About 82% of Americans travel each year, which means almost all of us have felt that “I need a getaway, but my budget says no” moment.

That’s when I turned to Affirm.

As one of the largest buy now, pay later companies in the U.S., Affirm offers financing options that go beyond short-term Pay in 4 plans. With loan terms that stretch anywhere from one month up to five years, it’s designed for larger purchases like flights, hotels, furniture, and electronics.

I’ve used Affirm for multiple trips, and while the Affirm app does make it simple to split up the cost, I’ve also seen firsthand how quickly interest can eat into your budget. Here’s what stood out to me after using it across airlines and Airbnb.

Who Should (and Shouldn’t) Use Affirm

✅ Affirm might be for you if…

- You need to spread out the cost of larger purchases like airfare, hotels, or furniture

- You want to see a clear payment plan with upfront terms before committing

- You prefer predictable monthly payments instead of juggling short-term pay-in-4 plans

❌ Affirm might not be for you if:

- You’re looking for interest-free, everyday shopping options (Sezzle or Klarna do this better)

- You’re concerned about multiple small loans cluttering your credit history

- You want extra perks like cashback, rewards, or flexible due dates

Affirm

What Is Affirm?

Affirm is a U.S.-based loan service that works like a cross between BNPL and traditional financing. Instead of offering just one type of plan, it gives you payment options that vary based on your purchase amount and credit profile.

- Short-Term: Split purchases into 3–6 monthly payments with a down payment

- Long-Term: Finance purchases up to 60 months (5 years)

- APR: Anywhere from 0% interest on promotional offers to a whopping 36% annual percentage rate

- Checkout: Select Affirm at checkout or use a virtual card in the app for online shopping or in-store purchases

You’ll need an Affirm account linked to a bank account or debit card, plus your Social Security number for the eligibility check. Affirm Holdings (the parent company) states that loans are “arranged pursuant” to partner banks, and funds are collected independently once your first payment is due.

How Affirm Works

When I signed up, Affirm asked for basic financial information—name, date of birth, phone number, and Social Security number for the eligibility check. I had to create an Affirm account and link it to my bank account or debit card before I could move forward.

Within seconds, I received an instant decision showing whether I was approved, what loan amount I qualified for, and the available payment options. Affirm Holdings (the parent company) explains that loans are “arranged pursuant” to partner banks, and the funds are collected independently once your first payment is due.

Each time you use Affirm, the system shows you different payment terms upfront, including:

- Principal amount (what you borrowed)

- Interest rate (APR)

- Total cost (principal + interest paid)

- Monthly payments and due dates

Unlike many BNPL apps, Affirm reports your payment history to credit bureaus, so paying on time may help your credit score. However, stacking multiple loans at once can also clutter your credit report and hurt you if you fall behind.

Fees, Credit, and Safety

Affirm is upfront about what you’ll pay, but the details can be easy to gloss over if you’re excited about a purchase. Here’s what you should know:

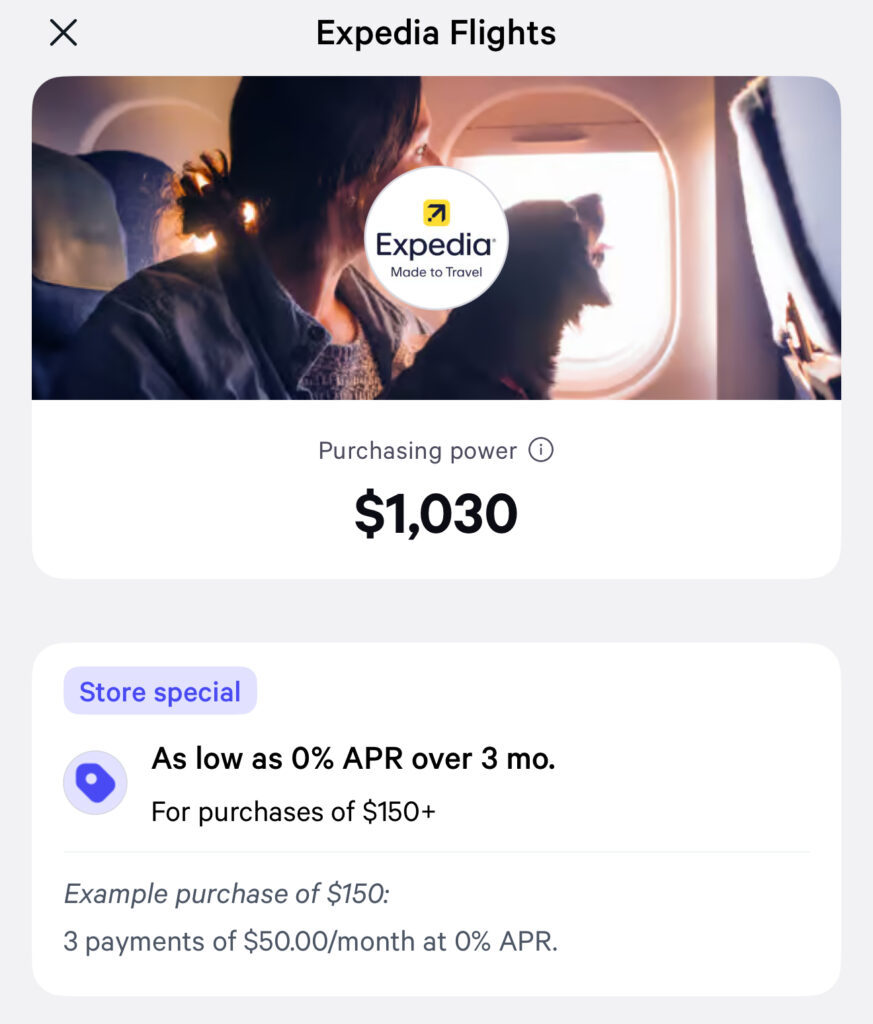

- Interest Rates: Range from 0% to 36% APR, depending on your credit profile, the merchant, and the loan amount. That $500 Airbnb I booked turned into a $530+ bill because of nearly $52 in added interest paid.

- Late Fees and Annual Fees: Affirm doesn’t charge late fees for missed payments, and there are no annual fees just to keep an account open. However, interest still accrues if you don’t pay in full, and your payment history is reported to the credit bureaus.

- Credit Reporting: Affirm now reports every loan to the three major credit bureaus. On-time payments can help your credit score, but stacking multiple loans can make your credit history look risky.

- Refunds: If a retailer cancels an order (say, Target cancelled a purchase), Affirm refunds you—but the process can take time and may depend on the store’s policies.

- Security Practices: Affirm is a Member FDIC, encrypts your financial information, and requires an eligibility check for each loan. I’ve always felt my Affirm account was safe, but the constant text messages and reminders can feel overwhelming.

In practice, the “no late fees” policy feels generous, but the high annual percentage rate (APR) often cancels out that benefit. It’s better to think of Affirm as a loan service than a flexible app like Sezzle or Klarna.

My Real-Life Experience (and Budgeting Impact) with Affirm

Using Affirm has been a mix of convenience and regret. On one hand, it gave me instant access to travel and lodging when I needed it. On the other hand, the long-term cost often made me wonder if it was worth it.

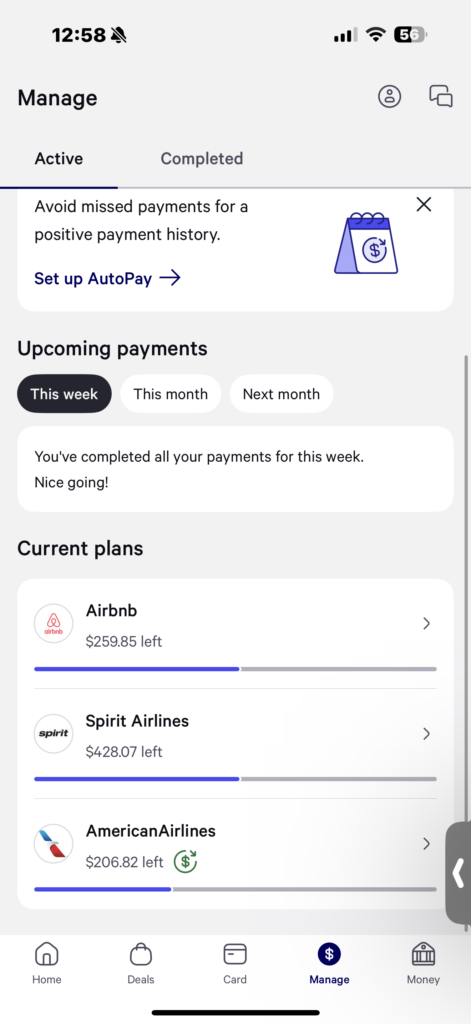

- Airbnb Staycation: I booked a $479 staycation using an Affirm virtual card. The loan came with a 35.98% APR, which added over $51 in extra charges. By the time I finish, the total cost will be more than $530. The monthly payments of about $88 felt easy, but that extra dinner or tank of gas I could have bought with the interest paid makes me question if it was worth financing.

- Spirit Airlines Flights: Affirm made it possible to book flights without feeling the full impact upfront. The monthly payments were manageable, but every time I logged into the app, I was reminded of the growing list of balances. Not every buy now, pay later option was interest-free, and that added weight over time.

- Purchasing Power Drop: At one point, my available borrowing amount dropped from $2,000 to $1,000 overnight, even though nothing major had changed in my account. That unpredictability made me hesitate to plan larger purchases through Affirm again.

In the moment, spreading out payments can feel like relief. But when you use Affirm for multiple loans at once, the balances stack quickly. What looks affordable month to month often turns into a larger financial burden, with little to show for the added cost.

Pros

- Flexible buy now, pay later payment options from 1 to 60 months

- Works well for larger purchases like travel and electronics

- No late fees for missed or late payments

- Prequalification with a soft inquiry (doesn’t affect your credit score)

- Terms are shown upfront before you commit

Cons

- Interest rates can reach 36% APR—higher than some credit cards

- Small purchases can cost significantly more over time (thanks to near-compound interest)

- Frequent credit adjustments make limits unreliable

- Every loan is reported, which can clutter your credit history

Tips for Using Affirm Wisely

If you’re going to use Affirm, here’s what I’d recommend from personal experience:

- Reserve it for big-ticket items only. Travel, furniture, or major electronics might make sense. Don’t waste Affirm on everyday purchases like clothes or groceries.

- Always calculate the total cost. Don’t just look at the monthly breakdown. If your loan amount comes with a high APR, figure out how much more you’ll actually pay before committing.

- Track multiple loans carefully. The app keeps everything in one place, but it’s still easy to forget that you’ve got three active balances at once.

- Pay early if possible. Since there are no penalties for early payoff, you can reduce the total interest paid by closing out the loan ahead of schedule.

- Don’t mistake “purchasing power” for free money. It’s easy to overspend when you see a $2,000 limit sitting there. Treat it with the same caution you’d give a credit card.

Affirm Review vs. the BNPL Competition

Affirm vs. Sezzle

Sezzle is better for everyday shopping—short, simple, interest-free payments and even options to adjust your due date. It’s a great tool for budgeting small purchases, but not ideal for financing something major. Affirm feels more like a structured loan service, giving you longer terms and higher limits for larger purchases like travel or furniture.

Winner: For everyday flexibility, Sezzle wins; for big-ticket items, Affirm takes the lead.

Affirm vs. Klarna

Klarna offers more perks, like cashback, loyalty features, and flexible cards, but it also encourages impulse spending with its mall-like app layout. Affirm doesn’t have the same rewards or shopping experience, but it’s steadier for larger purchases where you need a clear payment plan. The drawback is Affirm’s high interest rates—but for someone trying to avoid distractions and stick to essential purchases, Affirm may still be safer than Klarna.

Winner: Klarna is better for perks and shopping variety, but Affirm is the stronger choice for larger, essential purchases.

Affirm vs. Afterpay

Afterpay is straightforward, easy to track, and sticks to simple Pay in 4 plans. Affirm, on the other hand, is more complex, offering long-term loans and multiple payment options. If you want simplicity and a fast payoff, Afterpay is easier. But if you need breathing room for a $1,000+ purchase, Affirm is the stronger choice.

Winner: Afterpay wins for simplicity, but Affirm is better for financing major expenses.

Affirm vs. Zip

Zip charges flat fees (usually $1 per payment), which can make sense for smaller purchases. It also works in more places globally. Affirm’s strength is in its transparency—you see your loan amount, APR, and total cost upfront. While Zip may be cheaper on tiny purchases, Affirm is a better fit for financing larger items where fee stacking can add up.

Winner: Zip is fine for small purchases, but Affirm wins for larger loans with clear terms.

Affirm vs. Splitit

Splitit is unique because it doesn’t issue new loans—it simply breaks a purchase into installments using your existing credit card line. That means no new credit inquiries and no clutter on your credit history. But the catch is that you have to already have a credit card with enough available limit, and you’ll still pay interest if your card carries a balance. Affirm doesn’t require a card and gives you instant access to a loan amount.

Winner: Splitit works if you have strong credit cards, but Affirm is the more accessible option for most shoppers.

Affirm vs. Credova

Credova focuses more on niche markets, like outdoor gear and firearms financing, and often uses third-party lenders to arrange loans. While it does offer monthly payments, Credova has been criticized for unclear fees and inconsistent customer service. Affirm is more widely accepted, easier to manage through its app, and transparent about interest rates and payment terms.

Winner: Credova may suit niche shoppers, but Affirm is the more reliable, mainstream choice.

Is Affirm Worth It?

For me, Affirm has been a lifesaver in moments when I needed to pay over time for travel or a staycation. The ability to split costs into predictable monthly payments with a small down payment but without hidden fees is helpful, but the interest rates can be brutal.

✔️ Use Affirm if:

- You need financing for larger purchases like flights, hotels, or furniture

- You want transparent loan terms with no surprise hidden fees, and you can pay interest

- You’re confident you can use this buy now, pay later responsibly and on time

❌ Skip Affirm if:

- You’re trying to keep your credit history clean

- You don’t want your payment history cluttered with small loans

- You’re looking for perks or rewards beyond just financing on a payment plan

- You’re trying to avoid high interest paid on everyday purchases

Bottom Line

Affirm works best as a “sometimes” tool—a way to finance a trip or a large purchase without immediate sticker shock. But with APR that can rival credit cards and a tendency to shrink your credit overnight, it’s not something I’d rely on regularly.

FAQs

Yes. Some promotional plans are 0%, but most have Affirm loans with APRs between 10% and 36%.

No. Affirm does not charge fees for missed or late payments, which is one of the pros of using these kinds of BNPL services instead of traditional loans.

Yes. Your payment history is reported, which can impact your credit score.

Yes. Paying off your Affirm loan amount early can reduce the total interest paid.

Yes. Affirm is a regulated loan service that uses strict security practices and is a Member FDIC.

At checkout with thousands of retailers, in-store with select partners, and for online shopping using an Affirm virtual card or the buy now, pay later option.