Money’s tight for many Americans—33% say they’re struggling, and over half live paycheck to paycheck. No wonder buy now, pay later (BNPL) apps have become so popular. These services let you split purchases into four interest-free payments or longer monthly plans, covering everything from furniture to footwear.

Over the past year, I have personally tested the largest BNPL providers, signing up, shopping, and even utilizing their customer support and rescheduling options. Some felt like lifesavers, others like tricky traps.

In this guide, I’ll rank the best BNPL services for your spending style—whether you’re more of the squirrel, the elephant, or the fox—so you know which app is right for you.

| Best BNPL App Comparison | ||

| Get Started | |

| Get Started | |

| Get Started | |

| Get Started | |

| Get Started |

1: Sezzle — The Best BNPL

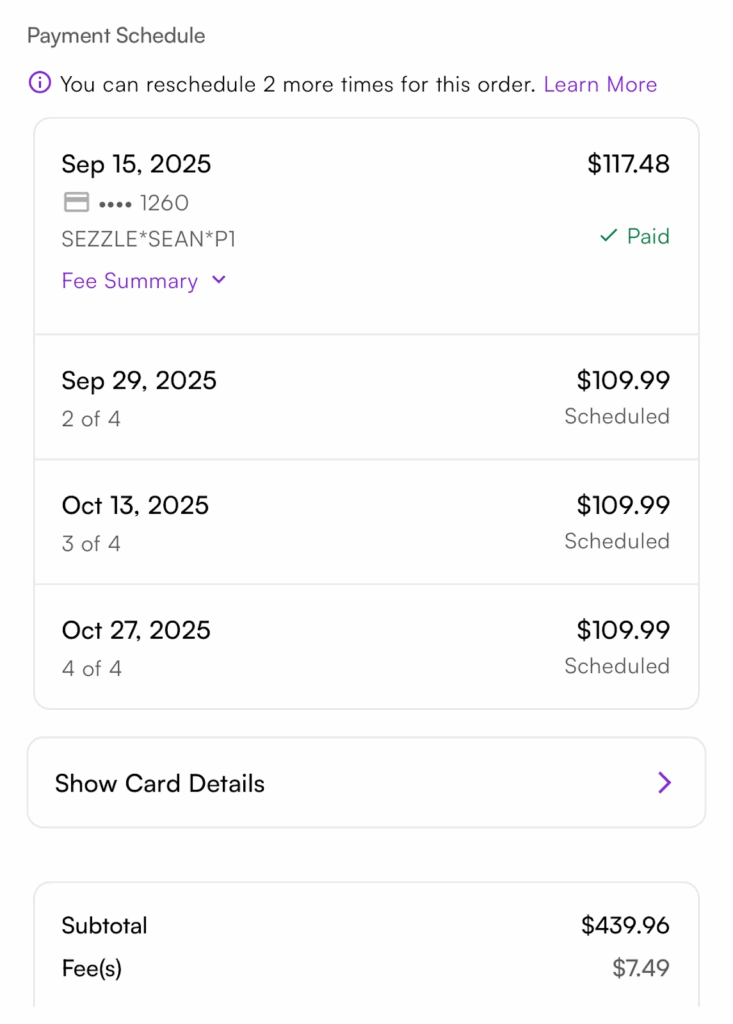

I’ve leaned on Sezzle for everything from a car battery to a $439.96 purchase split into four predictable payments. Instead of draining my bank account at once, I only had to put $117.48 down upfront, then covered the rest in three bi-weekly installments. Even with a small $7.49 service fee, it felt manageable and stress-free compared to swiping a credit card.

Sezzle follows the classic Pay-in-4 model:

- 25% down at checkout

- Then three more payments every two weeks over six weeks

- Payments are interest-free if you stay on schedule

- If you’re a part of Sezzle’s program, you can reschedule once per order for free

Where Sezzle really stands out is Sezzle Up, an optional feature that reports your payments to credit bureaus. That means responsible use can actually improve your credit history, something most BNPL providers don’t offer. Add in the fact that the app is clean, transparent, and easy to manage—you always see your repayment dates, purchase price, and fee summary up front—and it quickly becomes clear why Sezzle is different.

So, why is Sezzle my number one BNPL pick?

Because it consistently feels like a tool that’s on my side. Other BNPL apps either nickel-and-dime you with hidden fees or don’t give you anything back for using them. Sezzle, on the other hand, offers flexibility, credit-building potential, and a safety net if life throws you a curveball. It’s not just about splitting up payments; it’s about splitting payments in a way that’s transparent, supportive, and sustainable.

Sezzle Pros

- Predictable, transparent payment structure

- One free reschedule per order (built-in safety net)

- Sezzle Up reports on-time payments to credit bureaus

- Works online and in-store (Apple Wallet + Google Pay)

- Doesn’t nickel-and-dime with unnecessary fees

Sezzle Cons

- A small service fee applies

- Not designed for large, long-term financing

Quick Guide

- 🦉 This one’s for you if: you’re an owl—wise and practical—wanting predictability, flexibility, and even some credit-building potential.

- 🐇 Skip it if: you’re a rabbit—chasing bigger, longer financing plans. Affirm or PayPal Pay Monthly might be a better fit for large-ticket items.

Bottom Line

Sezzle is my top BNPL pick because it balances short-term breathing room with long-term credit perks. It’s reliable, transparent, and feels like a partner in responsible spending rather than a trap. For everyday purchases, it’s the BNPL that gives me the most peace of mind.

Sezzle

2: Klarna — Flashy, Flexible, and Full of Perks

Klarna is one of the most recognizable BNPL providers in the world, with millions of users and a huge network of online stores and in-store payments. It’s the app you’ll see everywhere—from Sephora to Ticketmaster—and it’s designed to feel more like a shopping mall in your pocket than a financial tool.

But my biggest Klarna test came when my daughter needed an iPad for college, at the last minute. I didn’t have the cash on hand, and Klarna gave me the buying power to grab it immediately. That flexibility was a lifesaver in the moment. The downside? I ended up paying $34.83 in interest on that plan. It wasn’t outrageous, but it was enough to make me think twice about when Klarna makes sense.

Klarna also stands out for its extra perks. I once used its “Pay in 30” feature to delay a bill for a month (no interest charges as long as I paid on time). Another time, I financed a trip through Airbnb using Klarna’s longer-term plan with monthly installments—yes, I had to pay interest that time, but it gave me more breathing room before travel. Klarna even has resale integration, linking directly to eBay and Poshmark so that you can flip unwanted items.

Klarna is smooth, flexible, and packed with features, but it’s also easy to get distracted. Between cashback offers, subscription “gifts,” and an AI shopping assistant that recommends products, it can feel less like a budgeting partner and more like a flashy friend who’s always tempting you to spend.

Klarna Pros

- Wide range of repayment options: Pay in 4, Pay in 30, or monthly financing

- Accepted at thousands of online retailers and in-store with Apple Pay/Google Pay

- Built-in perks: cashback rewards, loyalty card storage, exclusive deals

- Virtual Visa expands use anywhere Visa is accepted

- Helpful extras like resale integration and order tracking

Klarna Cons

- Trial “gift” offers can quietly roll into monthly payments if you forget to cancel

- Interest can sneak up on bigger purchases (like my daughter’s iPad)

- Late fees stack quickly if you miss a payment, with less flexibility than Sezzle

Quick Guide

- 🦩 This one’s for you if: you’re a flamingo—flashy, social, and love perks. Klarna is perfect for spreading out small purchases, snagging deals, and enjoying interest-free installments on everyday buys.

- 🐙 Skip it if: you’re juggling too many arms like an octopus—multiple BNPL loans, subscriptions, or missed payments could turn Klarna’s perks into clutter.

Bottom Line

Klarna is stylish, flexible, and fun to use. It gave me peace of mind when my daughter needed an iPad for school, but the extra $30+ in interest reminded me that its perks come at a price. I recommend it for splurges, travel, and one-off emergencies—but I keep Sezzle as my everyday budgeting favorite.

Klarna

3: Affirm — Best for Big Purchases (But Watch the Interest)

Affirm is one of the biggest BNPL companies in the U.S., and I’ll be honest—I’ve probably used it more than any other. From flights to furniture, Affirm has been there when I needed longer monthly installments or monthly financing. And just recently, they gave me a major spending limit increase, which felt like a nice bonus.

Affirm stands out because it isn’t just about short-term plans like Sezzle’s four interest-free payments. Instead, it offers loan terms ranging from 1 to 60 months. That means you can spread a purchase out over several months—or even years—depending on your budget and credit profile. Some plans are truly interest-free payments if you qualify, but others can go all the way up to 36% APR.

That’s where my caution comes in. On a recent $2,100 flight package (family vacay), one of the payment options Affirm offered me would have racked up more than $875 in interest charges over the loan’s life. Seeing that number in black and white was a wake-up call: yes, the monthly payment structure looked tempting, but the long-term cost was not worth it.

Compared to Sezzle, Affirm is more flexible for large purchases like vacations, electronics, and furniture, but it often comes with higher costs. Sezzle keeps things short, simple, and interest-free, making it a better choice for everyday, responsible spending. Affirm, on the other hand, is like taking out a mini-loan: useful when you need it, but not something you want to rely on too often.

Affirm Pros

- Flexible loan terms from six weeks up to 60 months

- Great for big-ticket items like travel, furniture, or electronics

- Prequalification with a soft credit check shows your options upfront

- No late fees if you miss a payment (a big difference from most BNPL apps)

Affirm Cons

- Interest rates can soar up to 36%, making some plans feel predatory

- More complicated setup than apps like Sezzle—requires choosing plan at checkout

Quick Guide

- 🐘 This one’s for you if: you’re an elephant—steady, reliable, and need to carry big loads over a long distance. Affirm is ideal for spreading out large purchases into manageable monthly installments.

- 🐇 Skip it if: you’re a rabbit who likes quick and clean—you’ll be hopping happier with Sezzle’s simple four interest-free payments and faster payoff.

Bottom Line

Affirm is a strong choice for financing large purchases, but the interest rates can weigh you down. I’ve used it often and appreciated the flexibility, but for everyday shopping, I’ll stick with Sezzle to avoid paying more than I planned.

Affirm

4: Afterpay — Quick, Easy, and Everywhere

Sometimes you just can’t wait. Your laptop charger dies, your kid needs a uniform tomorrow, or concert tickets drop, and you’re not missing out. With credit card interest rates averaging nearly 23%, it’s no wonder so many people are turning to BNPL apps like Afterpay to spread out the cost.

When I tested it, the approval was instant—with just a soft credit check—and I was given $1,000 in spending power right away. Using it for concert tickets felt painless. I paid a quarter of the cost upfront, then got automatic reminders every two weeks. The total never changed, and I liked the predictable structure.

But Afterpay isn’t flawless. While it’s accepted at a huge range of online retailers and can be added to Apple Pay or Google Pay for in-store purchases, I found it clunky that some transactions required creating a one-time virtual card inside the app before checkout.

And though the payments are interest-free installments, missing one can trigger late fees and even shrink your spending limit overnight. Compared to Sezzle, which lets you reschedule payments once for free, Afterpay is far less forgiving if you slip up.

Another thing I find interesting is that they seem to have abandoned some of their social media. I loved following them on Facebook because of their memes, but it is now a ghost town, with nothing being posted since 2023. Maybe it’s silly of me, but it definitely affects my trust when I see a company that isn’t active on its socials.

And also, I came across a story on Reddit that gave me pause. A user shared that being just a couple of days late on a payment cost them 30 points off their credit score. They said, “I’ll NEVER use them again. They dinged my score for being a couple of days late. Affirm never does that to me.”

That kind of consequence feels extreme, and it’s worth remembering: Afterpay rewards punctuality, but the penalties for even small slip-ups can sting harder than other BNPLs like Affirm.

Afterpay Pros

- Four interest-free installments over six weeks, no hidden interest charges

- Fast, app-based approval with only a soft credit check

- Works with a wide variety of online stores and in-store payments

- Debit- and bank-account–friendly (no credit card required)

Afterpay Cons

- Late payments come with fees and reduced spending limits

- According to users, being late can ding your credit big time

- The virtual card process at checkout can feel clunky under pressure

Quick Guide

- 🐇 This one’s for you if: you’re a rabbit—quick, decisive, and just need a fast way to split purchases without paying extra. Afterpay is perfect for impulse buys; you can actually pay off in six weeks.

- 🦉 Skip it if: you’re an owl who likes to plan ahead—Afterpay’s rigid structure and unforgiving late fees make Sezzle or Klarna better picks for flexibility.

Bottom Line

Afterpay is a reliable BNPL app for quick wins and small-to-medium purchases, but it rewards punctuality and punishes mistakes. Great if you’re disciplined; risky if you’re not.

Afterpay

5: Zip — A Clever but Fee-Happy BNPL Option

Zip is one of those BNPL providers that seems promising on the surface: a way to split purchases into four interest-free payments across six weeks, available at thousands of online stores and through in-store purchases with a virtual Visa card. In theory, it’s a convenient alternative to swiping a credit card with sky-high interest rates. In practice, though, my experience with Zip was rocky.

When I tried to set up my Zip account, I ran into login errors and verification snags. Even after contacting support, I couldn’t fully access the app on my own. A colleague helped me test it so I could dig deeper—and while the features are there, they come with some frustrating strings attached.

Here’s the main difference between this app and the others: Zip charges a flat fee on each installment, while other BNPL services like Sezzle usually charge a one-time service fee per order. It may not sound like much, but if you’re running multiple plans at once, the additional payments can add up quickly.

Also, Zip doesn’t usually report on-time payments to credit bureaus, so it won’t help your credit score. On the flip side, missed payments can lock your account or reduce your spending limit quickly. And unlike Sezzle, which lets you reschedule payments once per order for free, Zip doesn’t offer much wiggle room—you’re locked into their monthly payment structure unless you pay off your balance early.

Zip Pros

- Works almost anywhere via Apple Wallet, Google Pay, or the virtual Visa card

- Approvals are quick with only a soft credit check (no hard inquiry upfront)

- Can be used for large or small purchases, including lifestyle buys or shipping costs

- Offers deals and occasional rewards, plus a friend referral bonus

Zip Cons

- Every plan includes a flat installment fee, which makes frequent use more expensive

- Won’t build your credit history (no regular reporting to credit bureaus)

- Accounts can be frozen after missed payments, and support is hit-or-miss

- Frequent app glitches reported by users (like being flagged for “past due orders” when everything is current) and long delays with customer support make reliability a concern

Quick Guide

- 🦊 This one’s for you if: you’re a fox—clever, resourceful, and need a flexible way to handle both monthly plans and quick in-store purchases without pulling out a credit card.

- 🐢 Skip it if: you’re a tortoise—steady and cautious—because those small rescheduling fees and installment charges, plus app issues, can make it harder to stick to responsible spending.

Bottom Line

Zip isn’t a bad option if you’re looking for a buy now, pay later safety net, especially for qualified consumers who want to cover a mid-range purchase price without dipping into savings. But compared to Sezzle’s credit-building perks or Klarna’s loyalty rewards, Zip feels more like a backup BNPL tool than a first choice.

Zip

6: PayPal Pay Later — Familiar but Sometimes Frustrating

PayPal Pay Later feels like the natural next step for anyone who already uses PayPal to check out online. Honestly, I have been using PayPal since its inception (when the dinosaurs walked), and it is still attached to my very first email. Millions of online stores accept it, and I really love it.

Here’s the catch. In the past, Pay in 4 worked smoothly—approval was instant, the first payment came out at checkout, and the reminders kept me on track. But when I got ready to check out on a recent order, clicked PayPal, and waited for the option to appear, it didn’t. PayPal didn’t offer much explanation, which made it clear that eligibility depends heavily on credit, purchase size, and sometimes random factors. Others seem to have experienced this as well, with one Reddit user saying:

“I have used Pay in 4 many times over the past year. Never missed a single payment; in fact, I pay all of them in advance. I have excellent credit. And yet now the option has totally disappeared for me. I have tried multiple different websites that I always used Pay in 4 on before, and the option is totally gone.”

Someone replied that it is a security issue and that “There’s really nothing anyone can do to force the system to offer it to you again. There’s also no way to predict if/when the system will deem you worthy again.”

PayPal Pay Later Pros

- Works at millions of online retailers with a familiar checkout experience

- Pay in 4 offers true interest-free installments over six weeks

- Multiple repayment options, including longer terms via Pay Monthly

- Transparent dashboard shows APR, schedule, and monthly payments upfront

PayPal Pay Later Cons

- Denials are common with Pay Monthly, even for longtime PayPal users

- Interest rates on longer terms can be steep

- Not as predictable as other BNPL providers, with easier approvals

- You may not even be able to find it.

Quick Guide

- 🐢This one’s for you if: you’re a tortoise—steady, cautious, and looking for a short-term interest-free buffer without surprises.

- 🐉 Skip it if: you’re a dragon chasing big-ticket purchases—Pay Monthly plans can hit you with high interest or rejection.

Bottom Line

PayPal Pay Later is a strong BNPL option for small-to-mid purchases, especially if you’re already a PayPal user. But between the risk of denial and the high APRs on longer financing, it’s not the most reliable choice for covering large purchases.

PayPal Pay Later

7: Shop Pay Installments — Shopify’s Built-In BNPL

If you’ve shopped online in the past few years, you’ve probably seen the Shop Pay button pop up. It’s Shopify’s one-click checkout, but now they’ve layered in Shop Pay Installments, a buy now, pay later service that lets you split purchases instead of paying the full purchase price up front. I tested it on a couple of online stores and found it to be both convenient and a little sneaky in how it pushes you to spend more.

Shop Pay Installments is powered by Affirm, but it lives inside Shopify’s checkout system. That means if a store uses Shopify, you might see the option to:

- Pay in 4: Four interest-free payments over six weeks (the classic BNPL setup).

- Monthly payments: Extended monthly installments (3–12 months, sometimes longer) with interest rates that can range from 0% to about 36% APR.

- Down payment: Usually 25% due at checkout, followed by the chosen plan.

Shop Pay uses a soft credit check for the short-term “Pay in 4,” but if you go for the extended financing plan, you could trigger a hard credit inquiry.

I tried Shop Pay Installments on a boutique skincare order. The four interest-free payments worked seamlessly; I just hit the purple button, and it auto-filled everything from my saved details. Honestly, it was one of the fastest BNPL checkouts I’ve done.

But here’s where it gets tricky: when I tested a larger purchase amount (a $1,200 furniture cart), Shop Pay nudged me toward the monthly financing plan instead of the simple Pay in 4. The monthly plan was tempting because it spread payments out over a year, but the variable APR would’ve had me paying over $300 extra in interest charges. It felt a little predatory, similar to some of the high-APR offers I saw inside Affirm’s standalone app.

So yes, it’s fast, but you have to read the fine print before hitting confirm.

Shop Pay Installments Pros

- Ultra-fast checkout if you’re already using Shop Pay

- Choice between four interest-free payments or longer monthly plans (Affirm-backed)

- Works across thousands of online retailers that use Shopify

- Push notifications and emails make it easy to track dates and avoid missed payments

Shop Pay Installments Cons

- Longer monthly plans often come with high interest rates

- Not all in-store purchases support Shop Pay; it’s mostly online

- Easy to overspend since checkout is so frictionless

Quick Guide

- 🐇 This one’s for you if: you’re a rabbit—quick, impulsive, always on the go. You’ll love the fast checkout and short six-week plan.

- 🐻 Skip it if: you’re a bear—big appetite, big purchases. Those long monthly financing plans can turn into expensive debt caves if you’re not careful.

Bottom Line

Shop Pay Installments is a slick way to split purchases at checkout with your favorite online stores, especially if you stick to the interest-free installments. But treat those extended monthly payment structures with caution! They look cozy until you realize how much extra you’ll pay in interest.

Shop Pay

8. Synchrony Pay Later — Straightforward but Limited

Synchrony isn’t new to financing—they’re the company behind tons of store credit cards—but their Pay Later product is their take on BNPL. It’s offered at select participating retailers and comes in two flavors:

- Pay in 4: Four equal interest-free payments over six weeks. No interest, no fees.

- Pay Monthly: Equal monthly installments with interest rates anywhere from 0% up to 34.99% APR, depending on your credit and the loan term you choose. Late fees may also apply ($25 or the scheduled payment, whichever is less).

On paper, that sounds flexible. You can finance everyday items or high-ticket purchases through their marketplace, and approval decisions are instant. But in practice, I found it more rigid than services like Sezzle or Klarna. The Pay in 4 option works fine—nothing groundbreaking, just four interest-free chunks.

The Pay Monthly side is where things get dicey: the APR can get steep, and unlike Affirm (which at least shows you multiple offers), Synchrony felt more opaque about where I could actually use it.

Synchrony Pay Later Pros

- Offers both Pay in 4 (no fees, no interest) and longer Pay Monthly options

- Predictable, equal payments for budgeting

- Backed by a major financing company (Synchrony), so it’s stable

- No late fees on Pay in 4 loans

Synchrony Pay Later Cons

- High APR on monthly plans (up to 34.99%), making it less competitive

- Availability is limited to participating retailers

- Late fees apply to monthly loans

- Lacks perks of other BNPL providers (like Sezzle’s credit reporting or Klarna’s rewards)

Quick Guide

- 🦉 This one’s for you if: you’re an owl who likes predictable payments and want a no-surprise Pay in 4 plan.

- 🦈 Skip it if: you’re a shark circling big-ticket buys—Synchrony’s monthly plans can hit hard with high APRs compared to Affirm or PayPal.

Bottom Line

Synchrony Pay Later is fine for smaller purchases through the Pay in 4 option, but if you’re shopping for something big, the high interest on monthly financing makes it less appealing than Affirm or even Amazon’s card-based plans.

Synchrony

9: Splitit — Use Your Credit Card Wisely

Splitit is a little different from most BNPL apps. Instead of opening a new line of credit, it uses your existing credit card to break purchases into smaller monthly installments. That sounds convenient at first—no new account opening, no hard credit check—but in practice, I found it to be more limiting than helpful.

Here’s how it works: when you check out at a merchant that supports Splitit, the full purchase amount is authorized on your card. That amount is held as a pending charge against your available credit. Each month, Splitit releases one installment, which is billed like a normal credit card payment. If you’re on a “Retail Plan,” you won’t pay extra fees or interest to Splitit itself—just your card issuer’s terms apply. But if you’re routed into “Splitit Financing,” that’s where finance charges can appear, with APRs that can go as high as 36% depending on your state.

The problem?

You need enough available credit to cover the entire purchase amount upfront, even though you’re only paying installments over time. That defeats the purpose for anyone already tight on credit. It also means you’re not building positive credit history like you might with Sezzle’s credit bureau reporting.

And there are other headaches. Users report delays, order issues, and even merchants refusing to ship until “billing problems” with Splitit are cleared up. It has even been compared to a “loanshark middleman,” while others described orders being held up for weeks.

Splitit Pros

- No new loan or hard credit check; uses your existing credit card

- Retail Plans can mean no added fees or interest (beyond what your card charges)

- You keep your card’s perks: rewards, fraud protection, and insurance

Splitit Cons

- Requires full available credit upfront—locks up your card balance as a pending hold

- Limited to certain merchants, and many states restrict Splitit Financing

- APR on financing plans can climb up to 36%

- Multiple Reddit reports of glitches, billing issues, and delayed orders

Quick Guide

- 🦅 This one’s for you if: you’re an eagle with plenty of available credit who wants to spread payments while still racking up credit card points.

- 🦡 Skip it if: you’re a badger digging around for flexibility—Splitit ties up your card balance, offers little forgiveness, and feels more like a workaround than a true BNPL service.

Bottom Line

I mention Splitit here because technically it offers installment payments with no added Splitit fees on Retail Plans, but it feels like a clunky middle step. You’re still on the hook to your credit card company, and unless you have a large credit line, it’s just not practical. With all the restrictions, holds, and bad customer reports, I don’t see Splitit as a serious alternative to Sezzle, Klarna, or Affirm.

Splitit

10: Amazon Monthly Payments — Only Worth It with the Amazon Card

Amazon does technically have a BNPL setup, but here’s the truth: it’s not all that great unless you also have the Amazon Store Card.

Here’s my real-life example. My daughter’s cat destroyed my old down comforter (RIP cozy nights), so I went shopping for a replacement. At checkout, Amazon showed me installment options:

- Amazon Store Card — 0% APR, $23.17/month for 6 months.

- Affirm — $13.97/month for 12 months, but with 10–36% APR (so you pay more overall).

- Synchrony — Similar deal, high interest baked in.

See the pattern? If you’ve got the Amazon card, you win: you can split the purchase into monthly payments with no interest charges at all. But if you don’t, you’re stuck with the outside providers (like Affirm), which quickly tack on interest. In the screenshot above, that “$28.65 or less in interest” didn’t sound like much, but it added up to almost $30 on a $140 comforter. Suddenly, it didn’t feel like such a deal.

Amazon Monthly Payments Pros

- Seamless checkout—no separate BNPL app to download

- 0% interest with the Amazon Store Card (the only real sweet spot)

- Clear breakdown of the monthly payment structure before you click “Buy”

Amazon Monthly Payments Cons

- Limited item availability (electronics, home goods, Amazon devices)

- If you don’t have Amazon Store Card, you’re getting Affirm/Synchrony with high APR

- No way to reschedule payments or earn rewards

- Doesn’t help your credit score

Quick Guide

- 🐕 This one’s for you if: you’re a golden retriever who shops on Amazon all the time and already has the Amazon Store Card—because then it’s simple, interest-free, and makes sense.

- 🐍 Skip it if: you’re stuck with Affirm or Synchrony instead—those high-interest plans can sneak up and squeeze your wallet.

Save $15 on Your First Amazon Purchase via Sezzle App

Bottom Line

Amazon Monthly Payments looks like a BNPL perk, but unless you have the Amazon Store Card, it’s not much of a deal. With the card, splitting a down comforter into six painless, 0% monthly chunks is actually worth it. Without it? You’re better off using Sezzle or Klarna for more flexible, interest-free installments.

Amazon Monthly Payments

BNPL Faceoffs: Which BNPL App Fits Your Life?

Everyday Groceries, Gas, and Small Purchases → Sezzle

This is the one I grab when my budget needs quick breathing room without piling on debt. Four interest-free payments, plus Sezzle Up to build credit history. It’s the most reliable daily tool in the lineup.

- Sezzle vs. Afterpay: Both split purchases into four, but Sezzle lets you reschedule once for free and even build credit. Afterpay dings harder with late fees and reported credit drops. Sezzle wins for flexibility and safety net; Afterpay wins for speed.

Back-to-School Tech or Last-Minute Electronics → Klarna

Klarna saved me when my daughter needed an iPad for college. I got it instantly, but paid about $30 in interest. Worth it in a pinch, but not something I’d lean on for constant purchases.

- Klarna vs. Zip: Klarna gives you perks, rewards, and better store coverage. Zip is handy anywhere Visa is accepted, but the flat $1 fees add up. Klarna wins for polish; Zip wins for versatility.

Big-Ticket Travel or Furniture → Affirm

When flights or couches are on the table, Affirm stretches the payments for months (sometimes years). Just watch the APR—some plans are steep, but if you snag a 0% offer, it’s a lifesaver.

- Affirm vs. Synchrony Pay Later: Both offer longer monthly plans, but Affirm is clearer about rates upfront and skips late fees. Synchrony can go up to 34.99% APR with added late fees. Affirm wins here, hands down.

Impulse Buys and Concert Tickets → Afterpay

Need something fast? Afterpay’s approval is lightning-quick. I used it for tickets, and it worked like a charm—just don’t miss a payment, or the late fees and credit ding will bite.

- Afterpay vs. PayPal Pay Later: Afterpay approves in seconds and feels effortless, but late fees hit hard. PayPal Pay Later gives more repayment flexibility and the trust of an established platform. Afterpay wins for speed; PayPal wins for stability.

In-Store Purchases Anywhere Visa Is Accepted → Zip

Zip’s virtual card makes it versatile, but the flat $1 fee per installment adds up. Handy as a backup tool when Sezzle or Klarna don’t show up at checkout.

- Zip vs. Sezzle: Both work anywhere Visa is accepted, but Zip charges a $1 fee on every installment while Sezzle keeps it fee-free and even helps build credit with Sezzle Up. Sezzle wins outright—Zip can’t match the value.

Amazon Shoppers (with the Amazon Store Card) → Amazon Monthly Payments

Here’s where it finally makes sense. When I replaced my cat-destroyed down comforter, Amazon showed me $23.17/month for six months at 0% APR with the store card—smooth and painless. Without the card? You’re stuck with Affirm or Synchrony’s high-interest plans, which aren’t worth it.

- Amazon Monthly Payments vs. Affirm: Both show up at Amazon checkout, but only the Amazon Store Card keeps it at 0% APR. Affirm usually tacks on interest. If you don’t have the card, skip Amazon’s financing and use Sezzle elsewhere.

How I Ranked the Best BNPL Apps

I independently evaluated 10 major Buy Now, Pay Later (BNPL) providers using a data-driven and hands-on approach. Each platform was tested through real purchases, account setup, and customer support interactions to see how they perform in real-world use—not just on paper.

Then I scored every app across six weighted categories (totaling 100%), focusing on cost, flexibility, credit impact, and user experience.

| Category | Weight | What Was Measured |

|---|---|---|

| Total Cost of Ownership | 30% | APRs, late fees, service fees, and overall payment transparency. |

| Flexibility & Coverage | 20% | Payment options (Pay-in-4 or monthly), in-store use, and merchant availability. |

| Credit Impact & Eligibility | 15% | Whether apps perform soft or hard credit checks, and if they report on-time or missed payments. |

| Consumer Protections | 15% | Dispute resolution, refund speed, payment rescheduling, and hardship policies. |

| Merchant & Ecosystem Support | 15% | How widely accepted the service is, and how well it integrates with major retailers. |

| App Reliability & User Experience | 5% | App stability, clarity of repayment timelines, customer support quality, and ease of use. |

To ensure accuracy and trust:

- All pricing and terms were verified from each provider’s official website and disclosures.

- We prioritized firsthand testing and verified terms over anecdotal user feedback.

Our rankings reflect how each BNPL service performs for everyday shoppers, not just in ideal conditions. The result: a clear, balanced picture of which apps truly make budgeting easier—and which could cost you more in the long run.

Bottom Line

BNPL apps can be either a budgeting ally or a financial trap, depending on how you use them.

- Sezzle takes the crown for everyday purchases because it’s transparent, manageable, and even helps you build credit.

- Klarna and Affirm shine when you need flexibility for bigger buys—but Klarna tempts overspending, and Affirm’s APR can sting.

- Afterpay and Zip are fine for quick grabs, but don’t slip up, or you’ll pay the price.

- PayPal and Shop Pay are great if you’re already using them, though they’re unpredictable and interest-heavy long term.

- Synchrony Pay Later works for small Pay in 4 plans, but the monthly version is less competitive.

- Splitit is more of a credit card trick than a true BNPL.

- Amazon Monthly Payments only makes sense with the Amazon Store Card—otherwise, it’s just expensive Affirm in disguise.

Use BNPL for breathing room, not long-term debt. Sezzle is my everyday favorite, Klarna is my flashy backup, and Affirm is the elephant I call in only when the load is too heavy to carry alone.

FAQ

BNPL apps let you split purchases into multiple smaller payments instead of paying the full cost upfront. The most common plan is “Pay in 4,” which typically requires 25% at checkout and the rest in three bi-weekly, interest-free installments.

Sezzle is often recommended because it offers interest-free installments, allows one free reschedule per order, and even has Sezzle Up, which reports payments to credit bureaus to help build credit. Klarna, Afterpay, and PayPal Pay Later are also popular, but each has pros and cons depending on your shopping habits.

It depends. Many short-term Pay-in-4 plans are interest-free if you pay on time. But some providers (like Affirm, Synchrony, or Klarna on longer plans) can charge interest. Others, like Zip, add small fees to every installment, which can add up if you juggle multiple purchases.

Most BNPL apps don’t report on-time payments to credit bureaus, so they won’t build credit. Sezzle is an exception with its Sezzle Up program. Late or missed payments, however, can hurt your credit if reported (Afterpay has been criticized for this).

Consequences vary by app. Some charge late fees (Afterpay and Zip can be strict), others reduce your spending limit, and some may report the missed payment to credit bureaus, hurting your score. A few apps like Sezzle give you one free reschedule as a safety net.

BNPL plans can be cheaper for short-term, interest-free purchases if you pay on time. Credit cards, however, usually offer rewards and fraud protection — plus you can build credit with responsible use. The downside is higher average interest rates (over 20% APR) if you carry a balance.

Yes, BNPL apps are generally safe when used responsibly. They partner with major retailers and offer secure payment methods. The bigger risk is overspending — because splitting payments makes purchases feel more affordable than they are.

Both. Apps like Afterpay, Zip, and Klarna offer virtual cards you can add to Apple Pay or Google Pay, so you can use them in stores wherever Visa or Mastercard is accepted. PayPal Pay Later and Shop Pay are more commonly used for online checkout.

Pay-in-4 plans split your purchase into four equal payments over six weeks, usually interest-free. Monthly financing spreads payments over 3 to 60 months but often includes interest charges.

Avoid options that tack on hidden fees or high APRs for extended financing. For example, Zip adds a flat $1 fee per installment, and Affirm’s interest can climb above 30% on some plans. If you want the simplest and most transparent option, Sezzle and Afterpay’s Pay-in-4 are safer choices — as long as you never miss a payment.