New shoes can be a splurge, or a sudden necessity when your sneakers wear out or your boots give up mid-season. The price tag for quality footwear can hit hard, with some styles ranging from $50 to $300 or more per pair. Luckily, buy now, pay later (BNPL) makes it possible to shop at your favorite store, click checkout, and split purchases into manageable payments.

Every fall when the school year starts, money always feels tight. Between school supplies, fees, and clothes, there never seems to be enough left over for the shoes my kids need. That’s when I’ve had to get creative. This year, it was Sezzle that helped me out—letting me grab the new sneakers without blowing my budget all at once.

Here’s how BNPL works for shoes, which websites and apps let you apply, and what terms you should check to protect yourself from fees.

Key Takeaways

- Quick Approval: Apply with just your mobile number or account ID at checkout—most providers run only a simple credit check.

- Flexible Payments: Choose between interest-free installments or longer financing with fees.

- Where to Shop: Major brands and online shoe stores now offer BNPL options.

- Potential Drawbacks: Late fees can trigger extra costs if you’re unable to pay on time.

- Smart Shopping: Comparing providers helps you manage purchases without overspending.

How BNPL Works for Shoes

BNPL shoe programs let you choose a payment plan instead of paying the full price upfront. For example, instead of dropping $200 at once on boots, you can resolve the cost with four scheduled payments.

You’ll usually see the option during checkout. Once you apply, a BNPL app or website like Sezzle, Klarna, or Affirm runs a quick check to approve you. After that, payments are automatically charged on the card or bank account you submit.

It works for several actions: online orders, in-store purchases, and even pre-orders of limited-edition sneakers.

Where to Buy Shoes with BNPL

Here are a few examples of stores and brands that let you buy now, pay later for shoes:

- Nike: Use Klarna, Afterpay, Affirm, or Sezzle at checkout for sneakers and sports styles.

- Adidas: Offers flexible financing, letting you manage items in installments.

- DSW (Designer Shoe Warehouse): Partners with Sezzle and Klarna, giving you pay-later flexibility on everything from heels to boots.

- Foot Locker: Works with Afterpay for sneaker purchases, including popular limited drops.

- Walmart: Offers BNPL via Affirm, Sezzle, and Klarna for both online and in-store shoe purchases.

- Zappos: Known for its wide style selection, Zappos lets you finance through Klarna.

Many local shoe stores are also adding BNPL at checkout, so ask or check the store’s payment page.

Pros of Financing Shoes

- Get the shoes you need right away without waiting until payday.

- Short-term payment plans often charge no interest.

- Fast approval—sometimes just your phone number and email ID.

- Flexibility to line up payments with your budget.

Cons to Watch For

- Late fees if you miss a due date

- Longer financing may come with interest

Real-Life Example: Using Sezzle for Shoes

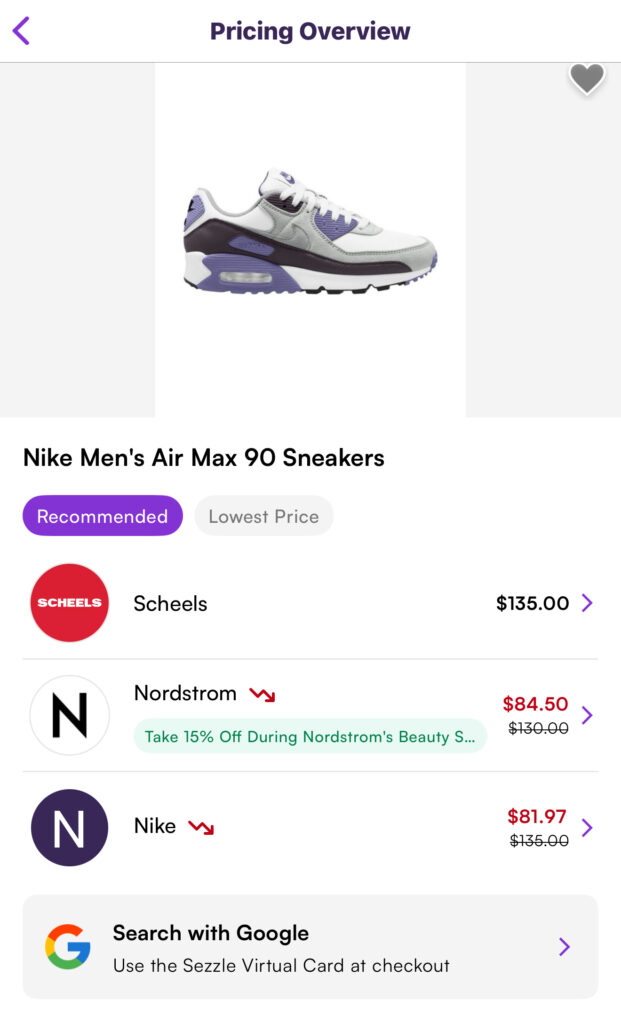

One of the things I love most about the Sezzle app is that it doesn’t just offer flexible payments—it also lets you compare prices for the exact same shoe across different websites. That means you can choose the cheapest option before you commit to a purchase.

For example, I found a pair of Nike Women’s Legend sneakers on Sezzle that were listed for just $39.97, compared to a much higher price in-store. Even with the small service fee Sezzle adds, I still saved money because I didn’t have to pay the full amount upfront. Instead, I split the total into four payments spread out every two weeks.

That kind of flexibility makes a huge difference, especially when money is tight around the back-to-school season. Instead of stressing about paying for new sneakers all at once, I was able to manage it in smaller chunks—and my kids still got the shoes they needed right on time.

Know the Terms (Using Sezzle for Shoes)

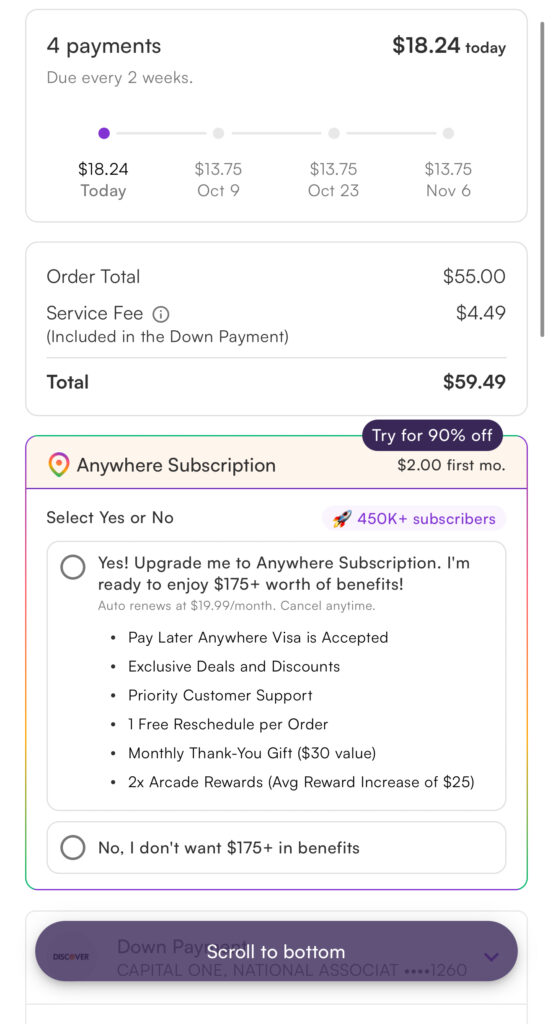

Here’s an actual example breakdown of how BNPL shoe financing worked for me with Sezzle:

- Order Total: $55.00

- Service Fee (Finance Charge): $4.49 (paid upfront, non-refundable)

- Amount Financed: $41.25

- Payments: Four installments of $18.24 (down payment), then $13.75, $13.75, $13.75

- Total Paid: $59.49

Tip: Always double-check the payment schedule before you click “apply” at checkout. If you stick to the terms and pay on time, Sezzle can be a really helpful way to manage purchases like sneakers, boots, or other must-have shoes.

Smart Tips for Shoe BNPL

- Compare Providers: Check which store uses Klarna, Sezzle, or Affirm and weigh the terms.

- Read the Fine Print: Some BNPL shoe programs act more like loans, subject to extra fees.

- Protect Your Budget: Just because you can spread payments doesn’t mean you should overshop.

- Stay on Time: Submitting payments late may trigger fees, account blocks, or negative marks.

- Look for Deals: Some apps even offer coupons—like $15 off when you download and shop via the Sezzle app.

Save $15 on Your First Amazon Purchase via Sezzle App

Final Thoughts

Shoes are one of those purchases you can’t really put off—kids outgrow them, sneakers wear down, or you just need a new pair for work or the weather. But when money is tight, especially during back-to-school season, it can feel impossible to cover everything at once. That’s where BNPL shoe programs shine. By splitting the cost into smaller payments, they give you the flexibility to shop brands like Nike, Adidas, or DSW without draining your account in a single checkout.

Still, it’s important to use BNPL wisely. Late fees or longer-term financing can quickly erase the savings, so always check the terms before you apply and set reminders to pay on time. For me, using Sezzle meant I could grab sneakers for my kids right when they needed them—without the stress of paying all at once. If you approach BNPL as a tool for managing essentials rather than an excuse to overspend, it can be a smart way to balance style, necessity, and your budget.

Start shoe shopping with Sezzle and split up those payments.

FAQs

Stores like Nike, Adidas, DSW, Foot Locker, Walmart, and Zappos all offer pay-later options with BNPL apps.

You don’t need good credit to finance shoes. Many providers run only a quick approval check that’s easier to pass than a traditional loan.

At checkout, click the BNPL option (like Sezzle, Klarna, or Affirm), submit your info, and choose your terms.

Late fees may apply, and some apps could block your account until the balance is resolved.

BNLP can be the best way to buy shoes if you pay on time and use short-term, interest-free options. Just manage your budget and compare terms first.