If there’s one area where I can confidently say I’ve earned the crown, it’s travel now, pay later. Over the years, I’ve used just about every buy now, pay later service imaginable—Sezzle, Affirm, Klarna, you name it, even the lesser-known flex pay options—to fund my adventures.

From family road trips to my honeymoon in Greece, these flexible payment plans have helped me see the world without draining my bank account all at once.

I don’t use BNPL out of desperation; I use it because it works. For travelers who plan carefully, it’s a tool for freedom, flexibility, and smarter budgeting. Keep reading to learn more about the flex pay process, plus my top tips for traveling on a payment plan.

Key Takeaways

- BNPLs make travel possible without huge upfront costs. Book flights, hotels, and excursions with flexible payment methods like Sezzle, Affirm, or Uplift.

- Expect some interest or small fees. Rates vary depending on provider, loan amount, and credit information.

- Perfect for planned, not impulsive trips. Use it to manage travel expenses strategically—not as a last-minute bailout.

- Stay organized. Keep track of your payment dates and set reminders to avoid late fees.

- Great for big purchases. Whether it’s a honeymoon in Greece or a family getaway, buy now, pay later travel can help you budget smarter without giving up adventure.

How Travel Now, Pay Later Works

BNPL platforms make travel more accessible by breaking down your purchase price into smaller installment payments over time, usually with fixed monthly payments or four easy pay-over-time options. Instead of paying hundreds or thousands upfront for an airline ticket, hotel, or excursion, you can spread the cost into manageable chunks.

During checkout, many travel sites—like Expedia, CheapOair, United Airlines, and Alternative Airlines—offer BNPL options right beside traditional credit card or debit card payments. Once you simply select Flex Pay or the buy now, pay later option, the platform performs a soft credit check and provides you with an instant approval decision. So while it might sound a little complicated, the actual process is pretty quick and easy.

That’s how many travelers do it—booking now and paying later as their trips approach. Personally, I like to plan it a little differently. I prefer to have my travel budget and Sezzle allowance settled ahead of time; that way, I know exactly how much I can spend before I book.

For example, if I have a $1,000 budget and a Sezzle line to match, I’ll map that out in advance. When I’m ready to book, I can just enter my Sezzle details at checkout and stay perfectly on track with my spending plan.

This method gives me the same flexibility BNPL offers, just with more intention and zero post-vacation regret.

Each service works a little differently:

- Affirm offers longer-term financing (often 3–12 months) with clear APR ranges and no prepayment penalties.

- Uplift partners directly with airlines like United and provides monthly plans timed to your departure date.

- Sezzle Anywhere uses a virtual card to pay any travel vendor that accepts Visa, perfect for flights, hotel stays, or experiences.

- Klarna gives flexible pay later options and sometimes rewards users with points or cashback on purchases.

Step-by-Step: How to Use BNPL for Travel

If you’ve never tried buy now, pay later for travel, it’s simpler than most people think. Here’s exactly how I do it:

- Set your travel budget first. Decide what you can realistically budget for your upcoming trip. For me, that’s often around $1,000–$1,200 depending on destination and timing.

- Check your BNPL spending limit. Before booking, I log into a BNPL account like Sezzle or Affirm to see my available line. This gives me a clear picture of what I can charge now and what my payment schedule will look like later.

- Plan the mix. I usually reserve my line for flights or deposits and handle hotels or extras separately. For example, if I have a $1,000 Sezzle allowance, I’ll apply that strategically to the biggest purchase—like airfare—so my travel foundation is secure.

- Go to checkout. On sites like Expedia, CheapOair, or Alternative Airlines, choose the buy now, pay later or Flex Pay option at checkout. If I don’t see the BNPL I want, I generate a one-time-use virtual card and enter it like a regular Visa at checkout. It works seamlessly for bookings that don’t list Sezzle as a payment method.

- Track your payments. Once booked, I immediately check both dashboards (travel site and BNPL app) to verify the total cost, payment dates, and reminders.

- Pay early when possible. I often pay off the balance ahead of schedule. This not only keeps my credit healthy but also resets my allowance faster for my next trip.

The Bigger Conversation Around BNPL Travel

The idea of using buy now, pay later for travel is no longer niche; it’s becoming a cultural talking point on social threads. According to CNBC, nearly one in five American travelers plans to use a BNPL service for their vacations this year. Apps like Klarna and Affirm report record growth—Klarna’s travel bookings jumped 50%, and Affirm’s travel and ticketing volume topped $1 billion in late 2024.

For many, the appeal is instant relief. “It felt like a lifesaver,” said Kristin Herman, who used BNPL for a last-minute Miami trip. But when she missed a reminder, “one skipped payment turned into fees.” Others, like Rane Teo, describe their experience as “easy and convenient,” having used BNPL to split the cost of a family stay in Indonesia into three monthly installments.

Those two stories capture the divide perfectly. BNPL can be a tool for freedom or a fast track to frustration depending on how it’s managed.

Why Travelers Are Doing It

- Accessibility: Quick approvals, soft credit checks, and the promise of no upfront cost make it simple to say yes.

- Flexibility: Spreading payments can ease short-term strain, especially after price jumps or unexpected life expenses.

- Mindset shift: Many Gen Z and younger millennial travelers view experiences as investments in joy and identity rather than luxuries.

And Why Some People Worry

Critics warn that the trend can disguise financial strain. Comments in the same thread show real concern:

- “Never go into debt for your vacation. How can anyone relax with debt hanging over them?”

- “It’s easy to be okay with more debt when you’ve grown up financing everything—student loans, phones, even clothes.”

- “I’m not against installments if there’s no interest, but if it starts adding up, that’s not a break—it’s a burden.”

There’s also a generational divide. Some commenters note that Gen Z is simply using the tools they were raised with. For some, BNPL feels more natural than credit cards. Others argue it reflects a culture that expects instant gratification and prioritizes now over later.

My Real-Life Travel BNPL Experiences

I’ve tested nearly all of them—and not just in theory.

- CheapOair Flight Booking: My total was $933.50, financed through Affirm with a 29.94% APR, bringing the total to $1,086.28. While the interest was steep, it allowed me to book a trip without touching my emergency savings.

- Expedia Hotel: I financed $631.90 with 29.99% APR, totaling $686.80. The rate wasn’t ideal, but it gave me low monthly payments and time to spread out the expense before my trip.

- Sezzle (Homeymoon Travel): My total came to $524.47, including an $8.49 fee. This one was for my honeymoon, and I loved how simple it was—surprise, free monthly payments, zero stress, and full transparency.

These examples highlight how flexible BNPL really is. Whether it’s booking a flight ticket, hotel, or experience, there’s almost always a pay later option available if you know where to look.

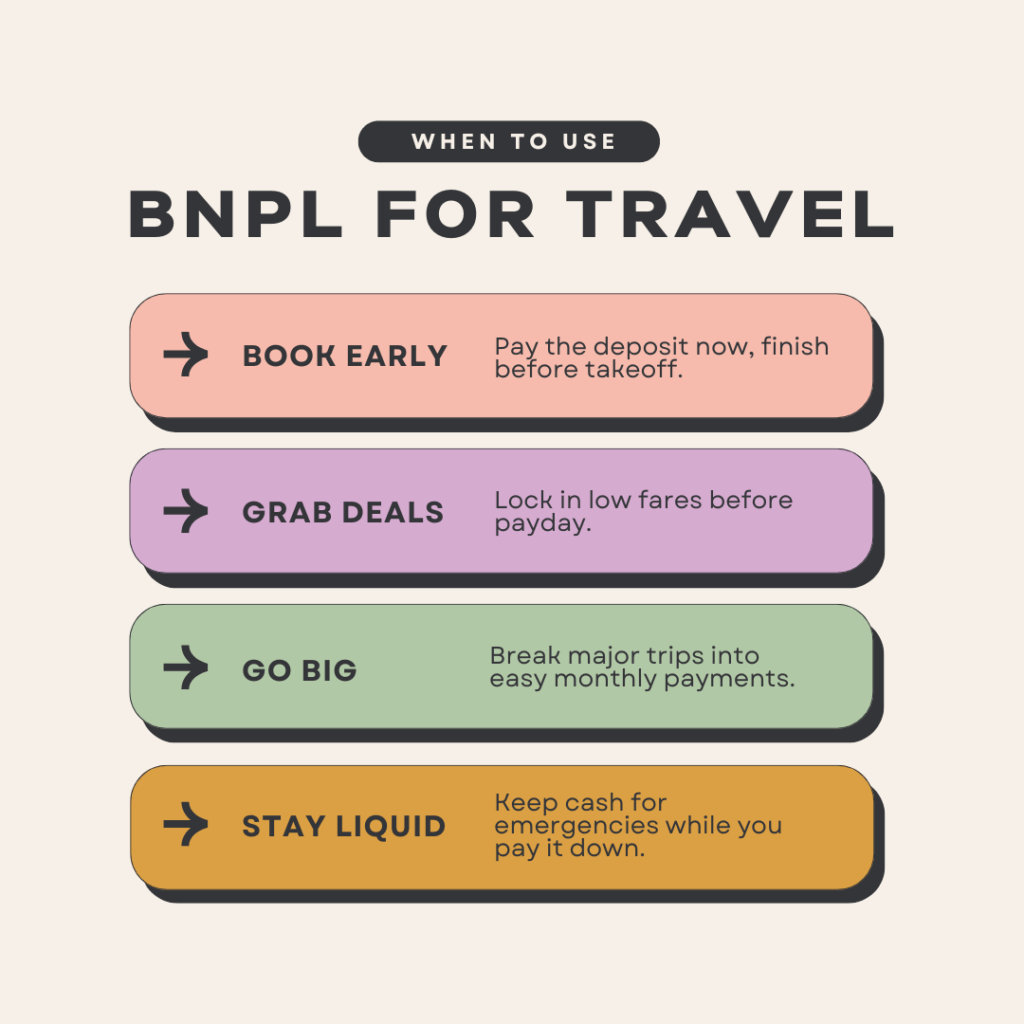

When to Use Travel BNPL—and When Not To

BNPL can be a powerful budgeting tool, but it’s not for everyone or every trip. Here’s when it makes sense:

- You’re booking early. Split your down payment and pay off your balance before your departure date.

- You find a great fare. Lock in your flight before prices rise, even if your next paycheck hasn’t hit yet.

- You’re planning a big vacation. Using a monthly plan helps make large travel expenses more manageable.

- You’re protecting your cash flow. Keeping some cash in reserve for emergencies while paying off your trip gradually can reduce stress.

- You’re confident about your payment dates. If you’re organized and make on-time payments, BNPL can be seamless.

Avoid BNPL if you’re uncertain about your budget, struggle with late payments, or tend to overspend when options feel too easy. The key is intentional use, not impulse booking.

What to Watch Out For

- Interest Rates: As my CheapOair and Expedia examples show, some loans can carry high APRs (near 30%). Read the actual terms carefully.

- Fees and Late Charges: While many services promise no surprise fees, missed payment dates can trigger late fees or affect your credit score.

- Eligibility: Most services require you to be a U.S. resident, provide basic information like your Social Security number and mobile number, and be at least 18.

- Short Application ≠ Free Money: BNPL makes travel easier, but it’s still a loan—so borrow responsibly.

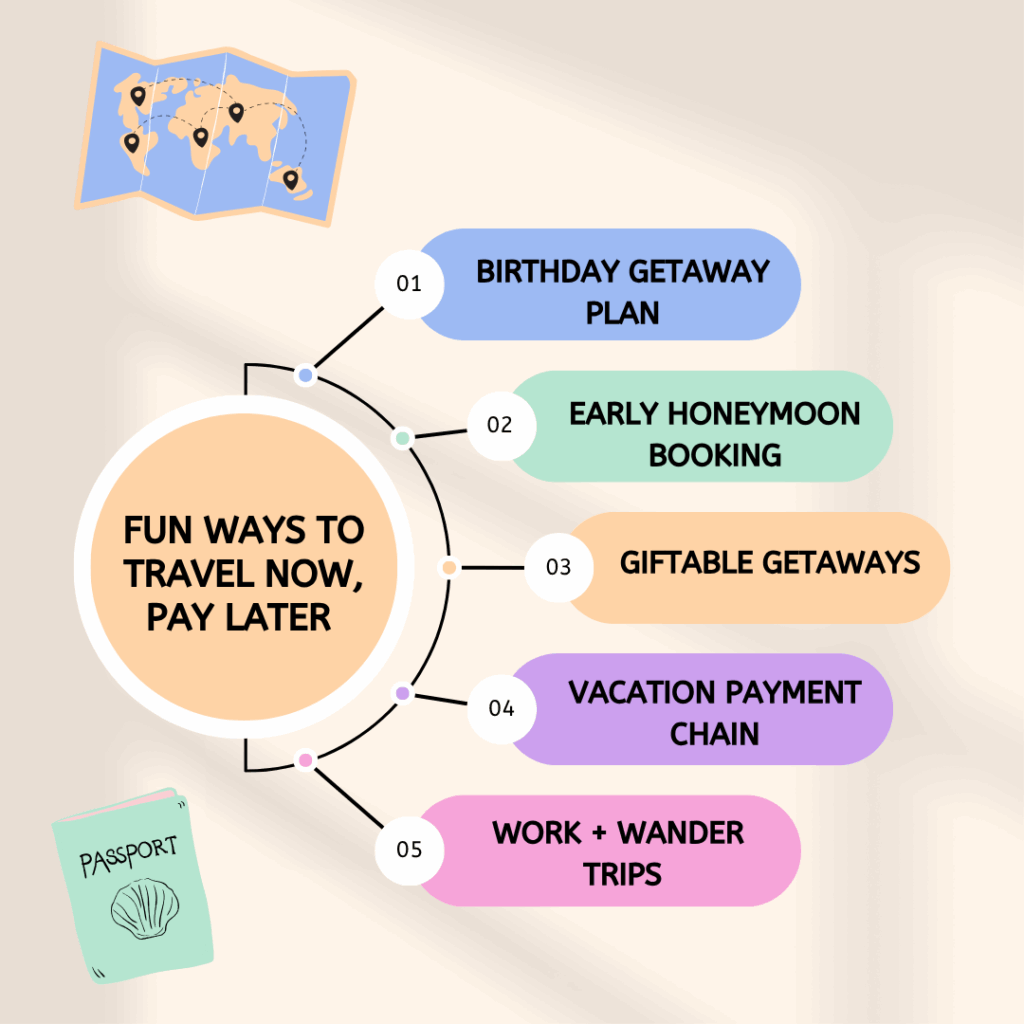

Fun Ways to Travel Now, Pay Later

Here’s where it gets creative, because buy now, pay later travel isn’t just for airfare and hotel rooms. If you’re strategic, you can use it to build full experiences and even surprise someone you love.

- Plan a Birthday Getaway: Use Sezzle for a small Airbnb or boutique stay and Affirm for flight tickets, making the whole trip payable in comfortable installments.

- Book Your Honeymoon Early: I used BNPL to pay for my Greece flights, which let me snag a great fare months in advance without emptying savings.

- Create a “Mini-Moon” or Weekend Escape: Use Klarna’s virtual card for travel purchases like gas, food, or local tours, then pay over time.

- Build a Vacation Payment Chain: Use Sezzle for buying flights, Affirm for hotels, and pay for excursions in four easy payments with Uplift. It’s like building your trip one layer at a time, stress-free.

- Gift Travel Instead of Things: Surprise a loved one with thoughtful purchases like prepaid flights, a hotel reservation, or other thoughtful purposes, and quietly handle it on a monthly plan behind the scenes.

- Content or Business Trips: For travel bloggers, photographers, or creators, BNPL lets you invest in travel-related projects without upfront strain. Just plan around your payment schedule.

The trick is mixing practicality with pleasure. BNPL gives you room to make spontaneous memories without financial regret.

Bottom Line

At the end of the day, travel now, pay later isn’t about escaping responsibility. Instead, it’s about creating more room to live your life while staying within your means. While not everyone will need it for an upcoming trip, for me, it’s never been about “winging it” financially; it’s about intentional flexibility.

That’s why I love using Sezzle. It gives me a way to plan ahead, stay organized, and still enjoy the freedom to book a trip when the timing feels right. Whether it’s a long-awaited honeymoon or a quick weekend getaway, Sezzle’s four easy payments and transparent no-interest options make it simple to explore the world without the stress of big upfront costs.

So yes—I may be the queen of travel now, pay later, but I’m also proof that with a little planning and a helpful BNPL tool like Sezzle, adventure doesn’t have to wait until your next paycheck.

FAQs

Yes. Many travel websites and booking platforms like CheapOair, Alternative Airlines, and Expedia let you select Affirm or Sezzle during checkout. Affirm works best for larger trips with longer monthly plans, while Sezzle is ideal for smaller travel purchases paid over six weeks.

Most services use a soft credit check, meaning it won’t impact your credit score. However, lending partners like Affirm may perform a hard check for larger amounts or longer-term loans.

It depends. Some buy now pay later services offer zero-interest options if you pay on time, while others charge APRs ranging from 0% to 36%. Always read your purchase details before confirming.

Missing a payment date can result in late fees or suspension of future BNPL use. Some BNPL providers report missed payments to credit bureaus, so it’s best to set reminders or autopay.

For many travelers—especially families or those balancing multiple expenses—it can be. It offers more flexibility and immediate access to your next trip without major upfront costs. As long as you understand the cost, track your payments, and book responsibly, it can be a fantastic tool for turning your travel plans into reality.