If you’ve used Sezzle for a while, you’ve probably noticed your spending limit (or spending power, as Sezzle calls it) isn’t always the same.

Right now, my own limit sits at around $600, but I’ve seen it climb much higher in the past—and then dip again for reasons that weren’t exactly clear. I’ve also read plenty of stories from other shoppers who’ve had the same experience.

The good news? A changing limit isn’t necessarily a bad thing. It’s just part of how Sezzle manages flexible, interest-free spending while keeping accounts safe and reliable. Let’s break down why your Sezzle spending limit can fluctuate, what affects it, and how to help it grow again over time.

Key Takeaways

- Dynamic Spending Limit: Your Sezzle spending limit is flexible—it changes as your account activity, payments, and shopping behavior evolve.

- Unique Approval Process: Sezzle uses its own system to determine and update limits, considering payment history, order activity, and account behavior rather than relying solely on credit scores.

- Soft Credit Checks Only: Sezzle performs soft credit checks that won’t affect your credit score, even when your account or limit is reviewed.

- Linked Payment Methods: Connecting a debit card or a verified bank account may improve your Sezzle standing, though results vary by user.

- Automatic Adjustments: Limit increases and decreases happen automatically. They aren’t punishments; they’re part of Sezzle’s effort to balance risk and keep the service running smoothly for everyone.

How Sezzle’s Spending Limit Works

Your spending limit in Sezzle isn’t a one-time number; it’s more like a snapshot of your financial relationship with the app at any given time.

When you first sign up, Sezzle assigns a limit based on a unique approval process that looks at:

- How often you use the app and make payments on time

- The average size of your orders

- Your connected debit card or bank account activity

- Sezzle’s overall risk and reliability models

Over time, your limit can rise as you successfully complete orders and demonstrate responsible use. But it can also decrease temporarily if Sezzle’s system detects anything unusual or if your usage pattern changes.

Why Your Limit Might Drop

Many users have noticed their spending power suddenly drops—even after paying early or never missing a payment. In one Reddit thread, shoppers mentioned decreases happening right after linking a bank account or paying off several orders at once.

This doesn’t necessarily mean you did anything wrong. Sezzle’s algorithm constantly adjusts based on multiple factors, including recent spending, payment frequency, and the overall demand on their system.

Sometimes, linking a new account through Plaid (Sezzle’s verification partner) can trigger a short-term reduction while the system re-evaluates your risk level. Other times, inactivity or rapid payments may temporarily lower your available limit until the algorithm updates again.

Why Your Limit Might Increase

Plenty of Sezzle shoppers have seen the opposite—steady growth over time. Some report small increases after consistent use, while others see jumps after paying early or finishing several orders in full.

Sezzle tends to reward:

- On-time or early payments

- Consistent app usage

- Smaller, frequent purchases

- Paid-off orders with no outstanding balances

Your limit may rise gradually every few weeks as Sezzle reviews your history and detects responsible use. Increases often happen automatically and don’t require you to request them.

Factors That Affect Your Spending Power

Here’s a look at what can influence your Sezzle spending limit—both positively and negatively:

| Factor | Effect on Limit | Why It Matters |

|---|---|---|

| On-time payments | ➕ Increase | Builds trust and reliability with Sezzle |

| Early payments | ➕ Increase | Signals strong financial habits |

| Inactivity | ➖ Decrease | Less usage can trigger automatic reductions |

| Linking a bank account | 〰️ Varies | Helps verification, but may temporarily lower your limit |

| Missed or failed payments | ➖ Decrease | Raises repayment risk |

| Smaller, consistent orders | ➕ Increase | Demonstrates stable, low-risk use |

| High order volume or risk | ➖ Decrease | May cause Sezzle to adjust temporarily |

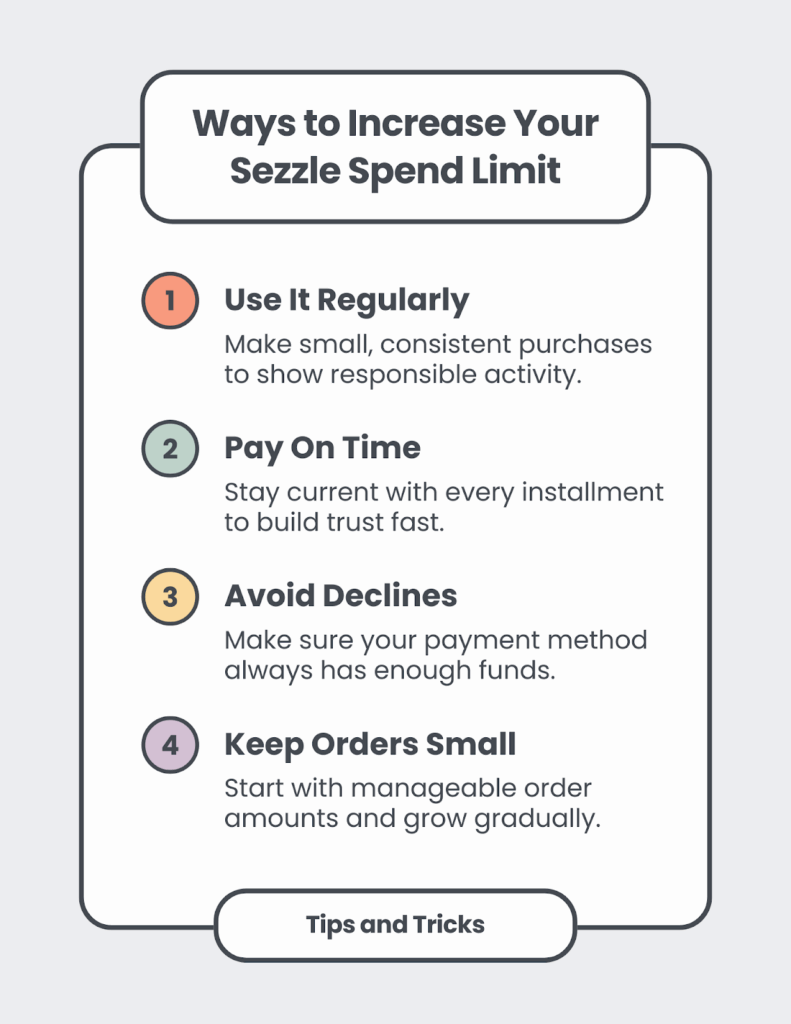

How to Encourage an Increase

While Sezzle doesn’t guarantee increases, most shoppers who see growth follow a few consistent habits:

- Pay early or on time. Even a few days early helps establish reliability.

- Keep a small balance. Avoid maxing out your limit; it shows control.

- Shop consistently. Small, regular orders tend to help more than big, occasional ones.

- Avoid missed or rescheduled payments. These can flag your account for review.

- Be patient. Sezzle often re-evaluates every few weeks, and increases can happen quietly in the background.

Common Misconceptions

There’s a lot of talk online about Sezzle “penalizing” users with lower limits, but that’s not exactly how it works.

- Bank linking doesn’t always hurt your limit. For some users, it improves reliability; for others, it triggers short-term recalculation.

- Limit changes aren’t punishment. They reflect Sezzle’s real-time risk adjustments, not your personal financial worth.

- Credit cards and Sezzle serve different purposes. Even with strong credit, Sezzle offers flexible, interest-free options without long-term debt.

Real Experiences from Sezzle Shoppers

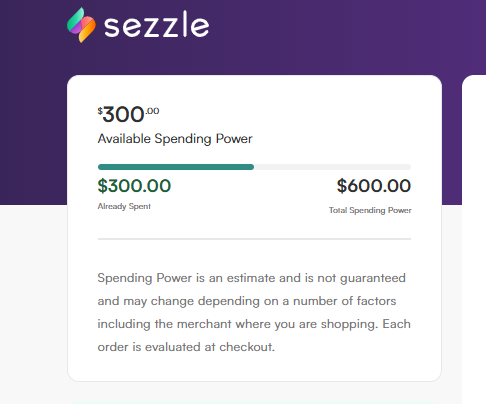

Across Reddit and other forums, experiences are mixed. Some shoppers reported their limit dropping from $1,000 to $250 after linking a bank account, while others saw steady growth from $300 to $600 after months of consistent use.

One user mentioned that paying early and using Sezzle regularly kept their limit rising, while another said inactivity led to a decrease. It’s clear that the system reacts differently for each person, likely based on individual usage patterns and risk evaluations.

As one user summed it up:

“I’ve been talking about how I’ve been using it regular since July, have gone from 300, 500 then 600. But this past week it went down to 525. I pay everything early, up to 2 weeks I just pay what will be due before my next paycheck. So it’s clear it reaches everyone at some point.” — u/FleetingDaisies91, Reddit

The same user later says,

“It stayed at 525 that period but on my recent 10/22 paycheck and normal

payment behavior it went up to 625.”

A Balanced Perspective

As a Sezzle user myself, I understand the confusion when your limit changes without warning. But these shifts don’t necessarily mean something negative; it’s just Sezzle’s automated way of adapting to user activity.

If your limit drops unexpectedly, give it a billing cycle or two. Keep your payments consistent, stay active, and check your account regularly. Most users eventually see their spending power rise again as their profile stabilizes.

Final Thoughts

Your Sezzle spending limit is meant to be flexible. It moves with your activity, order history, and overall reliability as a shopper. Think of it as a reflection of your Sezzle relationship, not a grade. The more responsibly and consistently you use the app, the better your spending power tends to become over time. So if your number dips for a while, don’t stress—it’s not permanent. Keep making smart purchases, pay on time, and let Sezzle’s system catch up.

Learn more about Sezzle in my review with first-hand experience using the app.

FAQs

Not always. Sezzle is mostly free to use, but there may be a small service fee at checkout. You’ll also see fees for missed payments.

Your purchasing power depends on several factors, like your order history, payment behavior, and overall account activity.

Yes. Sezzle shoppers who place smaller orders and pay them off quickly often see their limit rise over time.

No. Sezzle’s unique approval process happens instantly and separately from the merchant’s checkout system.

Definitely. Responsible use—like consistent payments and no declined orders—can increase your access and likelihood of being approved for larger order amounts in the future.