If you’ve ever stared at your bank account and wondered how a $40 Target trip turned into $187… welcome, you’re in good company. And if your credit score has taken a few too many hits? You’re still not alone.

In fact, only 9.2% of Americans have a FICO score below 550, meaning most people with “bad credit” are actually somewhere in the middle—just trying to make it through bills, birthdays, and surprise expenses.

That’s exactly where buy now, pay later tools like Sezzle step in. You don’t need perfect credit —or even good credit—to use it. With soft credit checks, small approvals, and interest-free Pay-in-4 plans, Sezzle can make room in your budget without another credit card or high APR loan.

But like anything involving money? It can help you or hurt you, depending on how you use it.

Key Takeaways

- BNPL works even with bad credit: Most services, including Sezzle, use a soft credit check that does not impact your credit score.

- You’ll start with a smaller limit: Approval amounts are usually low at first, but often increase over time with consistent, on-time payments.

- Pay-in-4 plans are interest-free: You pay 25% upfront, then three equal payments every two weeks with no interest when paid on time.

- Monthly payments are sometimes available: Larger purchases may qualify for monthly plans through providers like Sezzle Premium or Affirm.

- BNPL impacts cash flow more than credit: Missed payments can lead to late fees, paused accounts, and possible credit reporting if you’re enrolled in credit-building programs.

Can You Use BNPL with Bad Credit?

Long story short? Yes, you can use BNPL with bad credit.

Most buy now, pay later lenders like Sezzle, Klarna, Afterpay, and Affirm, and approve shoppers using:

- A soft credit check (not reported to credit bureaus)

- Your debit card or bank account

- Your payment history with them—not your entire credit score

That means even if your score is low or you don’t have much credit history, you can still be approved for a BNPL loan.

How BNPL Helps People with Bad Credit

When used wisely, buy now, pay later can make budgeting easier and less stressful—especially if you’re working with bad credit or trying to avoid traditional loans. Here’s how it helps:

- No hard credit check: Most BNPL companies only run a soft credit check or review your income and spending activity, so your credit score isn’t impacted just to apply.

- No high-interest credit card debt: Pay-in-4 plans are usually interest-free, which means you can spread out the cost of a purchase without paying extra, like you would with a credit card APR.

- Smaller, predictable payments: Your total is split into four payments (or monthly plans for bigger purchases), making it easier to fit into your budget without paying everything up front.

- Can help build credit history (with select plans): Some services, like Sezzle Up, report payments to credit bureaus, which can help you build a positive credit history over time if you pay on time.

“Why Was I Declined?” and How to Improve Your Chances Next Time

Even though BNPL is more flexible than credit cards, you can still get declined. The good news? It’s not permanent—and it’s usually fixable.

Here’s what BNPL companies actually look at (even with bad credit):

| BNPL Factor | What It Means |

|---|---|

| Recent payment history | Have you missed payments with them before? |

| Active BNPL loans | Too many open plans can make you look overextended |

| Purchase amount | A $500 order may be declined, but $100 might be approved |

| Linked bank/ debit card activity | Low balance, overdrafts, or prepaid cards can affect approval |

| Account age | New accounts often start with lower limits to “test trust” |

| Suspicious activity | Wrong birthday, mismatched names, or multiple accounts |

What to Do If You’re Declined

- Start with a smaller purchase amount ($25–$75)

- Pay off one active plan before opening another

- Make sure your bank account has enough cash for the down payment + buffer

- Avoid prepaid cards—use a real debit card or checking account to pay monthly payments

- If available, upgrade to credit-reporting plans (like Sezzle Up) to build trust

Most lenders will let you try again in a few days or after a payment goes through. So “no” today doesn’t mean “no forever.”

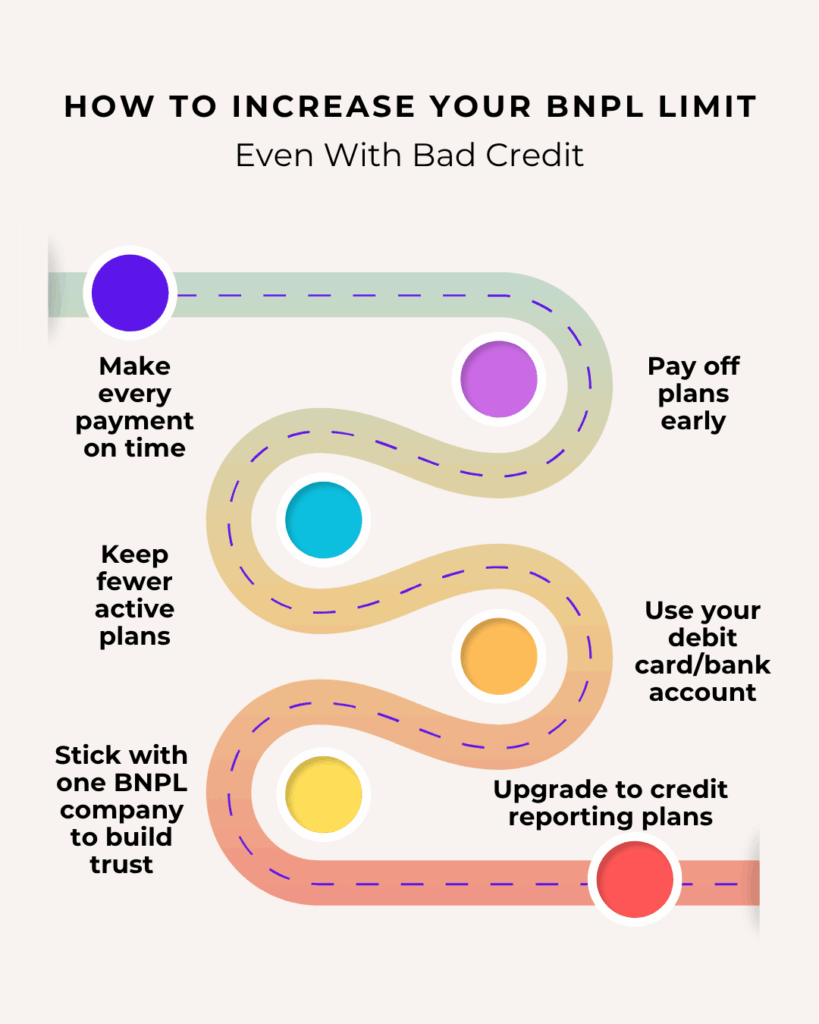

How to Increase Your BNPL Limit (Even with Bad Credit)

Start small—grow slowly. Here are ways to show you’re a responsible BNPL user:

- Make every payment on time: On-time installment loan payments = more trust + higher spending power

- Pay off plans early when possible: BNPL plans early pay off usually means no fee—this shows great money habits

- Avoid too many active BNPL plans at once: Too many outstanding loans can affect BNPL eligibility

- Use a debit card or bank account—not prepaid cards: BNPL lenders like seeing real checking account usage

- Sign up for credit-reporting upgrades (Sezzle Up, Affirm): This helps build a positive credit history over time

When Buy Now, Pay Later Can Be Risky

BNPL may not be the best choice when:

- You’re already behind on bills or loan payments

- You’re using it like a cash advance or ATM withdrawal

- You miss due dates and get hit with late fees

- You forget about multiple active plans and overdraft your bank account

- You depend on it to cover basic needs every week

BNPL isn’t free money. It’s still a short-term loan agreement that should be seen as a cash equivalent purchase, and unpaid plans can be sent to collections or reported to credit bureaus if you’re in a credit-reporting program.

Final Thoughts

Buy now, pay later doesn’t fix bad credit outright, but it can be a helpful tool when it’s used intentionally. It gives you flexibility without high interest rates, and for many of us rebuilding or protecting our credit, that breathing room matters. Just remember: every payment still counts. Start small, pay on time, and use it to support your budget, not stress it. If you want a BNPL option that’s flexible and credit-friendly, Sezzle is one of my personal favorites—and a great place to start.

FAQs

Most BNPL lenders only use a soft credit check, so it won’t affect your score.

Yes, you can still get BNPL with bad credit. Approval decisions are based on your account history, payment behavior, and purchase amount rather than just your credit score.

Yes, PayPal Pay in 4 is only available through a PayPal account. You’ll apply during checkout, and if approved, payments are managed directly inside your PayPal account.

Typically, yes, BNPL is better than a cash advance or loan. BNPL offers interest-free payments and no ATM withdrawal fees, but only if you pay everything on time.

When you make a BNPL payment, the first payment is processed like a debit card purchase (assuming you’re using your debit card). Most Pay-in-4 plans are interest-free and don’t charge an annual percentage rate (APR), but some longer monthly plans may include an APR, depending on the provider and loan terms.