I’ve tested just about every buy now, pay later app out there, but few have felt as opposite in tone and experience as Sezzle and Credova. One makes budgeting simple, flexible, and even kind of empowering. The other feels like stepping into a time capsule from the rent-to-own era, complete with unclear terms and a dashboard that never quite loads.

Sezzle sits at the top of my BNPL list for transparency, reliability, and everyday ease. Credova, on the other hand, sits at the bottom—not because it’s fraudulent or unsafe, but because it’s overly complicated, confusingly structured, and simply not built for the average shopper.

If you’re comparing Sezzle vs Credova and wondering which one actually supports your financial goals, here’s everything I learned from firsthand experience using both.

Sezzle or Credova: Which BNPL Should You Choose?

- For Everyday Purchases: Choose Sezzle if you want clear, interest-free payments and easy budgeting tools in one clean, reliable app. It’s ideal for groceries, gifts, travel, or other daily expenses—without hidden fees or confusion.

- For Building Credit: Choose Sezzle if you’re looking to build or strengthen your credit responsibly. With Sezzle Up, your on-time payments can be reported to major credit bureaus—no hard credit check required.

- For Flexibility and Transparency: Choose Sezzle if you value control and clarity. The app makes it simple to track spending, reschedule payments, and stay on top of your budget.

- For Niche or Tactical Stores: Choose a Credova offer if you’re shopping at a specific gun store, outdoor outfitter, or tactical retailer that partners with Credova. It’s designed for specialized merchants, not general shopping.

- For Short-Term Financing Only: Choose Credova if you can confidently pay off your purchase early. Miss the short payoff window, and those lease-style terms can make your total cost climb quickly.

Sezzle vs Credova Comparison

| Feature | ||

| Approval Process | Instant, no hard credit pull | Requires identity + bank account link |

| Payment Structure | Four equal interest-free payments | Lease or loan contract, depending on the merchant |

| App Access | Full mobile app and dashboard | Web-based portal, no dedicated app |

| Credit Reporting | Optional via Sezzle Up | Inconsistent, lease-style reporting |

| Merchant Network | 47,000+ stores, in-store & online for anyone who takes Visa | Niche network (firearms, outdoor, tactical) |

| Transparency | Clear payment terms upfront | Varies by merchant and contract |

| Best For | Everyday shoppers and budgeting | Specific gear or firearms financing |

What Is Sezzle?

Sezzle is a buy now, pay later app that splits your purchase into four interest-free payments over six weeks. You pay 25% upfront, and the rest is spread evenly across three more installments.

When I first used Sezzle, it was for an expense I hadn’t planned for. Instead of swiping my credit card and getting hit with a high interest rate later, I paid money up front on a $160 loan and handled the rest over time. It took two minutes to set up, didn’t affect my credit, and didn’t require sharing my full bank account routing number with anyone (although I did add it later on).

What I like most about Sezzle is its accessibility. You can use it almost anywhere, in-store or online, from grocery stores to clothing boutiques. I’ve used it for everything from Christmas shopping to booking travel, and it always feels straightforward—never sneaky.

Here’s what makes Sezzle stand out:

- Works Seamlessly Online & In-Store: Integrates with Apple Wallet and Google Pay for quick, flexible checkout anywhere.

- Free Payment Rescheduling: Lets you reschedule one payment per order at no cost if something unexpected happens.

- Credit-Building Feature: Offers Sezzle Up, a free opt-in credit reporting tool that can help boost your score over time.

- All-in-One Dashboard: Keeps approvals, reminders, and payment history organized in one easy-to-navigate app.

- Responsive Customer Support: Backed by real people who actually help—my issue was fixed in under 15 minutes.

With new FICO models soon including BNPL data, Sezzle’s credit-building option could become a real asset for responsible shoppers. If you’re looking for something predictable, transparent, and free of gimmicks, Sezzle makes everyday spending feel controlled and human—exactly what modern BNPL tools should be.

Get $15 Off Your First Target Purchase w/ Sezzle App

Sezzle

What Is Credova?

Credova is technically a buy now, pay later platform, but it doesn’t function like most others. Instead of giving you a universal virtual card or simple app, it partners with specific retailers—mainly in the firearms, outdoor, and tactical categories.

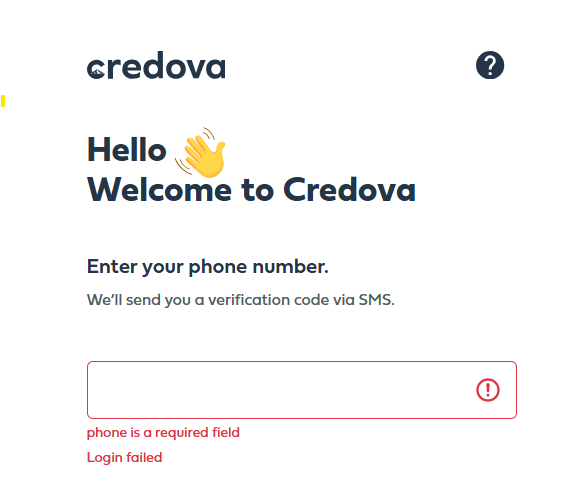

When I applied, I had to choose a merchant before seeing any offer. Out of curiosity, I clicked on one of the gun stores listed, even though I wasn’t actually shopping for anything. Seconds later, I was “approved” for $2,500 and redirected straight to that store’s website without ever seeing a clear confirmation screen. That’s when things started feeling off.

Credova’s financing can come as either a loan or a lease, depending on the merchant. Some contracts include an early payoff window—typically 30 to 90 days—that helps you avoid added costs if you pay on time. But if you miss that window, the total price can climb fast, similar to those rent-to-own stores where “easy payments” end up costing you triple the sticker price.

Here’s what stood out to me during the process:

- You must link your bank account for auto pay before proceeding. There’s no debit or credit card option.

- Approval happens before you pick a product, which feels backward for a financing platform.

- The customer portal didn’t work for me, showing only “invalid credentials” errors each time I tried to log in.

- There’s no mobile app or password recovery, leaving no way to verify your account or payments.

- Hours later, I started getting marketing emails urging me to “start shopping” with that same merchant—mostly ads for poultry feed, livestock fencing, and backyard supplies.

For someone with a homestead or outdoor business, Credova might seem convenient. But for the average shopper, it feels more like a sales funnel than a true financial tool. I never got confirmation that my bank details were safe, and I couldn’t tell who was handling my payment processing—Credova or one of their partners.

In the end, the entire experience felt impersonal and disjointed. I wasn’t sure what I’d signed, who managed my contract, or what would happen next. If you’re looking for a simple, reliable BNPL app, Credova isn’t it. This is especially true since they don’t have an app at all.

Credova

Sezzle vs. Credova: A Comparison

Using Sezzle and Credova back to back showed me just how different “buy now, pay later” platforms can really be.

Sezzle feels modern and user-friendly. I can shop online or in-store, split my total into four simple payments, and track everything in one clean app after checkout. The process is fast, there’s no hard credit pull, and I always know what I’ll owe and when.

Credova, on the other hand, is tied to one store at a time. It’s built for niche purchases—often at gun stores or outdoor retailers—where you apply before you even pick what you’re buying. That can make sense if you’re financing an entry-level pistol for competition shooting or stocking a small business, but for everyday purchases, it feels limited.

Here’s how they stack up in real life:

- Flexibility: Sezzle works anywhere its logo appears and even supports in-store tap-to-pay through Apple Wallet or Google Pay. Credova only works with select merchants, so once you choose, you’re locked in.

- Approval process: Sezzle allows you to experience great, instant, no-stress approval. Credova’s setup feels more like a mini loan application, complete with contracts and fine print.

- Payments: Sezzle automatically handles payment processing through its app, while Credova may hand your account to a third-party servicer like Monterey Financial, which adds extra steps if you need help with a transaction.

- Customer service: Sezzle’s support team is responsive—I reached a representative named Allie who fixed my issue in about 15 minutes. With Credova, I spent more time being redirected between the merchant and another company than getting answers.

- Overall experience: Sezzle feels built for shoppers who want control, convenience, and transparency through multiple purchases. Credova feels built for businesses that need financing options for big-ticket items.

Sezzle acts like a true consumer tool, helping you budget smarter and buy confidently. Credova operates more like a store financing program, and unless you’re already shopping with one of its niche partners, it’s hard to see the appeal, but let’s look at some of these areas in more detail.

Credit Reporting and Score Impact

Sezzle’s optional Sezzle Up program lets users report payments to all three major credit bureaus—Equifax, Experian, and TransUnion—helping build or rebuild credit responsibly.

Credova’s lease-style contracts, however, don’t always report in a way that benefits your score. Depending on whether your contract is a lease or loan, it may show up differently—or not at all. Some users have even reported seeing confusing entries on their credit reports that didn’t help them.

When I asked Credova support for clarification, I was never able to get a direct answer. Sezzle, by contrast, outlines everything upfront. You can see exactly what’s reported, how it’s shared, and what steps you need to take to qualify.

Bottom Line: If your long-term goal is improving your credit profile, Sezzle is the safer and more effective choice.

App Experience and Customer Support

Sezzle’s app is everything you want in a modern financial tool: clean, fast, and easy to navigate. You can see upcoming payments, manage due dates, and contact support all in one place.

Credova doesn’t offer a mobile app at all. Everything happens through a website that often feels like it’s been designed for desktop use only. The customer portal itself was buggy, and at one point, I couldn’t even log in. After I linked my bank account, I never got a confirmation or receipt—just marketing emails. It was the digital equivalent of being locked out of a store after handing someone your wallet.

Sezzle, meanwhile, sends automated reminders and updates. It’s not just about convenience; it’s about trust. I always knew exactly where my money was, what my balance looked like, and when the next charge would hit.

Credova’s system, by comparison, leaves too many gaps between the merchant, servicer, and customer. Even basic tasks like verifying your payment schedule or checking your balance can feel like detective work. I was never able to get a customer service representative to help much, although that doesn’t mean one wouldn’t offer assistance or a solution if pressed.

Bottom Line: Sezzle’s app is seamless and reliable, while Credova’s lack of one makes even simple account management frustrating.

Real Purchase Comparison

To see how both services really perform, I tested them with two realistic scenarios.

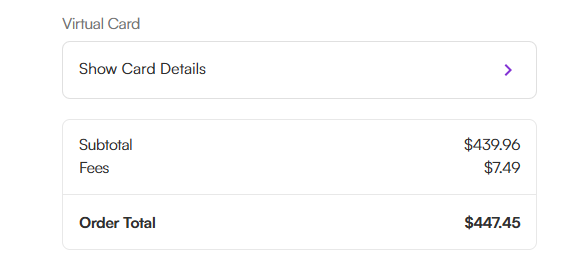

With Sezzle: I used Sezzle to book flights for an upcoming anniversary trip through Spirit Airlines. The total came to $447.45, including a $7.49 order fee. My plan was simple—$117.48 upfront, followed by three automatic payments of $109.99 every two weeks.

Everything appeared instantly in my app dashboard, with clear reminders, payment dates, and the option to manage the order through a virtual card. I made two payments before the airline canceled the flight, and Sezzle refunded my money within about five business days.

The only downside was that the initial order fee wasn’t refunded, which was disappointing since I never actually got to take the trip. Still, Sezzle handled everything automatically without me needing to contact support, and the process stayed smooth and transparent from start to finish.

With Credova, I tried to simulate a $600 firearm purchase for an entry-level pistol to see how the system worked. However, I was locked out of my account after the first entry and could never continue. Instead of assistance, I received three automated follow-up emails urging me to finish the purchase, but none of them offered help to fix the account. Because of that, I couldn’t even view or verify the loan terms—just repeated promotional messages with no actual support.

Credova User Experience (from Reddit)

One Reddit user shared an experience that perfectly illustrates why Credova’s structure can be so misleading for everyday consumers.

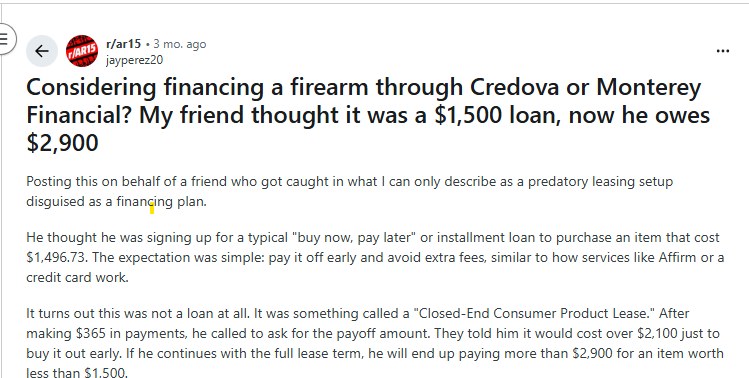

According to the post, the user’s friend thought he was signing up for a standard buy now, pay later or installment loan to purchase an item that cost $1,496.73. Like most people, he assumed he could pay it off early to avoid fees—just as he would with Affirm or a traditional credit card.

However, what he actually signed was a Closed-End Consumer Product Lease. After making $365 in payments, he called to request a payoff quote and was shocked to learn it would cost over $2,100 just to buy out the contract. Continuing through the full term would bring his total to more than $2,900 for an item worth less than $1,500.

The lease required paying 75% of the remaining balance to terminate early, and while the fine print technically labeled it a lease, the checkout process made it appear to be standard financing. Even the so-called “early buyout” option was limited to the first 30 days—and required paying the full item price upfront, regardless of any payments already made.

The user described the setup as predatory and misleading, adding that his friend now plans to file complaints with the Consumer Financial Protection Bureau (CFPB) and state attorney general offices.

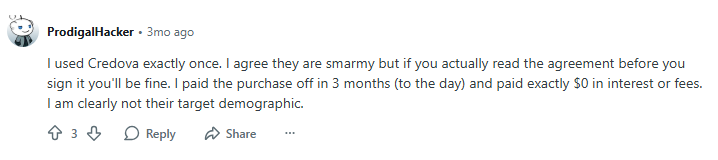

Stories like this highlight how Credova’s model can easily confuse customers who expect a traditional payment plan but instead find themselves bound by leasing terms that dramatically inflate the total cost. Still, it is important to note that many comments on this thread highlight the fact that these fees and lease obligations are in the fine print when you pull the trigger.

Final Verdict: Sezzle or Credova?

After testing both, I’d use Sezzle again in a heartbeat. I can’t say the same for Credova. I’ve used both, and only one felt like a financial tool that fits into my life instead of taking over my life.

Sezzle works for real life—for budgeting, emergencies, and everyday purchases. It’s free if you pay on time, integrates with your digital wallet, and even helps you build credit. The app feels human, and the customer support team actually acts like one.

Credova, meanwhile, feels like an old-school financing company trying to wear a modern BNPL mask. The bank account linking, merchant-locking, and lease-style contracts make it too complicated for the average shopper.

If you’re buying a specific item from a partner store—say, a competition shooting setup or outdoor equipment—and can pay it off fast, Credova might work. But for 99% of shoppers, Sezzle is the clear winner.

FAQs

Yes, Sezzle is safer than Credova because it uses a transparent app system with clear payment plans and no hidden fees. Credova’s lease and loan contracts vary by merchant, which makes it riskier and less predictable.

No, Credova doesn’t reliably report to credit bureaus. Sezzle does so through its Sezzle Up feature, which helps users build credit responsibly.

Yes, but Sezzle works more seamlessly in-store through Apple Wallet and Google Pay. Credova only works at specific partner merchants, like select gun stores or outdoor retailers.

Sezzle never charges interest if you pay on time. Credova’s interest rate or lease cost can rise quickly if you miss the early payoff window.

Sezzle is better for budgeting thanks to its easy app tracking and flexible payment options. Credova’s merchant-locked financing makes managing payments and costs more complicated.