When back-to-school season hit this year, I promised myself I’d be more intentional with spending. After all, over a quarter of Americans report spending more than what they earn. But between my daughter’s supplies, new shoes, and an unexpected car repair? That budget didn’t last long.

I wasn’t looking to overspend—just to space out payments in a way that didn’t wreck my monthly balance. That’s when I started looking into Buy Now, Pay Later (BNPL) options again.

Two of the most popular? Shop Pay and Sezzle.

Both let shoppers split purchases into interest-free installments, avoid hard credit checks, and pay over time. But they’re built very differently. I spent time researching both platforms, running test purchases, and reviewing how they handle fees, approvals, and credit reporting. Here’s how they compare—and which one fits your lifestyle best.

Quick Pick: Shop Pay or Sezzle?

- Best for Everyday Shoppers on a Budget: 🟢 Sezzle: Ideal for managing multiple purchases across paychecks—especially if you want to avoid interest while keeping your budget flexible.

- Best for Budget Flexibility: 🟢 Sezzle: Lets you reschedule payments, track your spending, and build credit history.

- Best for Frequent Shopify Shoppers: 🟣 Shop Pay: Perfect if most of your favorite online stores already use Shopify Payments.

- Best for Credit History Building: 🟢 Sezzle: Through Sezzle Up, you can report payments to credit bureaus and strengthen your credit payment history over time.

- Best for Fast, Seamless Checkout: 🟣 Shop Pay: Integrated directly into Shopify stores, it’s designed for one-tap checkout with saved details.

Shop Pay vs Sezzle: At a Glance

| Feature | Shop Pay | Sezzle |

|---|---|---|

| Payment Terms | Pay in 4 installments or pay in full (via Affirm) | 4 payments over 6 weeks |

| Interest | None for Pay-in-4 plans | None |

| Credit Check | Soft credit check through Affirm | Soft check only |

| Credit Reporting | No | Yes, with Sezzle Up |

| Late Fees | None directly (Affirm may apply fees for missed payments) | Small fixed fees |

| Flexibility | Minimal | High — reschedule or extend payments |

| Integration | Built into Shopify checkout | Standalone app usable at thousands of retailers |

| Order Tracking | Automatic via the Shop app | In-app payment and order tracking |

| Best For | Convenience and eco-friendly shoppers | Budgeters and credit builders |

What It’s Like to Use Shop Pay

I hadn’t used Shop Pay before this review, so I wanted to experience it exactly as a shopper would. Because you can’t download Shop Pay and sign up as a buyer like you can with Sezzle, I had to do a little research. When I looked up which merchants use it, the first one that appeared was one of my long-time favorites—Steve Madden.

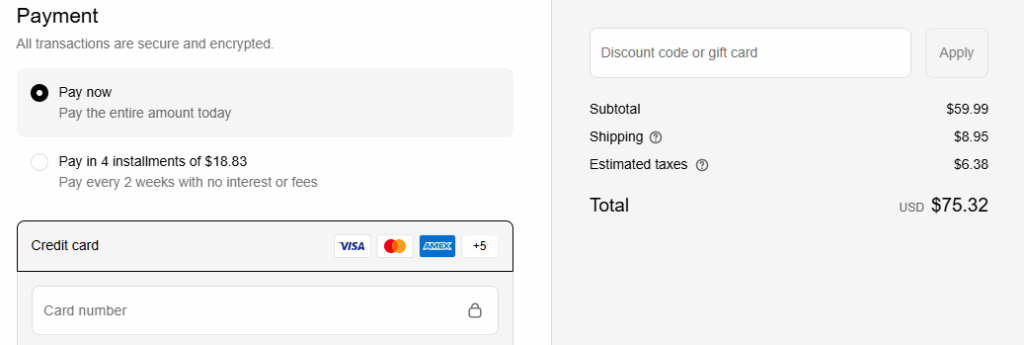

Since I’m currently on a no-spend streak, it took serious discipline not to complete checkout. I added a pair of shoes to my cart anyway—in the wrong size, just to keep myself honest—and clicked the purple Shop Pay button to test the flow.

I entered my email, phone number, and shipping address and saw two payment options:

- Pay in full ($75.32 total), or

- Pay in 4 interest-free installments of $18.83 every two weeks (via Affirm).

No extra fees, no re-entering card details, and no confusing redirects. After I entered my information, the screen clearly showed my four-payment breakdown before I (theoretically) clicked Complete Purchase. I didn’t, of course—I’m still sticking to that no-spend streak.

That’s where Shop Pay really shines. It’s fast, simple, and well-organized. Everything from shipping updates to carbon-neutral delivery tracking is handled right in the Shop app, where you can also view your full payment history at a glance. It’s one of the smoothest checkout experiences I’ve seen.

What It’s Like to Use Sezzle

Sezzle, on the other hand, feels more like a financial tool than a checkout button. I’ve used Sezzle for everything from back-to-school shopping to flights to holiday gifts. What stands out most is the control it gives you.

After linking your debit card or bank account, Sezzle approves your purchase amount instantly (using only a soft credit check) and divides the total into four payments, usually over six weeks.

The best part? You can reschedule one payment per order for free if your due date doesn’t align with payday. Additional changes come with a small fee, but the flexibility makes budgeting easier, especially when unexpected bills hit.

Another standout feature is Sezzle Up, which lets users report payment history to all three major credit bureaus. It’s optional, but if you’re working on credit improvement, that’s a big advantage. Sezzle also offers optional upgrades like Sezzle Anywhere and Sezzle Premium, which expand your buying power and include perks like exclusive discounts and payment reminders.

Here’s what using Sezzle looked like for me in real life:

- Back-to-school week: I bought about $200 worth of supplies when cash was tight and paid just $50 upfront, with three equal payments every two weeks.

- Flight booking: When I needed to visit family unexpectedly, Sezzle split the $400 ticket into four interest-free installments, making it easier to manage alongside my regular bills.

- Holiday shopping: I grabbed a few gifts early and used the reschedule option to move one payment back a few days until payday.

Each time, my payment schedule appeared instantly, and my due dates were clear. The ability to shift a payment when needed felt like breathing room, not a loophole.

Installment Flexibility & Fees

Both platforms offer interest-free payments, but Sezzle gives shoppers more wiggle room when real life gets in the way.

Shop Pay Installments

- Offers Pay in 4 interest-free installments or monthly financing for larger purchases through Affirm.

- Terms are fixed—if your payment date doesn’t align with your budget, there’s no built-in way to change it.

- Missed payments may result in late fees from Affirm and could reduce your eligibility for future financing.

Sezzle Installments

- Splits payments into four installments over six weeks, interest-free when paid on time.

- Often allows one free reschedule per order (then a small fee for additional changes).

- Late fees are capped and clearly displayed before checkout.

- You can link a bank account instead of a debit card to avoid an extra $1.50 in transaction fees.

Bottom line: Shop Pay keeps it simple and automatic. Sezzle gives you flexibility when your paycheck or expenses shift.

App & User Experience

Both platforms aim to make checkout easier, but they approach flexible payments in different ways.

Shop Pay is built right into Shopify’s checkout process, so you don’t have to download another app unless you want to use the Shop app for delivery tracking. For shoppers who buy from multiple Shopify stores, it’s almost effortless: saved info, click, confirm, done.

Sezzle, by contrast, is a standalone BNPL app designed for flexibility and budgeting control. You can view upcoming due dates, reschedule payments, check your available limit, and explore partner stores all in one place. It’s less about one-click checkout and more about managing purchases over time.

Here’s how that difference might look in real life:

Clara is shopping on the Spanx website for a new workout set. Her cart totals $141.10 after discounts, and when she clicks Checkout, the familiar purple Shop Pay button appears beneath the total. She selects it, her saved details auto-fill, and she’s offered two options: pay the full $141.10 today or split it into four interest-free payments of about $37 every two weeks. In under a minute, her order is ready to confirm, and she can track delivery right in the Shop app.

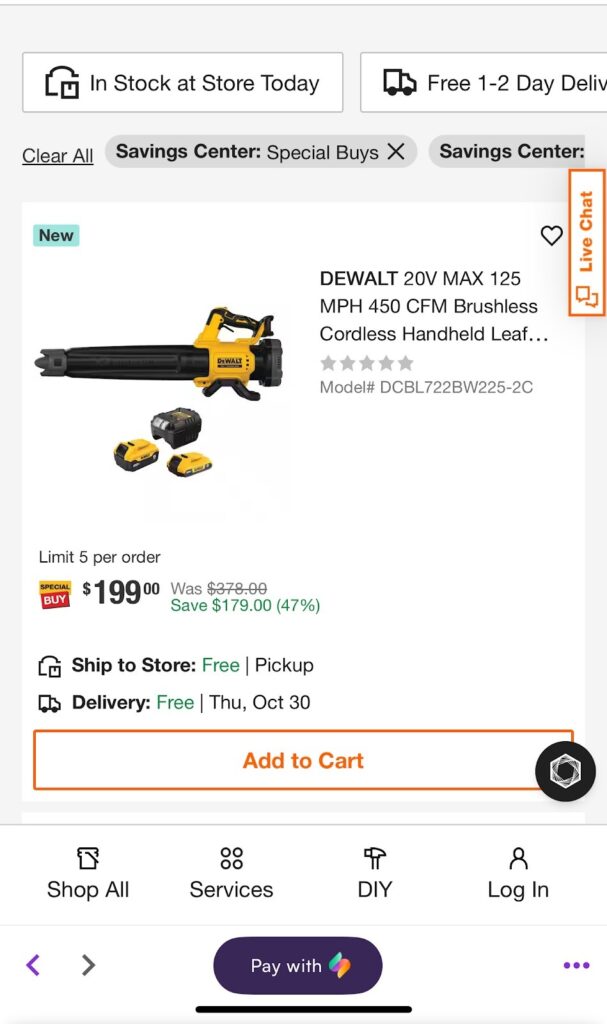

Asher is gearing up for his new lawn-care side hustle and needs a $199 leaf blower. He opens the Sezzle app and uses his virtual card to buy it from a hardware store that doesn’t take Shop Pay. Sezzle approves him instantly with a soft credit check and divides the total—including tax—into four interest-free payments of $50 each, billed every two weeks.

When an unexpected bill hits the same week as his second payment, Asher reschedules it right in the app—no penalty, no stress. His payment log updates automatically, and Sezzle sends friendly reminders so he stays on track while launching his new business.

Credit Impact & Extra Perks

This is where Shop Pay and Sezzle start to feel pretty different. Shop Pay, which runs its installment plans through Affirm, keeps things easy with no interest on Pay-in-4 purchases and nice touches like carbon-neutral shipping.

But it’s worth knowing that Affirm now reports all accounts to the credit bureaus, so opening a bunch of Shop Pay installment plans could show up on your credit report. There aren’t any membership perks or ways to move payment dates, so it’s mainly built for quick, no-fuss checkout.

Sezzle, on the other hand, gives you a little more breathing room. With Sezzle Up, you can choose to have your payments reported to credit bureaus to help build credit history over time. You can also reschedule one payment per order for free and even upgrade to Sezzle Premium or Sezzle Anywhere for extra features and spending power. It doesn’t have the eco benefits Shop Pay offers, but it’s definitely better for shoppers who want more flexibility and a few tools to manage their money.

Pros & Cons

Shop Pay

- Fast, one-tap checkout

- Carbon-neutral shipping

- Interest-free Pay-in-4 option through Affirm

- Built into millions of Shopify stores

- Limited to Shopify merchants

- No credit reporting

- No rescheduling or payment flexibility

Sezzle

- Four interest-free payments over six weeks

- One free reschedule per order

- Sezzle Up credit reporting to all three bureaus

- Standalone app with clear payment tracking

- Optional premium memberships for added perks

- Small service and late fees possible

- Requires linking a bank or card for full functionality

Final Verdict

If your main goal is fast, secure checkout, Shop Pay is hard to beat. It’s perfect for anyone who shops frequently on Shopify-hosted stores and wants a frictionless, eco-friendly payment experience. But if you’re looking for payment flexibility, budget control, or a way to pay for things at stores that Shop Pay doesn’t service, Sezzle comes out ahead.

Both platforms make paying later easier than ever. The difference?

- Shop Pay is a checkout shortcut.

- Sezzle is a financial tool.

Your best choice depends on whether you want convenience or control.

FAQs

No. Both Shop Pay and Sezzle offer interest-free installment plans as long as you make your payments on time.

No. Both platforms use a soft credit check for approval, which means applying won’t affect your credit score.

If you miss a payment, Shop Pay (via Affirm) may charge a late fee depending on the loan terms. Sezzle applies small, capped late fees and may temporarily lower your spending limit until payments are caught up.

Shop Pay is ideal for everyday or quick purchases made on Shopify-based stores, while Sezzle works better if you want to manage multiple payments across different retailers in one place.

Yes. Both payment options can increase conversion rates and reduce cart abandonment by giving customers the ability to choose flexible, interest-free payment plans at checkout.