When my car insurance premium suddenly went up, I started thinking about how hard that kind of jump can hit families already stretched thin. Not everyone can cover a big upfront payment or risk losing their insurance coverage, and I wanted to see whether buy now, pay later car insurance policies could really help.

In my state, recent audits have shown that drivers pay steeper reinstatement fees for insurance lapses than for DWIs. So, paying for insurance is a must.

BNPL platforms like Sezzle, Klarna, and Affirm are best known for online shopping, splitting purchases into four easy payments with no interest, but the idea of using one for auto insurance felt new. Most insurers don’t officially support these systems because of regulations around financing and monthly payments, but I decided to try it anyway.

Here are my results, and we’re digging deep; I’ll cover down payments, future payments, and more, so you know exactly what you’re getting into before getting started.

Key Takeaways

- BNPL can work for car insurance. Using Sezzle, I successfully made a Progressive auto insurance payment through a virtual card, split into four easy payments.

- It’s not a replacement for traditional payment plans. Most car insurance policies don’t officially partner with BNPL providers due to strict insurance coverage regulations.

- Small fees, big flexibility. Sezzle charged a $7.49 processing fee—not interest-free, but worth it to avoid a lapse in auto coverage or state penalties.

- Helpful for short-term relief. If you’re facing a sudden premium increase, BNPL can offer immediate relief without taking out a loan or using credit.

- Use it strategically. BNPL can bridge the gap between payment date and payday, but relying on it monthly could lead to higher costs over time.

When Would You Use Buy Now, Pay Later for Car Insurance?

While most car insurance policies are paid by the month or every six months, not everyone has the flexibility to make a large upfront payment when rates spike or renewals hit at the wrong time. That’s where buy now, pay later car insurance can offer short-term help.

Top national insurers like Progressive, GEICO, State Farm, Allstate, and USAA typically accept credit and debit payments online. So, if your BNPL app provides a virtual card (like Sezzle or Zip), you may be able to use it to fund a one-time auto insurance payment.

Here are a few situations where a BNPL option could make sense:

- 💸 Premium Increase: When your car insurance premium suddenly rises after an accident, moving a payment to installments can ease the impact on your budget.

- 🕒 Policy Renewal: If your renewal date arrives before payday, BNPL can help you stay covered without risking a lapse in insurance coverage.

- 🚗 New Vehicle Purchase: Buying a car often means an immediate insurance deposit or down payment; BNPL can give you breathing room while getting your new vehicle on the road.

- ⚠️ Avoiding Lapse Penalties: In states like Louisiana, letting auto coverage lapse can lead to fines or even license suspension. A BNPL payment can keep you insured until your next payment date.

- 🛠️ Unexpected Expenses: When life hits—repairs, medical bills, or other financial strain—BNPL offers help without adding interest or affecting credit.

While it’s not a long-term solution, the convenience and accessibility of BNPL can help drivers stay insured and drive legally when money is tight.

My Real Sezzle + Progressive Test

Here’s exactly what I did.

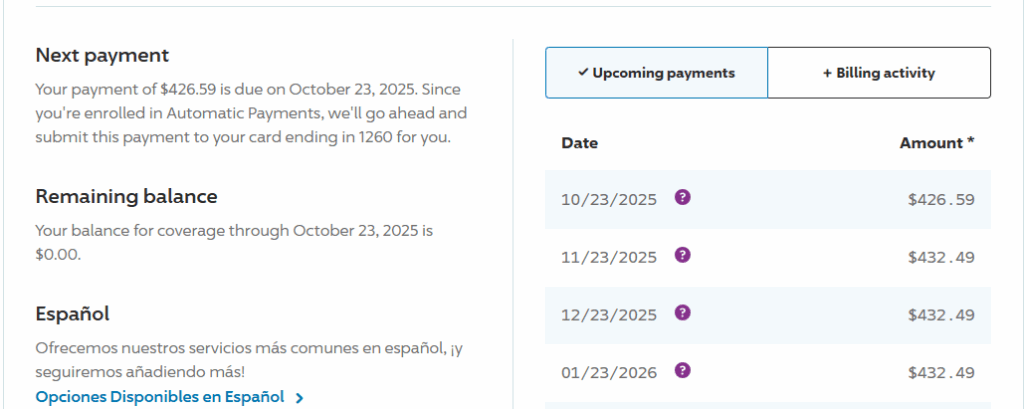

- Logged into my Progressive account and started a $400 payment toward my renewal balance.

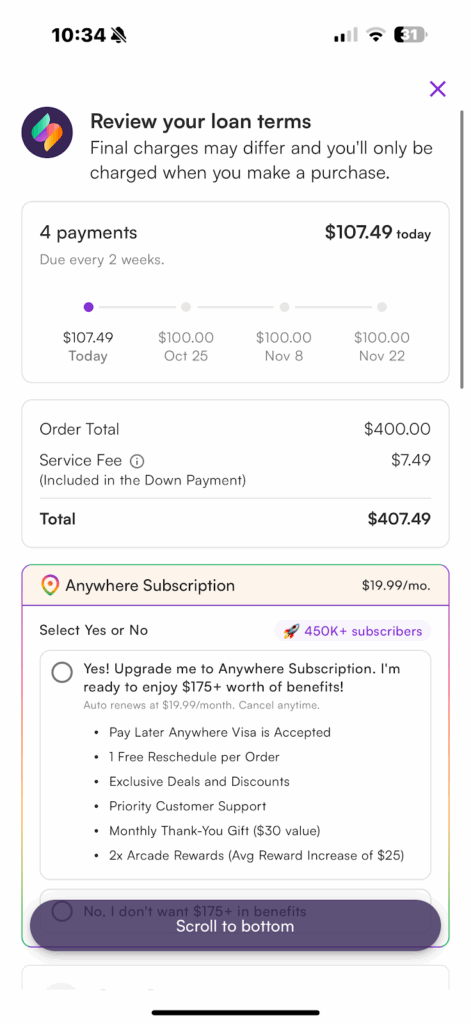

- Opened the Sezzle app, entered the amount I wanted to borrow ($400), and generated a one-time virtual card through Sezzle Anywhere.

- Copied the card info into Progressive’s checkout page.

- Hit “Pay.”

And it worked. Progressive processed the $400 payment instantly, and I got a confirmation page saying, “Thanks for your payment.”

Sezzle broke my $400 into four installments, plus a $7.49 processing fee—no interest, just the standard service charge. I paid my remaining $26 balance to Progressive separately, since Sezzle didn’t cover that fraction. If you qualify for more money, you could pay your whole amount.

Within seconds, everything showed up clearly inside both dashboards: Sezzle’s app listed my payment schedule, and Progressive displayed my next due date.

Why It’s Not Perfect—But Still Useful

Using Sezzle for auto coverage isn’t an ideal long-term plan. The $7.49 fee may seem small, but if you used it every month, that could add up fast. Still, if you’re in a financial pinch and facing a policy lapse, this option could be a lifesaver.

In my state, a lapse in car insurance coverage can mean big late fees, license suspension, or even your vehicle being flagged as uninsured. Paying a small Sezzle fee beats paying hundreds in state penalties or risking your license.

It’s not a full financing program or payment plan like some insurers offer, but it’s a workable solution for consumers who just need coverage options until their next paycheck.

BNPL and Car Insurance: The Bigger Picture

While my Sezzle experiment worked with Progressive, not every provider will process payments this way. Some companies block third-party cards, and others require recurring billing through direct debit.

That said, the trend is shifting. As more Americans look for flexible payment options, expect to see BNPL for car insurance become more common—especially as insurers seek ways to help customers afford coverage without falling behind.

Other BNPL platforms—like Affirm, Zip, and Klarna—are already expanding into sectors like medical bills, travel, and auto coverage programs, though most limit how much you can borrow or charge small fees for convenience.

Final Thoughts

My verdict? Buy now, pay later car insurance is possible—at least, to an extent. Sezzle made it easy to bridge a payment without risking my policy, and everything processed smoothly.

Would I use it every month? No. But in a tight spot, it’s an option that can protect your coverage, keep you insured, and help you drive legally—without taking out a high-interest loan or putting your credit on the line.

Sometimes, financial flexibility isn’t about luxury; it’s about keeping your life running when things go sideways.

FAQs

Yes, you can use Sezzle to pay for car insurance in some cases. I successfully used Sezzle to make a Progressive auto insurance payment by generating a one-time virtual card through the Sezzle app.

Not yet. While I confirmed it worked with Progressive, many insurers still don’t support buy now, pay later car insurance directly. Acceptance depends on whether your insurer’s payment portal allows third-party cards or BNPL checkout options like Affirm, Klarna, or Zip.

No, Sezzle doesn’t charge interest—but there is a small processing fee. In my case, the fee was $7.49 for a $400 payment. So, while it’s technically “interest-free,” it’s not totally free. Still, that’s often cheaper than risking a lapsed policy and the fees that come with it.

It depends on your situation. If you’re facing financial strain and need immediate relief to avoid losing coverage, BNPL can help. But it’s not ideal for every month—especially since repeated fees add up. Think of it as a short-term bridge, not a long-term financing plan.

Yes—if your insurer accepts it. There’s nothing illegal about using a BNPL service to fund an insurance bill, but not every provider allows it due to state regulations on financing insurance premiums. Always confirm with your insurer before relying on a third-party payment platform.

Absolutely. That’s one of its biggest benefits. In states like Louisiana, where a lapse in coverage can lead to suspended licenses or hefty reinstatement fees, using Sezzle or another BNPL app for an emergency payment can keep you insured.

Buy now, pay later car insurance lets drivers split their auto insurance or car insurance bills into smaller payment plans instead of one large initial payment. Using apps like Sezzle, you can pay for your insurance coverage over a short payment schedule.