I’ve tried almost every buy now, pay later service—Sezzle, Affirm, Klarna, Afterpay, Zip—and most make it simple: sign up, get approved, and start splitting your payments. Splitit, on the other hand, might be the most confusing BNPL platform I’ve ever attempted to use.

Here’s the kicker: I never even got to use it.

I went to Splitit’s website, ready to create an account, only to find there’s no “sign up” button anywhere. The only option is Manage My Account, which only works if you already have one.

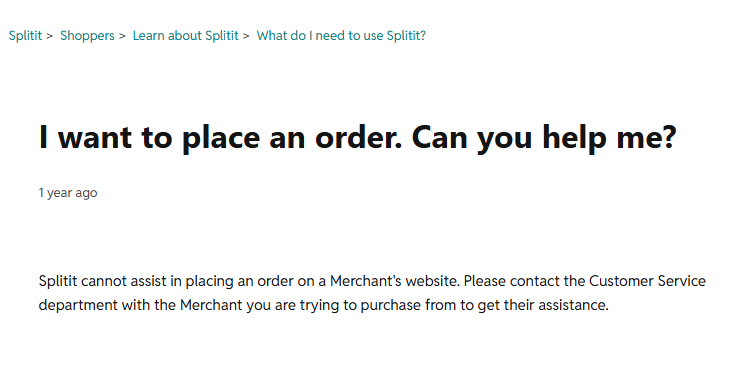

When I checked the FAQs, this line summed it up perfectly:

“Splitit cannot assist in placing an order on a Merchant’s website. Please contact the Customer Service department with the Merchant you are trying to purchase from.”

So basically, you can’t sign up, and they can’t help you buy anything.

Splitit: Best Fit vs. Bad Fit

Who Splitit Might Work For

- Shoppers with plenty of available credit who want smaller monthly installments without opening new financing

- People who want to keep earning credit card rewards or cashback while spreading payments

- Consumers who prefer no new credit checks or applications

Who It Might Not Suit

- Anyone looking for a simple, user-friendly BNPL experience

- Shoppers with limited credit or low available limits

- People who expect clear customer support or easy merchant access

- Anyone who doesn’t want their full credit card statement tied up with authorization holds

Splitit Snapshot

Splitit’s big selling point is that it lets you split purchases into smaller payments using your existing credit card—Visa, Mastercard, or Discover. There’s no hard credit check, no new loan, and no interest on Retail Plans.

Here’s how Splitit works (in theory):

- You shop with a merchant that accepts credit cards/accepts Splitit.

- At checkout, you choose Splitit as your payment option.

- Splitit places an authorization hold on your card for the entire purchase price.

- Each month, it releases one installment plan amount and adjusts the hold accordingly.

It’s marketed as a way to manage cash flow and avoid taking on new debt. But because the entire amount must be available on your card upfront, it’s not exactly freeing up your finances—it’s just moving the money around.

My Attempted Sign-Up: Frustration from the Start

After using dozens of BNPL platforms, I expected Splitit to have a standard onboarding process. Instead, I found myself in a maze. The website looks professional enough, but there’s no way to create an account or get pre-approved. There is also no app. While there is an app with the same name, it is for a totally different purpose (it is a splitting your bill calculator).

When I clicked around, the only button I could find was “Manage My Account.” So, I checked the FAQ—and discovered that Splitit doesn’t actually let customers sign up directly. You have to find a store that offers Splitit at checkout, and even then, Splitit can’t help you place the order.

For comparison, Sezzle and Klarna let you create an account in minutes and shop anywhere online, even generating one-time payment cards for checkout. Splitit’s process feels like it was designed a decade ago and never updated.

It’s not that I don’t understand how it’s supposed to work—it’s that it makes it nearly impossible to test as a consumer without being on a merchant’s website with a full purchase amount and a connection to Splitit.

Where You Can (Sometimes) Use Splitit

Splitit claims to work with select merchants—mainly in high-value categories like electronics, mattresses, and luxury goods—but finding one that actually offers it feels like a scavenger hunt.

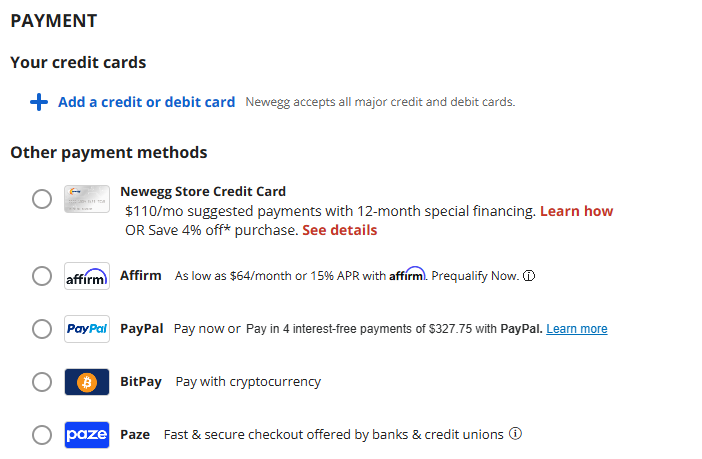

When I googled “Splitit merchants,” I found mentions of stores like Samsung, Purple, Ergomotion, and NewEgg, so I decided to give it a real shot. I went through a mock checkout for a gaming PC on NewEgg, expecting to see Splitit listed alongside other payment options.

Here’s what I actually saw:

The available options included Affirm, PayPal Pay in 4, and even BitPay—but no Splitit. Not in the checkout page, not hidden in fine print, not anywhere.

So despite being listed as a Splitit partner online, NewEgg doesn’t appear to offer Splitit as a real payment option at checkout. And it’s not just them; several other “supported” stores I checked showed the same issue.

It’s frustrating because without an app or directory, there’s no easy way to verify which stores actually use Splitit. You basically have to stumble on it by accident—and even then, there’s no guarantee it’ll still be active when you check out.

The Fine Print: How Splitit Really Works

Splitit doesn’t offer new credit lines or soft credit checks like Sezzle or Affirm. Instead, it uses your existing credit card to split payments into manageable installments.

But that convenience comes with limitations:

- You need enough available credit to cover the full purchase price upfront.

- The purchase appears as an authorization hold on your credit card statement.

- If you miss a payment or can’t cover the balance, your card issuer’s late fees and finance charges still apply.

- Splitit doesn’t report to credit bureaus, so it won’t help you build credit.

What I Learned from Trying (and Failing) to Use It

After exploring Splitit’s site, help center, and partner merchants, I came away thinking it’s a great idea executed poorly.

It’s designed more for businesses than consumers, promoting “higher conversion rates” for merchants rather than convenience for shoppers. From a user perspective, it’s confusing, restrictive, and lacking the flexibility that makes BNPL services so popular.

I wanted to like it. I really did. But when I can’t even create an account or get a clear explanation of how to use it, it’s a no for me.

Pros

- No new credit check or loan; uses your existing card

- Keeps your card’s fraud protection, rewards, and insurance

- Zero interest or fees on standard retail plans

- Works for larger purchases if you have the available credit

Cons

- No direct signup option; must find a merchant that accepts it

- Requires enough available credit for the full amount upfront

- Complicated process and poor user experience

- Limited to certain merchants and industries

- APRs up to 36% on Splitit Financing

- Authorization holds can tie up your credit line

How Splitit Compares to Other BNPL Options

Splitit vs. Sezzle

Sezzle is designed for accessibility. You can sign up instantly, split payments into four or more installments, and even reschedule a payment once per order—no calls, no confusion. Splitit, by contrast, makes you hunt for merchants and requires full credit coverage upfront.

Bottom Line: Sezzle puts the control in your hands; Splitit makes you work for it.

Klarna vs. Splitit

Klarna integrates directly into thousands of online stores and offers everything from short-term pay-in-four to long-term financing. The app is intuitive, packed with features, and easy to manage. Splitit, meanwhile, has no standalone app and no clear signup process.

Bottom Line: Klarna feels like a modern shopping tool; Splitit feels like a merchant back-end feature you weren’t supposed to see.

Affirm vs. Splitit

Affirm is built for transparency. You see your total cost, APR, and monthly payment schedule before you ever click “confirm.” It’s ideal for larger items and doesn’t require a traditional credit card. Splitit’s entire system depends on having enough available credit and navigating confusing holds.

Bottom Line: Affirm gives clarity and confidence; Splitit gives complexity and uncertainty.

Bottom Line: Is Splitit Worth It?

Splitit markets itself as a smarter, more “responsible” BNPL service, but it feels more like a confusing middleman between you and your credit card. It’s not truly buy now, pay later—it’s more like buy now, reserve the funds, and hope it goes smoothly later.

If you already have excellent credit and love the idea of keeping your card rewards while splitting payments, you might appreciate it. But for everyday shoppers who want flexible payment options, easy access, or clear support, Splitit is far from a game-changer. Personally, I’ll stick with BNPL services that actually let me sign up, split payments easily, and manage everything in one app—without feeling like I need a finance degree just to check out.

FAQs

Splitit is a payment platform that lets shoppers split purchases into monthly installments using their existing credit card.

Not on standard Retail Plans, but Splitit Financing may include finance charges or high APRs on the remaining balance, depending on your location.

No. Splitit doesn’t perform or report credit checks to credit bureaus, but your credit card issuer might if you carry a balance.

No. You can only access Splitit through partner merchants, and even the company’s support team can’t assist in placing orders.

Splitit works with Visa, Mastercard, and Discover, depending on merchant availability.

Not really. While Splitit offers zero interest and no new credit payment plan options, it’s confusing, limited, and far less convenient than Sezzle or Klarna.