrilled. But between tuition deposits, essentials, and the cost of last-minute travel, the expenses piled up faster than I expected.

I wasn’t in crisis, but I was feeling the pressure. I didn’t want to rack up credit card debt—and with revolving credit already growing at nearly 10% a year, compared to less than 2% for other types of credit, it felt smarter to avoid adding to that trend.

That’s when I started looking into buy now, pay later (BNPL) apps as a way to spread out purchases without interest or long-term loans. I tested out two of the biggest names—Sezzle and Afterpay—to see which one actually made managing my money easier. And while they both get the job done, one stood out for flexibility, control, and credit-building potential.

Here’s what I learned.

Quick Pick: Sezzle or Afterpay?

- Best for Budgeting: Sezzle offers more control with built-in tools for rescheduling, tracking, and managing your payments—all interest-free.

- Best for On-Time Shoppers: Afterpay works well if you’re always on top of payments, but it’s less forgiving if your schedule shifts.

- Credit Building: Sezzle lets you opt into credit reporting through Sezzle Up, helping you build credit history over time. Afterpay doesn’t report on-time payments.

- Subscription Perks: Sezzle offers optional upgrades like Sezzle Premium with extra perks and rewards. Afterpay doesn’t offer a membership model.

- Approval Process: Both use soft credit checks, but Sezzle is more transparent about how your spending power grows and gives you more visibility in-app.

Sezzle vs Afterpay: At a Glance

| Feature | Sezzle | Afterpay |

|---|---|---|

| Payment Schedule | 4 payments over 6 weeks | 4 payments over 6 weeks |

| Credit Check | Soft check only | Soft check only |

| Credit Reporting | Yes, with Sezzle Up | Not currently (unless account is in default) |

| Rescheduling | 1 free per order | Not allowed |

| Late Fees | Capped, transparent | Capped, but stricter |

| In-Store Use | Yes (via digital wallet) | Yes (via Afterpay Card) |

| Buying Power | Adjusts with use | Varies without clear explanation |

| Customer Support | Live chat + email | Mostly self-service |

| Subscription Perks | Varies without a clear explanation | None |

What It’s Like to Use Sezzle

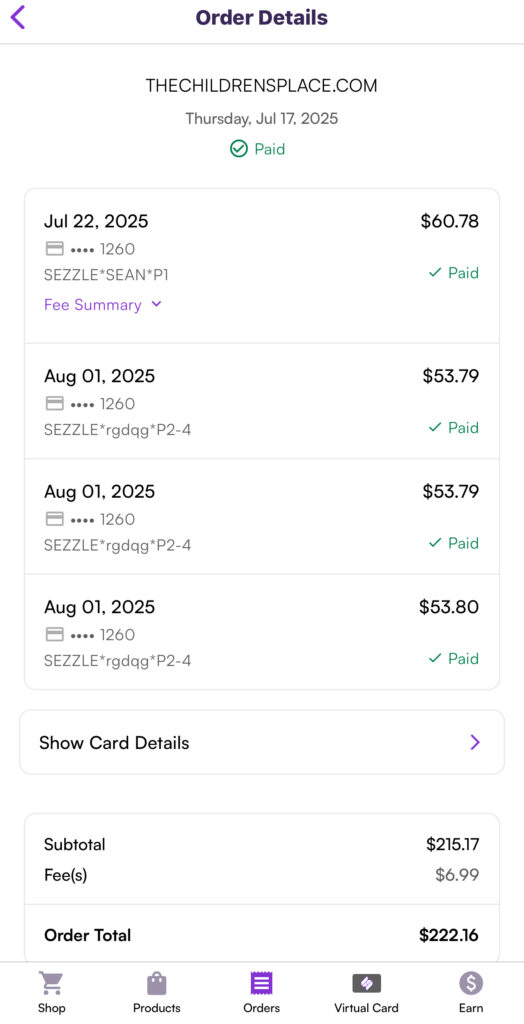

Honestly, I have used Sezzle so many times. I can’t remember the first purchase, but one of the most memorable was when I needed to buy back-to-school supplies during a tight week. I was a divorced mom, and the purchase was just $216, but it felt like a lot at the time. With Sezzle, I paid just over $60 up front—including a small service fee—and the rest was split into payments every two weeks.

What stood out most was the flexible payment options. Now, it is a bit annoying that their service fee has increased a few cents since this purchase a few months back, but it is better than paying interest.

Sezzle Up was also a game-changer. One of my favorite perks is the ability to reschedule one payment for free. Once I linked my account and paid off a few orders, I was able to enroll and start building credit. Sezzle reports your payment history to all three major credit bureaus—something Afterpay doesn’t do. With FICO expected to factor in BNPL activity more heavily in 2025, that’s no small thing.

Sezzle Pros

- Four interest-free payments with soft credit check

- Free payment reschedule options

- Option to build credit history with Sezzle Up

- In-store and online purchases

- Real-time notifications and reminders

- Customer support was fast and helpful

Sezzle Cons

- $7.49 one-time fee when making a purchase

- $1.50 fee if paying with debit instead of a bank account

Sezzle

Afterpay: Convenient but Unforgiving

Afterpay was easy to set up as well. I linked my debit card and was instantly approved with $1,000 in buying power. I used it to buy concert tickets (Monica + Brandy reunion tour—bucket list!) and the app split the $380 into four automatic payments. So far, so good.

But the second time I tried to make a purchase—with active orders paid on time—I was declined without warning. This seems to be a pattern: many users report sudden limit reductions or rejections without clear reasoning. Unlike Sezzle, there’s no way to reschedule payments either. If your paycheck is late or you miss a day, you’re out of luck.

And once you’re flagged, it may take a long time to recover. In one Reddit thread, a user shared that after paying off just a $30 balance, their limit was reset to $50, and it took over a year and a half to earn back their original spending power. Several others reported similar experiences, especially after missing just one payment, even if it was eventually paid. Afterpay doesn’t seem to offer much leniency when it comes to rebuilding trust with the platform, which could be frustrating if you’re working on improving your financial habits.

The app itself is very shopper-friendly, though, which is worth factoring into your decision. Think deals, trending items, and brand promos. But that shopping mall vibe? It can make it harder to stay disciplined if you’re already working on budgeting.

Afterpay Pros

- Interest-free installments

- Sleek mobile app

- Thousands of online and in-store retailers

- Fast, soft-approval decisions

Afterpay Cons

- Can’t reschedule payments

- Missed payments lower your limit fast

- No credit reporting unless delinquent

- Customer support is mostly self-service

Afterpay

Installment Flexibility

Both Sezzle and Afterpay let you break purchases into four interest-free payments over six weeks, but Sezzle edges out for one key reason: flexibility.

With Sezzle, you can shift due dates right inside the app. Here are a few real-world ways that might look:

- Paycheck Timing: Bought $200 worth of groceries? Instead of four $50 payments, you can push the second installment back a few days so it lines up with payday.

- Unexpected Bill: Had a utility bill hit the same week as a Sezzle payment? Reschedule one installment (free the first time per order) and spread out the pressure without late fees.

- Travel Costs: Booked a $400 flight? You’ll pay $100 at checkout, then three $100 payments. If the second payment feels too close to rent week, you can shift it ahead and stay on track.

- Back-to-School Shopping: For example, when I bought $240 worth of back-to-school supplies, I paid $60 upfront and rescheduled one of the later payments when my paycheck hit.”

With Afterpay, you don’t get this kind of wiggle room. Payments are locked in, and if one fails:

- You’ll be charged a late fee (capped but still frustrating).

- Your spending limit may be reduced suddenly.

- There’s no way to “catch up” other than paying off the balance and waiting for Afterpay to (maybe) restore your limit.

Bottom line: Sezzle lets you adapt payments to your life. Afterpay expects everything to go perfectly on schedule, something most of us can’t guarantee.

Fees, Interest & Transparency

Neither app charges interest when you pay on time. But both include service or late fees under certain conditions. One of the main reasons I wanted to write this article on BNPL services is so that online shoppers looking for an instant approval decision wouldn’t be surprised by hidden fees.

Here is how they stack up:

Sezzle

- $7.49 service fee (usually baked into the first payment)

- 1 free reschedule, then $5–$7.50 fee for additional changes/rescheduling options

- $1.50 late saver fee if a bank account isn’t linked

Afterpay

- No service fee

- Late fee up to $8 per missed payment

- No rescheduling, and limits can be reduced quickly

Pro Tip: Link a bank account in Sezzle to avoid extra charges and qualify for Sezzle Up.

App Experience: Afterpay Feels Smoother, But Sezzle Works Smarter

Afterpay’s app is polished and easy to scroll through. The layout feels modern, and the home screen is filled with store listings, promos, and trending items. If you like discovering new brands or browsing deals while you shop, it’s a fun experience. The flip side? It can feel more like walking into a mall than opening a budgeting tool, which isn’t always great if you’re trying to spend less.

Sezzle, on the other hand, keeps things simple. When you log in, you immediately see:

- What you owe today

- What’s due next

- How much buying power you have

- Quick options to reschedule or view your payment history

It’s straightforward, and I liked that it didn’t push me to shop; instead, it helped me manage what I already bought. Now, I did recently receive notifications that I had $10 in Sezzle Spend to use on a purchase. I didn’t really plan to use Sezzle as a payment method at this time, but it was a little tempting.

Sezzle also sends other helpful notifications—not just about payments, but when an order ships or when there’s a deal at a store I actually shop at.

But what about Afterpay? When I tried Afterpay’s one-time virtual card, the setup felt slow and clunky, especially with the Ticketmaster countdown clock ticking. Sezzle’s virtual card worked more smoothly and added right into my Apple Wallet for quick tap-to-pay. They also send payment reminders and allow you to set automatic payments on your split purchases.

Bottom line: Afterpay’s app is slick and shopper-friendly, but to me, Sezzle performs better and has a wider range of options and more flexibility.

Credit History Building & Membership Perks

As of now (things are always changing), Afterpay doesn’t report to credit bureaus unless your account goes to collections. So even if you’re a perfect payer, you won’t see those benefits reflected on your credit report. With Sezzle Up, you can build credit history just by paying on time. Below are some other perks I found when looking at Afterpay vs. Sezzle.

| Feature | Sezzle Up | Afterpay |

|---|---|---|

| Credit Reporting | ✅ Yes (all 3 bureaus) | ❌ No |

| Credit Check | Soft only | Soft only |

| Bank Link Required? | ✅ Yes, for Sezzle Up | ❌ No |

| Rewards or Membership? | ✅ Sezzle Premium available | ❌ No perks or rewards |

| Monthly Fee | Free (Up) / $19.99 (Anywhere) or $13.99 (Premium) | Free |

While Sezzle offers optional upgrades like Sezzle Premium and tools like Sezzle Up for credit building, Afterpay doesn’t have a true rewards program anymore. They discontinued the Afterpay Plus Card and Pulse Rewards in 2024, and although a new rewards program was supposed to launch in spring 2024, it never materialized. Many users on forums have expressed frustration, noting that all that’s left are limited gift options—hardly a substitute for a real rewards system.

Final Verdict: Sezzle Edges Out Afterpay

If you’re looking for a flexible, reliable, and more supportive BNPL app, Sezzle is the winner. It’s built with the shopper in mind, not just the sale. Sezzle helps you plan, stay on track, and even build credit history, all while offering the same interest-free payment structure as Afterpay. Afterpay is still a solid option, especially for impulse purchases at trendy brands. But if you care about budgeting, payment control, or financial growth, Sezzle is simply the smarter pick.

FAQs

No. Both Sezzle and Afterpay let you split purchases into four interest-free installments over six weeks as long as you make on-time payments.

Yes, Afterpay and Sezzle work with in-store and online purchases through Apple Pay, Google Pay, or their one-time virtual cards.

Sezzle does report to credit bureaus through Sezzle Up, which reports your payment history to all three major credit bureaus. Afterpay does not currently report positive credit history.

With Sezzle, you can reschedule a payment once per order for free, and additional changes come with a small fee. Afterpay does not allow rescheduling payments at all.

Sezzle is the stronger option. It offers more flexible payment options, credit-building features, and clear payment reminders—tools designed to support long-term financial wellness.