When I first started using buy now, pay later services, my biggest fear was hidden interest rates and surprise charges I didn’t expect. That’s why I looked closely at Sezzle. So, does Sezzle charge interest?

The short answer is: No, Sezzle does not charge interest on its standard Pay-in-4 plan.

Instead, Sezzle makes it possible to split payments into four interest-free payments, beginning with the first payment at checkout. The remaining amount is scheduled automatically over six weeks. With the popularity of BNPL continuing to rise—already making up nearly 1 in 10 e-commerce purchases in North America—it’s easy to see why I felt confident signing up for a Sezzle account. The purchase price I saw at checkout was the same total cost I paid in the end.

Key Takeaways

- No Interest on Pay-in-4 – Sezzle’s standard Pay-in-4 plan is always interest-free, so your purchase never costs more than the original price as long as you pay on time.

- Flat Fees, Not Interest – Instead of charging interest, Sezzle applies late fees or small service fees for missed or rescheduled payments.

- Pay Monthly Plans Include Interest – Sezzle’s longer-term Pay Monthly options for larger purchases do carry interest rates, which can raise your total cost.

- Hard Credit Inquiry for Interest-Bearing Loans – Unlike Pay-in-4, Pay Monthly financing may require a hard credit inquiry since interest is involved.

- Interest and Credit Reporting Work Together – With Sezzle Up, on-time payments from either plan can be reported to the credit bureaus, helping you build credit while keeping interest costs low.

Why the Pay-in-4 Plan Is Interest-Free

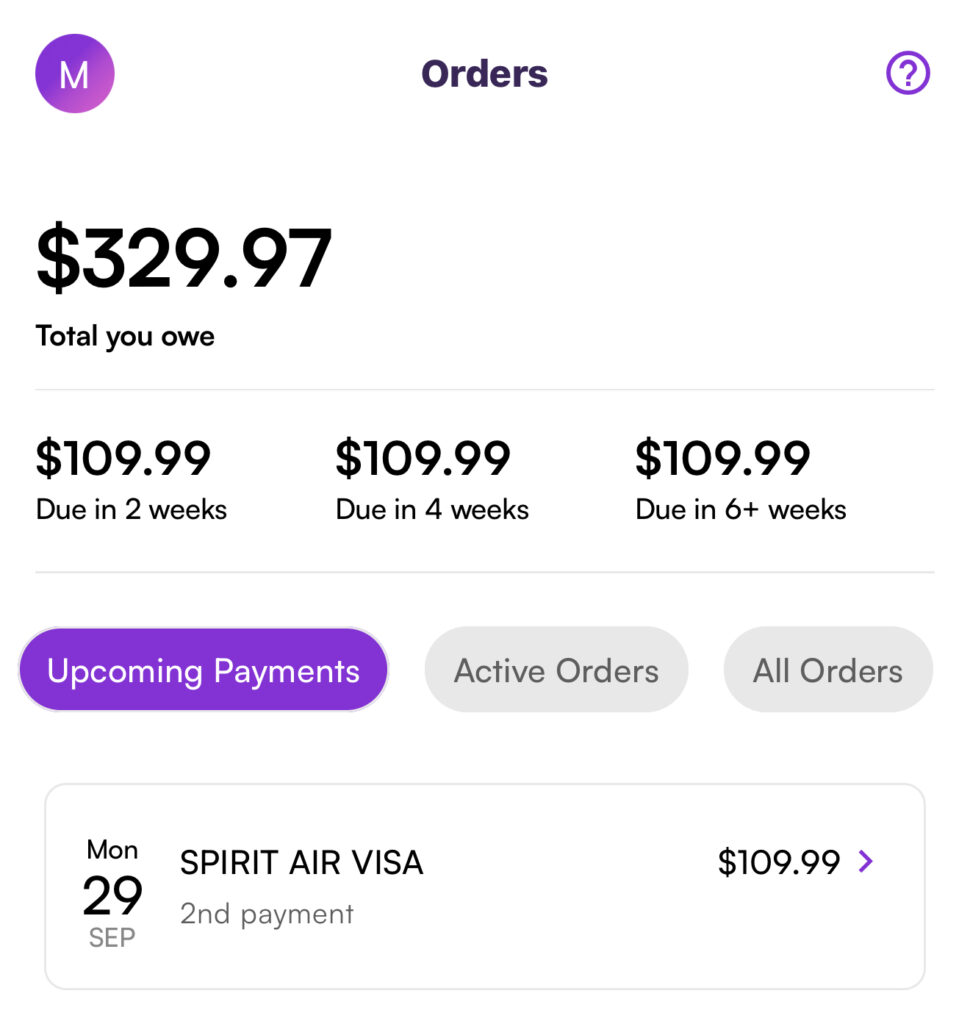

The most common payment plan Sezzle offers is Pay-in-4, which is built around interest-free installments. For example, I once used Sezzle for a purchase that totaled $447.45. Instead of paying the full amount upfront, the order was divided into four payments spread over six weeks. My first payment came to $117.48 because it included Sezzle’s small service fee along with part of the purchase cost. After that, the remaining amount was split into three weekly payments of $109.99 each.

What stood out to me was how the total cost stayed exactly $447.45—no hidden fees, no creeping interest rates, and no unexpected finance charges the way there would have been if I had put the same expense on a credit card or taken out a personal loan. That’s what makes this BNPL payment option plan so different: the structure is simple, predictable, and interest-free as long as you stay on schedule.

How Credit Checks Relate to Interest

When you open a Sezzle account, the company only runs a soft credit check, which won’t affect your credit score. This is why the standard Pay-in-4 plan stays interest-free—Sezzle isn’t extending long-term credit, just short-term installments.

However, if you choose a Pay Monthly option for larger purchases, the rules change. Because these plans charge interest, Sezzle may require a hard credit inquiry to evaluate your risk as a borrower. In other words, interest-bearing plans involve a deeper look at your credit profile, while interest-free plans don’t. That distinction gave me confidence. It showed that Sezzle is clear about when interest comes into play and when it doesn’t, making it feel more transparent than many traditional lending options.

What Happens With Missed Payments

While Sezzle doesn’t charge a percentage on interest-free payment plans, it does have clear rules about due dates. If you have missed payments or late payments, you’ll face a flat late fee.

In my own experience, I once had insufficient funds in my bank account when a payment hit. Sezzle first tried my default payment method and then a backup debit or credit card. When neither worked, I had to cover the missed payment plus a fee.

Thankfully, Sezzle lets you reschedule payments once per order for free. After that, there’s a small service fee. With a little planning, you can avoid these costs entirely.

Longer Plans That Do Charge Interest

Sezzle’s Pay-in-4 is interest-free, but Sezzle also offers Pay Monthly plans for larger purchases. These can range from three months up to 48 months, and they do charge interest.

Here’s how it works:

- Interest rates typically range from about 5.99% to 34.99% APR.

- Monthly payments are lower, but the total cost ends up higher because of interest.

- Your payment history is often reported through credit reporting, which can help or hurt your credit history depending on how you manage it.

Example: If I wanted to finance a $1,200 laptop, I could use Pay-in-4 and make four payments of $300 with no interest. Or, I could choose a 12-month Pay Monthly plan at 18% APR, paying about $110 each month. It’s easier to budget, but I’d pay more than $1,200 overall because of the interest Sezzle charges on longer-term loans.

Final Thoughts

Sezzle does not charge interest on its standard Pay-in-4 plan, making it one of the most transparent and affordable BNPL options available. However, its Pay Monthly option for larger purchases does include interest, so you need to weigh the benefit of lower payments against the reality of paying more overall.

Now that you know how to use Sezzle without getting charged interest, sign up with Sezzle and start splitting your payments.

FAQs

Yes and no. The Pay-in-4 plan is always interest-free. But if you choose Sezzle’s extended monthly financing, interest will apply, and the total cost will increase.

Yes, Sezzle checks credit. A soft credit pull is used when you first sign up, and it won’t hurt your score. For extended financing, a hard credit inquiry may be required.

Yes. With Sezzle Up, your payment history is reported to the credit bureaus, allowing you to establish a credit history and gradually build credit.

If you miss a due date, Sezzle charges a flat late fee. Missed payments can also lower your credit limit and limit access to Sezzle’s exclusive perks like higher spending power or a rewards program.

In my opinion, yes. Sezzle stands as a more transparent payment solution. The Pay-in-4 plan is always interest-free, and even though the Pay Monthly plan includes interest, it’s still clear up front. That makes Sezzle safe to use as long as you stay on top of your payment deadlines.