According to the Federal Reserve Bank of New York, Americans hold a staggering amount of credit card debt, totaling $1.18 trillion as of the first quarter of 2025.

Yet, you’ve probably seen the rapid increase of Buy Now, Pay Later services, such as Sezzle or Klarna, pop up during online checkout. They promise interest-free payments and no hard credit checks.

So, could Buy Now, Pay Later help decrease that seemingly insurmountable debt mountain? And, more personally, could it help you create a safer financial future? Let’s break down how both systems work, how they make money, what they do to your credit score, and what you’ll want to consider before clicking “buy.”

Key Takeaways

- BNPL Is Simpler, But Short-Term: Buy now, pay later services break purchases into a few easy payments, but only some plans report to credit—though that’s changing.

- Credit Cards Help Build Credit: When used responsibly, credit cards support your credit history and can earn rewards, but carry real risk if misused.

- Late Fees Can Sneak Up: Both options charge penalties for missed payments, but credit cards tend to hit harder with late fees and interest.

- BNPL Doesn’t Offer Much Protection: BNPL services usually lack the fraud protection and purchase guarantees that come standard with major credit cards.

- Value Depends on Your Habits: If you’re organized and pay in full, credit cards win. If you want predictability and low commitment, BNPL may suit you.

BNPL vs Credit Card: How They Work

How Does Buy Now, Pay Later Work?

Buy Now, Pay Later (BNPL) companies let you split a purchase into smaller monthly payments—usually four interest-free installments. You’ll pay one upfront and the rest every two weeks. No interest, no annual fees… if you pay on time.

These services often don’t do hard credit checks, which makes them accessible if you have poor credit. But be warned: late payment fees can add up fast, and missed payments can still get reported to the three major credit bureaus, depending on the provider.

How Do Credit Cards Work?

When you use a credit card, you’re borrowing money from a credit card issuer. You’ll get a set credit limit and a billing cycle, typically a month. If you pay your full balance on time, you won’t owe any interest. But if you carry a balance? Say hello to interest rates that can range from annoying to downright brutal.

Major credit cards often come with perks like fraud protection, cashback, or travel rewards. But to get those, you need to stay on top of your billing cycle and avoid falling into credit card debt.

Business Models: How They Make Money

BNPL Business Model

BNPL services make most of their money by charging retailers a small fee per transaction, usually around 4–6%. That’s why you’ll see them featured across so many online stores.

They can also earn revenue through late fees or interest on longer-term installment plans. While many BNPL options are interest-free if paid on time, some extended plans (especially those over 6 months) may come with APRs ranging from 10–30%, depending on the provider.

So while BNPL can be convenient, always check the terms, especially for big-ticket purchases or longer payment windows.

Credit Card Business Model

Credit card companies cash in through a combo of:

- Interest charges (when you carry a balance)

- Merchant fees (like BNPL)

- Annual fees (on premium cards)

- Late fees (if you forget to pay)

If you’re using rewards credit cards, the cost of those perks is usually baked into the interest rates or annual fees.

Buy Now Pay Later Pros and Cons

Pros

- Easy approval, even with poor credit

- Simple payment schedule (usually four interest-free payments)

- No hard credit check in most cases

Cons

- Missed payments can result in late fees or credit score damage

- Doesn’t build credit history unless reported

- Limited buyer protections compared to major credit cards

Credit Card Pros and Cons

Pros

- Builds credit history (as long as you pay on time)

- More security and fraud protection

- Rewards programs and cashback perks

Cons

- High interest rates if you don’t pay in full

- Easy to overspend with a set credit limit

- Missed payments can tank your credit score

Credit Impact: The Good, the Bad, and the Unclear

Here’s where things get dicey. If you’re trying to improve your credit score, you need to know how each option plays with the three major credit bureaus: Equifax, Experian, and TransUnion.

Credit Cards: These are well-established tools for building credit. Your payment history, credit utilization, and length of credit account all factor into your score. That’s why many personal finance experts still recommend using credit cards responsibly.

BNPL Services: This one’s trickier. Some BNPL providers, like Affirm, already report payment activity to credit bureaus. Others don’t—or they report only negative activity, like missed payments. Sezzle stands out with Sezzle Up, an opt-in feature that reports both on-time and missed payments to TransUnion, giving users a chance to support their credit through responsible BNPL use.

So while BNPL may help you avoid a hard credit check, it usually doesn’t build credit unless you opt in to programs like Sezzle Up—or use a provider that reports full repayment details.

Plus, with new credit scoring models evolving to include tracked BNPL behavior, responsible use may offer growing credit benefits over time.

Interest, Fees, and Payment Flexibility

Interest Charges

Most BNPL plans are interest-free as long as you make your payments on time. But longer-term options can come with interest rates. Always read the fine print.

Credit cards, on the other hand, tend to hit you with interest if you don’t pay your full balance each month. These rates can easily top 20%, which is no joke if you’re carrying a balance.

Late Fees

BNPL late fees often range from $0 to $10, depending on the provider, though some charge a percentage of the purchase price on extended plans.

By contrast, Credit card late fees can be higher (some up to $40) and may trigger a penalty APR—a higher interest rate that sticks until you prove you can manage your debt again.

Flexibility

Credit cards give you more control over how much you pay each month, as long as you hit the minimum. BNPL locks you into a set payment schedule. That’s good for discipline, but bad if your budget suddenly shifts.

Asking the Experts (And Real People)

One of the tough things about the BNPL service vs. credit card debate is that opinions are wildly different. In the same Reddit thread, two popular comments read, firstly:

“If I can’t just buy something outright, I simply don’t buy it.”

With the high-upvote (though not ratioed) response,

“Definitely more complex than that. Especially as an adult. Understanding credit/financing will serve you way better than being scared of it.”

Further, some BNPL services can positively (or negatively) affect your credit score:

“Not through BNPL unless you are using Affirm or 12 installments through Afterpay or Klarna, because those are reported to credit bureaus. I get credit alerts every time I pay my Affirm.”

“I’ve bought several through Sezzle. No fees as long as you pay on time.”

Ultimately, it seems like the consensus is pretty simple: though many say “don’t buy what you can’t afford,” others reason that that’s an easier thing to say when you have money to work with. So, if you’re organized, pay on time, and stay within your means, either is fine, and both could even have a positive effect on your credit score. However, BNPL may be safer overall, depending on user habits.

So, Which Is Smarter? BNPL or Credit Cards

There’s no universal answer, but here’s how I’d break it down:

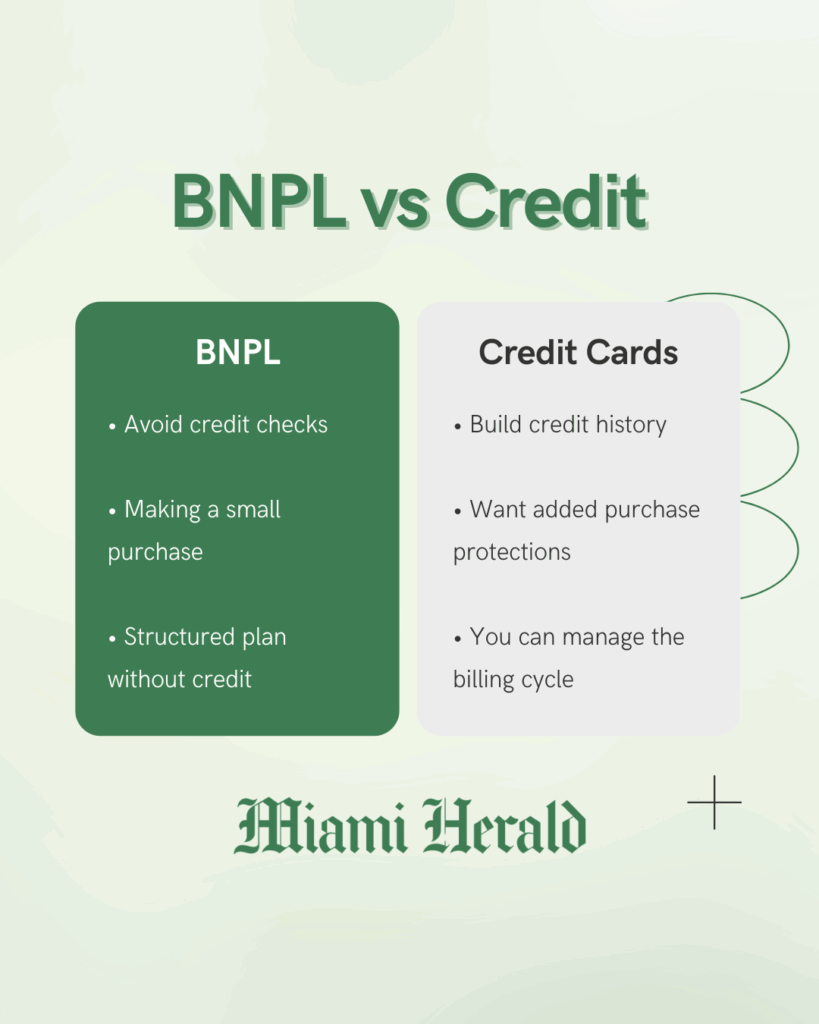

Use BNPL if:

- You want to avoid credit checks or changes to your main score

- You’re making a smaller purchase that you can pay off in a few weeks

- You want a structured plan without dealing with a credit card issuer

Use a Credit Card if:

- You’re focused on building your credit history

- You want added purchase protections

- You can manage the billing cycle without falling into credit card debt

Final Thoughts

Both credit cards and BNPL options can be valuable tools—it all comes down to how you manage them. The best choice isn’t about what’s “better,” but what aligns with your financial habits and goals.

If you’re focused on building long-term credit and can consistently pay in full, credit cards offer rewards, protections, and a solid path to credit growth. But if you need a short-term, interest-free way to break up a purchase—without a hard credit inquiry—BNPL services like Sezzle can be a smart solution.

With features like Sezzle Up and the rise of new credit models that recognize BNPL activity, responsible usage is beginning to carry more weight with lenders. Staying on top of your payments and choosing the right fit for your lifestyle can support not just your present budget—but your future financial success.

FAQs

BNPL splits your purchase into fixed payments, usually interest-free. A credit card gives you revolving credit with more flexibility—but charges interest if you don’t pay in full.

It depends on your habits. Credit cards help build credit and offer rewards, but BNPL is simpler and often better for small, one-time purchases..

Most BNPL providers don’t require a high score. Many don’t check your credit at all for short-term plans.

Sometimes. Some BNPL providers report to the major credit bureaus—especially through opt-in programs like Sezzle Up—and credit scoring models are beginning to include more BNPL data.

Missed BNPL payments can result in late fees, account suspension, and in some cases, your debt may be sent to collections—just like a credit card.