I’ve tested plenty of buy now, pay later apps, but Credova left me more uneasy than any of them. What started as a quick sign-up turned into a confusing mix of instant credit checks, required bank links, and unclear approval terms that seem more like risky loans than BNPLS.

I was surprised by how much personal information the site seemed to pull automatically—and even more confused when a “lease” appeared on my screen before I’d made a purchase. But still, many people like and use Credova on a daily basis. So in truth, it isn’t all bad.

In this review, I’ll break down how Credova’s application process really works, what its payment terms and financing options look like, and why so many users (myself included) have questions about customer service.

Who Is Credova Best For?

- Shoppers who plan to pay off early—ideally within a 30-day or 90-day promotional window.

- Buyers who already have a specific merchant in mind that partners with Credova.

- Users who are comfortable linking a bank account and setting up autopay even before deciding if they want to use the service.

- Consumers seeking a simple interest-free Pay-in-4 experience like Sezzle or Klarna.

- Anyone hoping to build credit—Credova’s lease structure may not report positively.

- Customers who dislike sharing account information or navigating unclear contracts.

- Buyers who expect a universal virtual card or easy app access (Credova doesn’t offer one).

What Is Credova?

Credova is a buy now, pay later platform that works a little differently from most. Instead of issuing a virtual card you can use anywhere, Credova partners with specific retailers, often those operating outside the mainstream financial ecosystem. Your approval applies only to the merchant you choose, not across multiple stores.

The company’s branding and blog emphasize themes of self-reliance, preparedness, and traditional values, appealing to shoppers who identify with outdoor lifestyles and hands-on professions. Most of its retail partners fall within a few clear categories:

- Outdoor and adventure gear – camping, hunting, fishing, and survival equipment

- Firearms and tactical shops – guns, ammo, optics, safes, and accessories

- Rugged lifestyle and workwear – boots, apparel, and field-ready tools

- Ranching, farming, and pet supply merchants

- Small specialty retailers in industries often underserved by traditional credit

That gives Credova a distinctly “frontier finance” feel, built for buyers who prefer practical purchases over luxury goods. It’s also what sets the platform apart: while other BNPL apps integrate with fashion, beauty, or tech retailers, Credova’s merchant base is rooted in blue-collar, outdoor, and firearm-adjacent markets.

A Merchant-Locked System

When you apply through Credova, your approval is tied to a specific retailer. You can’t move forward until you pick one from a dropdown list of partner stores. Once you do, you’re locked in; there’s no browsing or changing your mind later.

For people who already know and love Credova’s partner network—outdoor outfitters, tactical gear suppliers, hunting and fishing shops, and similar retailers—that probably feels natural. But if you’re not immersed in that world, it can be a little disorienting.

In my case, I grew up in a hunting and fishing community, so I should have recognized at least one name on the list… but I didn’t. (Apparently, years of bait-shop proximity did not prepare me for BNPL wilderness survival.) I ended up clicking the first merchant that popped up just to keep the process moving, not realizing I’d be stuck financing only through that one store.

Moments later, I was automatically approved for $2,500 and redirected straight to that store’s website, with no chance to explore other options or even confirm what I was agreeing to. It felt less like a flexible “shop now, pay later” service and more like a single-use line of credit attached to a random retailer.

Lease or Loan: What It Really Means

Credova’s financing can take two forms: a lease-to-own agreement or a standard installment loan, depending on the merchant and product. Lease-style contracts often come with an early purchase option (usually within 30 to 90 days) that lets you pay off the balance before extra fees or lease charges kick in. But that “no interest if paid early” tagline only holds true if you hit that deadline exactly; miss it, and the plan can turn into a high-cost lease or interest-bearing loan.

The whole setup feels a lot like those rent-to-own stores that advertise “easy weekly payments” on a washing machine, until you realize you’ve paid for it three times over. You’re not steadily building ownership; you’re feeding an endless cycle of small payments that mostly go toward fees and interest.

To add another wrinkle, Credova often partners with Monterey Financial for payment servicing and collections. That means you might make payments—or try to fix billing issues—through a different company entirely. If you use Credova, it’s worth confirming who actually handles your account and getting their contact info in writing.

In short, what starts as an affordable or interest-free plan can quickly grow costly if you’re not careful with timing or communication. Read every contract line, know who you’re paying, and don’t assume the deal ends when your receipt says “paid.”

How the Application Process Felt (and What to Expect)

How the Application Process Works

Applying for Credova feels quick at first, but it’s anything but transparent once you dig in. The entire process unfolds in a way that looks straightforward on the surface yet leaves you with more questions than answers.

Step 1: Instant Personal Data Recognition

After entering my phone number and the last four digits of my Social Security number, the site immediately populated my personal details—including my full name, address, and contact information. I hadn’t uploaded anything or verified my identity, which made the process feel unsettlingly automatic, as if my information was already on file somewhere.

Moments later, I received an email from TransUnion showing my credit score, even though the site never clarified whether the check was soft or hard. That lack of transparency can make applicants uneasy, especially if they’re protective of their credit profile.

Step 2: The Confusing Approval Stage

Once my information was verified, I was approved for $2,500; however, instead of showing me a list of clear financing options, Credova required me to select a merchant from several unfamiliar stores. I hadn’t browsed these retailers beforehand, which made the step feel out of order—almost like being asked to choose where to spend your loan before knowing what you were buying.

Since I was traveling, the store options appeared tied to my location/IP address, not my home state. It was strange to be approved for financing at a shop hundreds of miles away from where I live.

Step 3: Bank Account Requirement

Before I could move forward, Credova required that I link a bank account and set up auto pay. There was no option to skip or use a debit or credit card instead. That’s the point where I started feeling uneasy about continuing, since it meant granting the system direct access to my financial information before even finalizing a purchase.

To protect myself, I used an account I rarely touch. Only after doing that did the site allow me to proceed—and it immediately redirected me to the merchant website I had just selected.

Step 4: The Redirect and Aftermath

From there, everything went silent. The approval didn’t transfer smoothly, and I never reached a confirmation screen. When I later tried to log back into Credova’s customer portal, I repeatedly got an “invalid credentials” message. Without a mobile app or recovery system, I had no clear way to check the status of my application or whether my bank information had actually been verified.

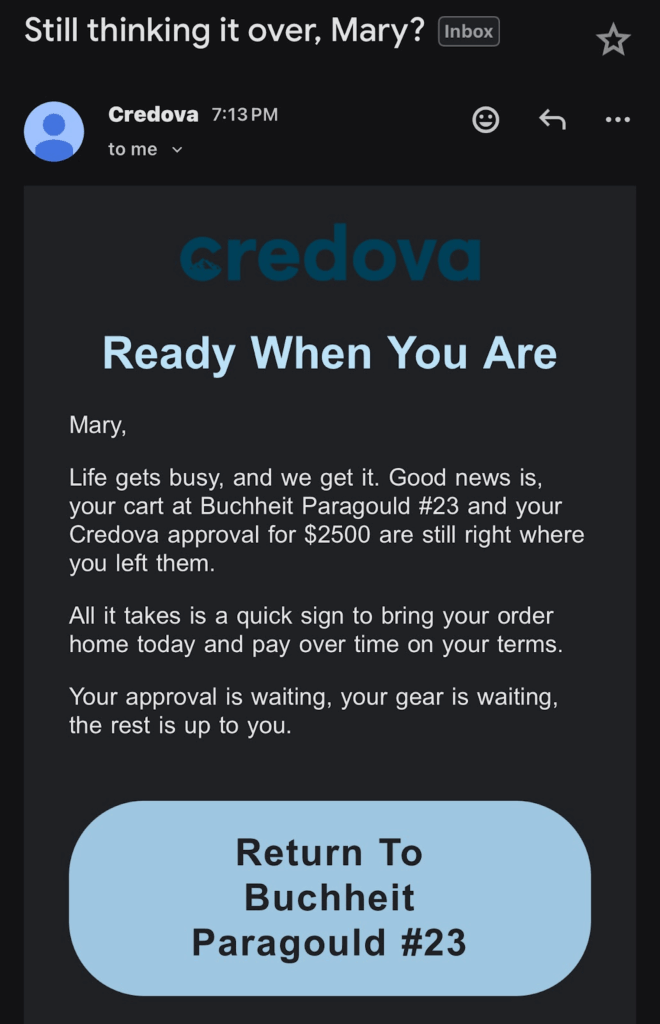

But what they did do was start emailing me a few hours later, encouraging me to start shopping with the same merchant I’d been auto-linked to during approval. The emails promoted items like poultry, livestock feed, and backyard animal supplies. To be fair, that might be perfect for someone running a small homestead. But since I wasn’t in the market for chickens or fencing, I ignored it.

It was a strange experience overall. I couldn’t log in or confirm that my banking information was secure, yet the system had no problem sending me marketing emails about spending money I wasn’t even sure I could access.

Step 5: Takeaways From the Process

For shoppers used to services like Sezzle, Klarna, or Affirm, Credova’s setup feels like a throwback to older lease financing models: fast approval, limited transparency, and contracts that move ahead before you’ve reviewed all the details.

If you ever decide to try Credova, my advice is simple:

- Take screenshots of every page as you apply.

- Confirm in writing whether the credit pull is soft or hard.

- Wait to link your bank account until you fully understand the terms.

- And most importantly, don’t assume approval means control—once you enter your info, the process takes on a life of its own.

Customer Service & Support: What Happened When I Tried to Re-Access

When I couldn’t log back in (the customer portal kept throwing an “invalid” notice), I wanted a quick customer service representative to help verify and confirm my account information. This is where your experience may hinge on the customer service team you reach and whether your merchant or a servicer like Monterey Financial is involved.

If you need assistance, try this:

Fast Escalation Checklist

- Document everything: timestamps, screenshots, contract PDFs, and confirmation emails.

- Contact multiple channels: merchant support and Credova’s support. Ask who is servicing your account (Credova vs. Monterey Financial).

- Ask targeted questions: “Is my agreement a lease or loan?”, “What’s my early payoff date and amount?”, “What shows on my credit?”, “Was my pull soft or hard?”

- Confirm in writing: Request a written response; keep it for future review.

- If unresolved: Consider a formal complaint with the merchant and appropriate regulators; remain factual, non-emotional, and include your transaction record.

Credova Pros

- Quick approvals at checkout with select merchants

- Potential interest-free outcome if early purchase/30-day payoff applies and you meet it

- Fills a niche for multiple purchases across specific outdoor/tactical retailers

Credova Cons

- Merchant-locked flow (not a universal virtual card)

- Lease contracts and payment terms can be complex

- Requires linking a bank account up front; login/portal issues are confidence-draining

- Customer service/servicing handoffs (e.g., Monterey Financial) may complicate resolution

- Potentially confusing credit reporting and unclear soft credit check vs. hard pull expectations

Real User Experience: A Cautionary Example

While my own time with Credova stopped short of a full purchase, plenty of customers have shared first-hand stories that reveal a pattern: smooth at first, then confusing when it counts.

One Reddit user described using Credova three times to buy firearms-related gear, saying,

“The first two contracts went fine—it’s this last one that’s a nightmare. They explained how a final $21 payment suddenly increased to $51, even after confirming the funds were ready in their bank account: “I had the money there Monday. They said they’d pull it Tuesday. Next thing I know, it’s $51 and no one can tell me why.”

Frustrated, the user claimed that neither Credova nor its servicing partner, Monterey Financial, could clearly explain the discrepancy, adding:

“Their dealings with the vendor are what they care about, not the customer.”

That comment thread spiraled into a debate about the risks of using lease-style financing to “build credit.” One responder put it bluntly:

“You’re not building credit with consumer loans—you’re just proving you can’t wait.”

Others echoed that Credova’s structure—short-term, merchant-tied, and often treated as a lease—can make disputes or final payments complicated. As one commenter summed up: “If you can’t afford to buy it three times, you can’t afford it once.”

Credova vs Other BNPL Apps

Credova isn’t the only option for splitting purchases into smaller payments—but it’s one of the few that operates more like a lease-to-own service than a traditional BNPL app. Here’s how it stacks up against some of the most popular competitors.

Credova vs Affirm

Affirm lets shoppers pay over time with set terms ranging from a few weeks to 12 months or more. It’s transparent about interest rates, offers a clear APR disclosure before checkout, and integrates with major online retailers. Credova, on the other hand, often presents lease-style contracts that can vary widely in cost and structure depending on the merchant.

Bottom line: Affirm wins for clarity and transparency—you know exactly what you’ll pay before agreeing to anything.

Credova vs Sezzle

Sezzle is a short-term BNPL service that divides purchases into four equal payments over six weeks with no interest if paid on time. It’s simple, predictable, and ideal for smaller purchases. Credova’s approvals and contracts tend to focus on larger, higher-risk items and can include fees or lease terms beyond the typical six-week window.

Bottom line: Sezzle wins for simplicity and fee-free flexibility.

Save $15 on Your First Amazon Purchase via Sezzle App

Credova vs Klarna

Klarna combines pay-in-4 financing with a user-friendly mobile app, virtual cards, and extensive retailer partnerships. It’s designed for everyday shopping and offers cashback deals, return tracking, and more. By contrast, Credova has no mobile app and works only with select merchants—mainly in the outdoor and tactical categories.

Bottom line: Klarna wins for usability and wide merchant access.

Credova vs Zip

Zip (formerly Quadpay) functions as a true BNPL app with a virtual Visa card that can be used almost anywhere. Its four-installment plan includes a small per-payment fee, but it offers real-time flexibility for both online and in-store purchases. Credova lacks that versatility, locking users into one specific retailer once approved.

Bottom line: Zip wins for freedom of use and modern BNPL convenience.

Credova vs Splitit

Splitit takes a unique approach by using a shopper’s existing credit card limit to divide payments, charging no interest or new credit inquiries. It’s a great choice for users with established credit who want to spread payments without affecting their credit score. Credova, in contrast, creates new lease or loan accounts that can appear on your credit report.

Bottom line: Splitit wins for credit-friendly, no-new-loan financing.

Final Verdict: Should You Use Credova?

For me, no; I won’t be using Credova again. The forced bank account link, the merchant funnel, the portal access issues, and seeing a lease-style entry before choosing anything made this my least-favorite BNPL-style experience.

If your “tiny dream” is a specific, entry-level pistol for competition shooting and you’re absolutely certain you’ll pay off within the early window, Credova might bridge the gap. For most consumers, though, the process, contract complexity, and support variability make traditional cards (0% APR promos), credit-union loans, or old-school layaway feel safer—and simpler.

FAQs

Not by default. Some offers include a short interest-free or reduced-cost early purchase option, but if you miss it, your total cost can rise quickly. Read the contract.

In my experience, no. The money offered was merchant-locked; I had to choose from a store list during checkout and could not generate a universal virtual card for multiple purchases elsewhere.

Expect attempts to contact you and potential fees per your contract. If there’s a mistake (e.g., processing error), document it immediately and ask the customer service representative to review and fix it, as well as answer further questions.

Not reliably. Reporting can vary, and a lease entry doesn’t necessarily help your credit score. If your goal is credit building, a low-limit credit card with auto pay may be a better tool.

Some merchants allow additional transactions, but terms vary per payment plan. Always verify with the merchant and support before assuming your approval covers future buys.