Sometimes, a purchase just can’t wait—a replacement laptop charger, a back-to-school uniform haul, or a last-minute birthday gift you didn’t plan for. With prices creeping up and credit cards charging average interest rates around 22.8%, consumers are always looking for a way to spread out costs without falling deeper into debt.

That’s why I decided to give Afterpay a try. One of the biggest names in buy now, pay later, I wanted to see if it could help me cover those unexpected costs without adding too much to my credit card balance.

After testing it on both smaller buys and a larger purchase, I found things to like, along with some drawbacks to consider before checking out. Keep reading to discover both.

Afterpay: Best Fit vs. Bad Fit

Who Afterpay Works Well For

- Anyone who wants to split a purchase into four interest-free payments over six weeks

- Shoppers who prefer using a bank account or debit card instead of a credit card

- People who are confident that they can track and meet payment dates to avoid fees

Who It Might Not Suit

- Those who can use Sezzle or another BNPL provider

- Shoppers who need higher spending limits for large purchases

- Those who are tempted by impulse buys when payments are delayed

- Anyone who wants live customer support instead of mainly self-service help

- People who prefer more flexible or extended repayment terms

Afterpay

Afterpay Snapshot

Afterpay is a short-term financing tool that allows you to break down a total purchase into weekly or monthly payments without incurring interest—if you stay on schedule. Originating in Australia, it’s now available across the U.S. with partnerships spanning clothing, electronics, travel, and more. You can use it directly at partner stores, through the Afterpay app (available in the Apple App Store and Google Play), or with the Afterpay Card added to your digital wallet for quick checkout.

What you get with Afterpay:

- Interest-free installment payments for qualifying purchases

- A quick account setup using only a soft credit check

- Options to pay with a debit card or link a checking account

- Automatic reminders to keep you on track

- Flexibility to shop online or in-store at participating retailers

The main advantage is being able to spread out the cost without traditional credit. But as with any BNPL service, late fees and spending limits can make a difference in whether it works for you.

Step-by-Step: Using Afterpay for the First Time

Getting started is easy. I downloaded the app, created an account, and linked my bank. Approval came instantly, thanks to the soft credit check. I didn’t even have to enter my Social Security number to find out my initial spending amount ($1,000).

Now, keep in mind that this amount varies from person to person. I know someone whose spending limit was just $50 when signing up. So, while Afterpay doesn’t perform hard credit checks, they do consider payment history and other financial factors when deciding how much you can borrow.

Once set up, you can shop at partner retailers or use the Afterpay Card at checkout (both in-store and online). Purchases are divided like this:

- First payment: Due at checkout — usually 25% of the total.

- Three follow-ups: Charged automatically every two weeks.

No interest is added if weekly or monthly payments are on time. Miss one, and you’ll face a flat late fee. This may seem small individually, but it can be costly if you have multiple plans.

From the app, you can:

- See upcoming charges and due dates

- Pay off balances early

- Update your payment details

- Browse promotions and higher-value items

It’s simple, but you have to manage it closely. Multiple active plans can quickly stack up when you make too many purchases outside of your “pay in full” budget.

Where Afterpay Is Accepted

Afterpay works with a lot of retailers, from clothing and beauty to electronics, furniture, travel, and more. Hotels.com, Wayfair, Shein, Amazon, Expedia, and Stubhub are just a few that you can find on the Afterpay buy now pay later app.

For stores that don’t offer it directly, you can pay with the Afterpay Card in your mobile wallet. Just add it to Apple Pay or Google Pay and use it anywhere those are accepted. The process for using this card is similar to that of other BNPL providers, particularly Sezzle (check out my Sezzle review to see how). You have to create a one payment card before checking out (read more about that below.)

Places I’ve personally spotted Afterpay in action:

- Snagging a Free People dress or a Sephora holiday gift set without paying all at once

- Upgrading to a MacBook at Best Buy or grabbing a Nintendo Switch from GameStop

- Bringing home a West Elm sofa or tackling a Home Depot kitchen makeover

- Scrolling Etsy for custom jewelry or finding rare collectibles on eBay

- Booking a weekend getaway on Expedia or splitting the cost of flights to New York on Priceline

You can divide anything using BNPL, from a $100 pair of shoes to a $1,000 sofa, into four interest-free payments if you pay on time. But again, eligibility depends on your order amount, account history, and other factors.

Breaking Down the Interest-Free Promise

So, is Afterpay truly interest-free? Yes, so long as you split it into four installments over six weeks and stay current.

Things to note:

- Late fees – Capped per order, but still costly if you miss multiple payments.

- First payment at checkout – Usually 25% upfront.

- Longer plans will cost you – You can extend repayment into longer monthly payments, but this will often include interest.

- Order limits – Based on your history, recent activity, and past payment behavior.

The biggest perk is that the total doesn’t change if you’re on time. But it’s not a license to overspend. Discipline matters.

What Happened When I Tried Afterpay

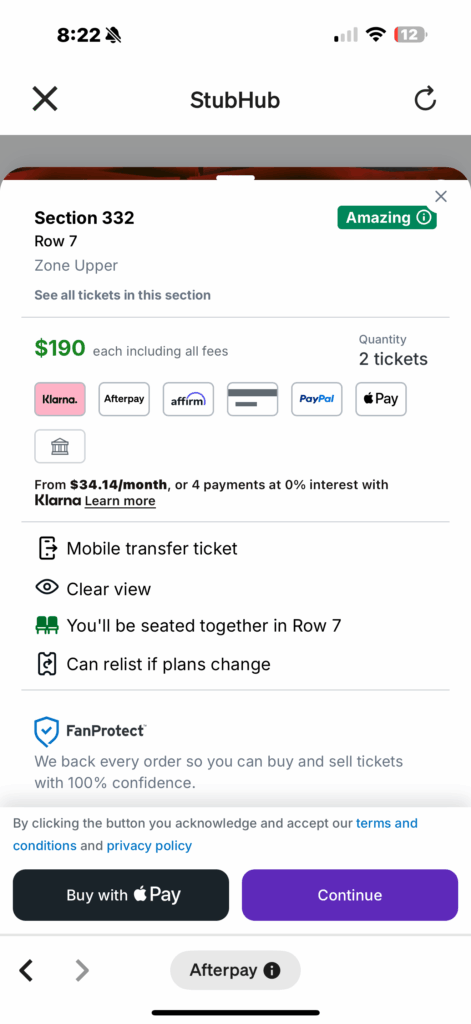

My first run with Afterpay was for something I’ve been waiting decades for — Monica and Brandy are finally touring together, and as a millennial, seeing The Boy Is Mine live is a can’t-miss bucket-list moment. The tickets were $380 total, and I wasn’t ready to drop that much at once, but a must is a must.

At checkout, I noticed an Afterpay button, but clicking it didn’t magically split my bill. Instead, it directed me to open the Afterpay app, create a one-time virtual card, and then come back to the ticket site to enter it like a regular credit card. Not a deal-breaker, but a little clunky when you’re trying to grab seats before they’re gone. The Ticketmaster countdown looming while trying to activate a one-time Afterpay card definitely had me stressed.

Once I set it up, I paid $95 upfront, followed by three more $95 payments every two weeks. The total stayed exactly the same, and I liked getting reminder notifications before each due date.

The second time I tried Afterpay, though, was a very different experience. I wanted a $500 sectional, but instead of approving me like before, I got a notice saying I needed to pay off active orders first. This was unusual, as I had never been late and my usage had always been consistent. I also had enough buying power available, so it should have been an easy purchase.

It turns out, this isn’t just me—there’s a whole Reddit thread of loyal, on-time customers suddenly being told “the system” won’t approve more purchases without explanation. The reasoning? Vague “risk assessment” talk, with no real clarity.

I could have paid down the ticket balance and tried again, but the inconsistency left a bad taste in my mouth. It’s frustrating to feel like the rules change on a whim. And judging by how many people online are dealing with the same thing, it’s not rare.

Navigating the App and Customer Support

Like Klarna and some other BNPL providers, the Afterpay app feels more like a digital shopping mall than a finance tool. The home screen is packed with store listings, promos, and trending items, all right alongside your active payment plans. It’s easy to see due dates, track past payments, and pay early, but the constant deals can make overspending far too tempting.

Do I need to take 20% off select styles with Nike? No… but Afterpay’s four installments make me feel like I do.

It’s important to mention that the Afterpay Card works with Apple Pay and Google Pay for in-store or online use. However, even when a retailer shows an Afterpay button, it often just redirects you to the app to create a one-time card, which you then have to enter at checkout like a regular credit card, not exactly seamless.

Many users report frustrations with the “Preferred Payment Date” setting. Even after turning it off multiple times, it can switch back on, moving a payment from the original schedule to an earlier day without warning. Customer service rarely changes it back, and missed payments often trigger steep spending limit cuts.

One user expressed their frustration in this thread, commenting,

“I was late less than 24 hours on one payment after having made over 20 completely on-time or early paid orders and my limit went from $1,000 to $100 immediately. I have made two orders now and paid them off trying to get it raised again and they still aren’t budging. As has been stated, they are very unforgiving.”

Support is mostly self-service via the help center, with mixed feedback on response times. Data is encrypted, and upcoming charges are clearly listed in the app, but at its core, Afterpay is built for shopping convenience, not budgeting flexibility or customer leniency.

Afterpay as a Payment Method: Pros and Cons

Upsides

- Zero-interest installments — Pay in four without extra cost if you stay on schedule.

- Bank and debit-friendly — No credit card required to use it.

- Instant approvals — Just a quick soft check, no instant score impact.

- Huge store network — Works at thousands of online and in-store retailers.

- Helpful payment alerts — Push reminders before each due date.

Downsides

- Late = fees + lower limits — Missing a payment can cost you and shrink your spending power.

- Starting caps can be low — Limits may feel restrictive until you build history.

- Shopping temptations — The app’s store promos can fuel impulse spending.

- Minimal live help — Most support is self-service, and responses can be slow.

How Afterpay Stacks Up Against Other BNPL Apps

- Sezzle – Offers interest-free plans like Afterpay but with more flexibility. Sezzle allows you to reschedule payments once per order for free, while Afterpay is less forgiving than Sezzle if you miss a due date.

Bottom Line: Choose Sezzle if you want more wiggle room on due dates — stick with Afterpay if you rarely miss a payment.

- Klarna – In addition to pay-in-four, Klarna offers financing for up to 36 months and has a wider global retailer network. Klarna’s app also includes more shopper perks like rewards points. Afterpay is more limited in both term options and extras.

Bottom Line: Klarna is better for long-term financing or earning rewards, but Afterpay keeps things simpler and interest-free for short-term purchases.

- Zip – Similar to Afterpay’s four-payment method, Zip charges a $1 fee per installment in the U.S., making it more expensive over time. Afterpay wins here by offering true no-interest financing with no per-payment fee on the purchase price.

Bottom Line: If avoiding extra fees is your priority, Afterpay comes out ahead of Zip.

Bottom Line: Is Afterpay Worth It?

Afterpay can be a real win when you just need to spread out a purchase without paying interest, whether that’s snagging concert tickets, replacing a worn-out couch, or covering a last-minute expense without maxing out a credit card. The app is straightforward, approvals are quick, and it works at thousands of online and in-store retailers.

But here’s the truth: Afterpay is built for shopping, not saving.

Yes, splitting into four payments is interest-free as long as you pay on time. Yes, the app sends reminders and makes it easy to see what’s coming up. And yes, I liked how simple it was to link my bank account and check out in-store with the Afterpay Card.

That said, Afterpay isn’t without its drawbacks. Payment schedules are fixed, so if your budget shifts unexpectedly, there’s little room to adjust without risking late fees. Missed or late payments can quickly reduce your available spending limit, and getting those limits restored isn’t always fast. While the app is designed to be simple and convenient, its strict repayment structure means it’s best suited for shoppers who are confident they can pay on time, every time.

Final Verdict: Who Should Use Afterpay

So, here’s my Afterpay verdict.

✔️ Use Afterpay if:

- You want short-term, interest-free breathing room on purchases

- You’re confident you can pay every installment on or before the due date

- You shop at Afterpay-friendly retailers and like in-app reminders

- You prefer soft credit checks that won’t ding your score

❌ Skip Afterpay if:

- You need flexibility in case of a late or skipped payment

- You already struggle to keep track of multiple due dates

- You want fast customer support

- You’re trying to curb impulse spending

Afterpay is a great “sometimes” tool, handy for planned purchases you know you can cover, but not something to lean on when money’s tight. If I can’t buy with cash, I’ll keep it in my rotation for occasional splurges I’d rather not pay in full upfront. If you treat it as a convenience, not a safety net, Afterpay is a solid option for making payments on needed (or wanted) purchases easier when you don’t have access to the funds. Just make sure you use it wisely!

FAQs

The Afterpay app is a buy now, pay later tool that lets you split purchases into four equal installments over six weeks with no interest financing. The major benefit is avoiding personal loans or high interest rates if you practice responsible spending.

Link a bank account, checking account, or debit card to your Afterpay account. At checkout (in store or shop online), your first payment (or down payment) is due, with the rest in equal installments.

For standard plans, no. Payment history isn’t sent to credit bureaus, though defaults can go to collections. Keep in mind, laws around this are changing, and you can check Afterpay on the Better Business Bureau for customer feedback.

Miss a due date, and Afterpay charges a late fee. Multiple late payments may lower your order value limit, as Afterpay considers several factors before approving new purchases.

Yes, calling Afterpay safe is accurate. The Afterpay Card works in-store, or you can shop online for everyday or big-ticket items. If you pay on time, the total cost doesn’t increase. It’s available in most states, including West Virginia and New Mexico.