Klarna has become one of the most recognized BNPL apps, with over 31 million active monthly users in 2024. The company is known for its mix of four interest-free payments, monthly installments, and even a paid membership that unlocks cashback perks. Furthermore, Klarna is widely accepted at online retailers and also supports in-store purchases through Apple Pay or Klarna’s own card.

Still, Klarna isn’t the only BNPL service available if you’re looking for the top pick for flexible payments. In fact, some argue that Klarna’s competitors may be a better choice for your pay-later provider. In this guide, I’ll look at some top alternatives—including Sezzle, Afterpay, and Affirm—to see how they stack up, and help you choose the best app for your needs.

Key Takeaways

- Klarna Isn’t One-Size-Fits-All: It offers Pay in 4, Pay in 30, and monthly financing, giving shoppers multiple ways to manage purchases.

- Membership Matters: Klarna’s paid tiers add perks like cashback, waived fees, and store discounts that set it apart from other BNPL apps.

- Competitors Shine in Different Areas: Sezzle helps with credit building, Afterpay emphasizes simplicity, and Affirm focuses on long-term financing.

- Limits Aren’t Always Transparent: Klarna’s “purchase power” can feel unpredictable compared to fixed spending caps from other providers.

- BNPL Requires Discipline: While these apps smooth out expenses, missed payments may lead to fees, collections, or damaged financial health.

Klarna: A Flexible Leader in BNPL

Klarna is one of the most popular BNPL services, offering a mix of short-term interest-free installments and longer-term financing. Shoppers can choose between four interest-free payments, a “Pay in 30” option, or monthly installments with interest for bigger purchases. Klarna also has paid memberships that unlock perks like cashback and fee waivers, and it integrates with Apple Pay for a seamless payment process both online and in stores.

Pros

- Various payment plans: Pay in 4, Pay in 30, or monthly financing

- Soft credit check only for most purchases

- Can use a credit or debit card, bank account, or Apple Pay

- Extra perks through Klarna’s paid membership tiers

Cons

- Spending limits are unpredictable (“purchase power” is automated)

- Some merchants add hidden fees unless you pay with Klarna’s card

- Monthly financing includes interest charges and stricter terms

Sezzle: Credit-Building Potential

Sezzle offers interest-free installments through Pay in 2 or Pay in 4 plans, making it simple to split payments into manageable installments. It also stands out for its Sezzle Up feature, which lets you build credit by reporting on-time payments to the bureaus. One Reddit reviewer hypes up their spending limit, explaining,

See a more detailed comparison of Klarna and Sezzle here.

“Hands down sezzle by far! I’ve had it since 2016 never missed a payment on anything and have $4000 limit now for years with them. They own the zip one too but zip is nowhere near as good as sezzle.”

Pros

- Flexible payment plans (2, 4, or long-term monthly)

- Credit-building option with Sezzle Up

- Works with a debit card or linked traditional payment methods

Cons

- Fees for rescheduling, failed payments, or convenience add-ons

- Starting spending limits are very low and grow slowly

Afterpay: Straightforward and Predictable

Afterpay keeps it simple: make an upfront payment at checkout, then cover the balance in four equal installments. There are no interest fees for on-time payments, though you may pay a late fee capped at 25% of your order if you fall behind.

Pros

- Always free when you pay on time

- Widely accepted at online retailers and stores via the Afterpay Card

- Clear fee structure and capped late fees

Cons

- Spending limits start low, and approval isn’t guaranteed

- The Pay Monthly option comes with interest rates and a required credit check

Affirm: Longer-Term Financing

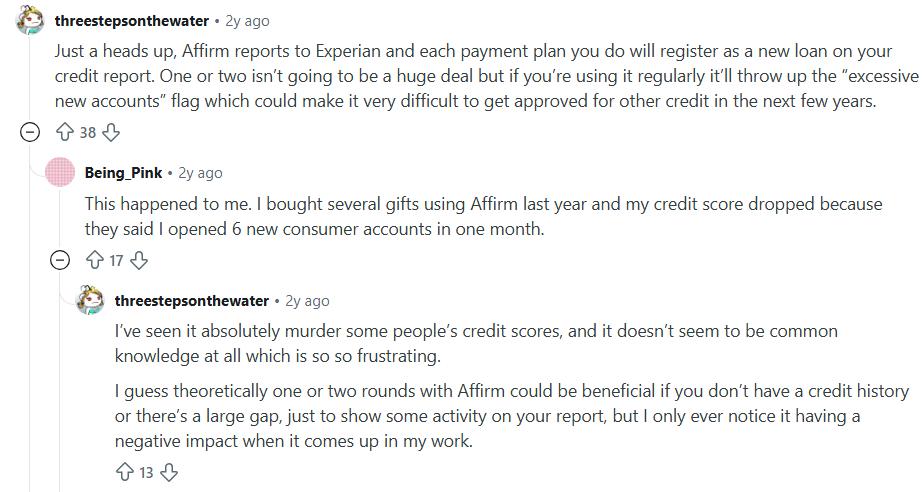

Affirm differs from Klarna by leaning more heavily into long-term monthly installments. Depending on the purchase, Affirm may charge interest fees, but there are never late fees, which can make it easier to manage cash flow responsibly. However, the credit reporting can get excessive. Here’s a quick breakdown from Reddit, but keep in mind these are years-old posts (and naturally, you have to take everything from Reddit with a grain of salt):

Pros

- Transparent pricing with no hidden fees

- Can finance large purchases with 3–60 month loans

- Integrates with PayPal Credit and other BNPL services

Cons

- Interest can make it expensive for smaller purchases

- Requires a down payment in some cases

PayPal Pay Later: A Familiar Option

If you already use PayPal to shop online, their BNPL service is built right in. It offers Pay in 4 for smaller purchases and a deferred interest option for larger ones, giving you a familiar interface with a wide acceptance network.

Pros

- Seamless payment process inside your PayPal account

- Broadest reach since PayPal is accepted almost everywhere

- Pay in 4 has no interest charges if paid on time

Cons

- Deferred-interest plans can backfire if you miss the payoff window

- Customer service is less specialized than Klarna or Affirm

Final Thoughts: Klarna and Beyond

If you value choice and flexibility, Klarna is still one of the strongest BNPL apps around, offering everything from split payments to long-term loans. But Sezzle, Afterpay, Affirm, and PayPal Pay Later each bring something unique — whether it’s credit-building, predictability, or broader merchant acceptance.

No matter which service you choose, keep in mind that financial responsibility matters most. These tools can help smooth out expenses and free up cash flow, but missing payments can mean fees, interest, or even a hit to your credit.

FAQs

Sezzle is closest in terms of offering short-term, interest-free installments, though it adds a credit-building feature that Klarna doesn’t provide.

Sezzle’s ability to report on-time payments through Sezzle Up makes it a good choice for shoppers who want their BNPL use to support long-term financial health.

Afterpay keeps things simple with just four equal installments or a flat monthly payment, while Klarna offers more varied payment plans like Pay in 30 and long-term financing.

Affirm leans into longer monthly installments, sometimes with interest charges, whereas Klarna is better for short-term flexibility and rewards.

Klarna has the most flexible payment plans, but Sezzle stands out for credit building, and PayPal Pay Later adds convenience for frequent online shoppers.