I’ve used plenty of buy now, pay later apps before, but I wanted to see if the Affirm Card could make everyday purchases and larger expenses easier to manage. Unlike a traditional credit card, this one is a hybrid debit card that connects directly to your bank account. You can pay in full right away or split eligible purchases into payment plans directly in the Affirm app.

In simple terms, it’s a debit card that lets you swipe and then decide whether to pay now or split the cost later in the app.

When I first tried it, it worked just like any other card purchase. But what sets it apart is the option to turn that payment into installment payments after the fact. That kind of flexibility is useful, but it comes with some tradeoffs. That’s why I decided to dig deeper and put together this Affirm Card review, to see if this hybrid really makes sense for everyday purchases, larger purchases, and long-term personal finance goals.

Who is the Affirm Card For?

Best for:

- Disciplined spenders who want to build credit history through on-time payments

- Shoppers making larger purchases who want to see the total costs upfront

- People comfortable managing their payment history carefully since it’s reported to credit bureaus

Not great for:

- Casual BNPL users who want flexibility to reschedule payments (Sezzle is better for that)

- Shoppers who don’t want every transaction tied to their credit profile

- Anyone looking for rewards, perks, or extras beyond basic financing

How the Affirm Card Actually Works

When I first got the Affirm Card, I wondered the same thing most people do: If it’s linked to my bank account, how is this any different from a regular debit card?

Here’s the difference:

- Step 1: Use it like any debit card. You can swipe it in-store or online anywhere Visa is accepted. The money doesn’t instantly leave your bank account. Instead, the charge shows up in your Affirm app.

- Step 2: Decide how to pay. You have two options—either pay the full amount right away (like a normal debit card) or request to turn it into a payment plan. You can do this before checkout or within about 24 hours after the purchase.

- Step 3: Pick your plan. If your purchase qualifies, you can split it into four installment payments or longer monthly payments. Some are interest-free, while others have a disclosed APR.

- Step 4: Watch the fine print. Most plans require a down payment (the first payment at checkout), and other fees may pop up.

That flexibility is what makes it a hybrid between a debit card and a financing tool. You’re not locked into debt unless you choose to be—but you do take on the responsibility of managing your payment history carefully, since Affirm reports every loan.

Eligibility & Approval

Getting an Affirm Card to spend money requires a few things, including the following:

- An Affirm account in good standing

- Passing eligibility checks (done through a soft inquiry, not a hard pull)

- Being 18+, U.S. residency (not in territories)

- Linking a bank account for payments

Unlike some BNPL apps, Affirm sets your purchasing power based on factors like creditworthiness, payment history, and the loan amount you request. They also give you different payment plans to choose from, so you can decide whether to prioritize lower interest or lower monthly payments.

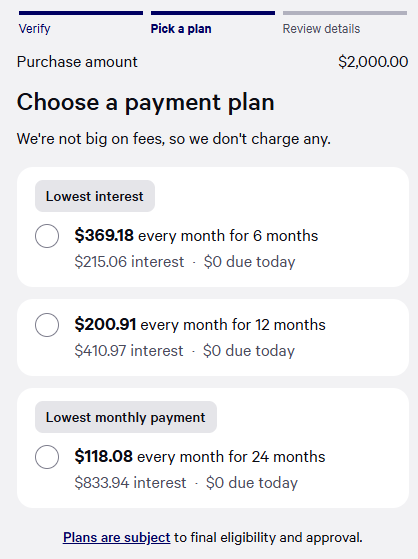

For example, I’m getting ready to take my family to Mexico, and these were my real Affirm Card options for booking flights at $2,000:

- 6 months: $369.18 per month, with $215 in interest.

- 12 months: $200.91 per month, with $410 in interest.

- 24 months: $118.08 per month, with $833 in interest.

I don’t have perfect credit, but because I’ve built a great track record with Affirm, they recently lifted my buying power. That’s one thing I appreciate—responsible use actually expands your limit.

But here’s the catch: can you imagine paying over $800 in interest for flights that only cost $2,000? By the time the trip is paid off, your total would be closer to $2,833—more than a 40% markup. That’s why choosing the right payment plan matters. Shorter terms cost more each month, but they save you a significant amount of money overall.

Affirm Review: Credit Impact

Here’s the catch: Affirm now reports all loan activity to the credit bureaus.

- On-time payments help your credit history.

- Late payments can affect your credit score and lower your purchasing power.

- Every Affirm loan made through the card shows up on your credit report.

Every Affirm Card purchase that is connected to a play is reported, meaning your payment history—good or bad—affects your credit score. On-time payments may help your credit history, while late payments can hurt it. Keep in mind that laws are changing, and soon all BNPL providers may be required to report. For now, Affirm does it automatically. With other BNPLs like Sezzle, you have the choice to opt into reporting (through Sezzle Up). With Affirm, there’s no opt-out—which means this card needs to be managed carefully if you don’t want to risk negative marks.

So how much will using the card actually cost you?

Fees, Interest & Costs

The Affirm Card does a good job of being transparent about costs, but there are still things to watch for:

- Annual fees: None

- Balance transfers: Not offered

- Overdraft fees: None from Affirm, but your bank may charge if funds are short

- Late fees: Possible, depending on your payment plan

- Interest rates: Only apply to longer monthly payments; shown before checkout

- Hidden fees: Not really—but your total cost can grow if you accrue interest on big purchases

App & Card Experience

I found the Affirm app fairly user-friendly, especially when paired with the Affirm Card. You can:

- View your online account and account details

- Check your payment date and future payments

- Receive text messages about due dates

- See your purchasing power for eligible purchases through Affirm Pay

I liked that I could easily track the total cost of a plan, something traditional credit card statements often hide with fees and interest. Using the card through the app made it simple to turn everyday purchases into installment payments and see exactly what I owed.

That said, I did find the app a little pushy toward longer Affirm loan services. By comparison, Sezzle feels more like a personal finance tool, while Affirm leans more toward a financing platform. It was also a little strange to have to plan a purchase by store ahead of time.

Affirm Card vs Sezzle, Klarna & Zip

Here’s how Affirm stacks up against other BNPL cards and services:

| Feature | Affirm Card | Sezzle | Klarna | Zip Visa |

|---|---|---|---|---|

| Type | Physical debit card + BNPL | Virtual card + app | Virtual card + app | Visa debit (digital/physical) |

| Payment Plans | Pay in full or installment payments | 4 interest-free payments | 4 payments or longer financing | Pay-in-Four, Zip Pay/Plus options |

| Interest | Sometimes (pay interest on longer plans) | Interest-free if on time and paid in four | Longer plans may charge interest | Short-term usually interest-free, but some plans have interest rates |

| Credit Reporting | Reports all activity to a credit bureau | Optional with Sezzle Up | Varies; longer loans may report | Limited; varies by product |

| Rescheduling | 1 free reschedule per order with Sezzle UP1 free reschedule per order with Sezzle UP | Some flexibility | Limited/unclear | |

| In-Store Use | Anywhere Visa accepted | Via wallet/app | Via wallet/app | Works in-store, Apple/Google Pay |

| Best For | Bigger purchases & credit builders (if managed well) | Budgeting & flexible buy now pay later | Longer financing on larger purchases | Every day use with wallet integration |

Pros & Cons of the Affirm Card

Like any buy now, pay later product, the Affirm Card has strengths and trade-offs. I’ve found it works well as a hybrid between a debit card and a financing tool, but it isn’t as flexible as some alternatives like Sezzle. Here’s what stood out the most when I used it:

Pros

- Works anywhere Visa is accepted

- Clear APR disclosure, no hidden fees

- No annual fees

- Can build credit history through on-time payment history

- Combines debit card use with BNPL options

Cons

- Reports all activity to credit bureaus (no opt-out)

- Can affect your credit score if you slip up

- No rescheduling like Sezzle

- Late fees and overdraft fees are possible

- Pushes more into long-term, Affirm loan services

Is the Affirm Card Worth It? What Users Say

Whether the Affirm Card is “worth it” depends on how—and how often—you use it. I came across a Reddit thread asking this exact question, and the responses were all over the place:

Positive Experiences:

- “I’ve used mine a bunch. Mostly at Costco but yea, I def think it’s worth it. I’ve got an Affirm card, a ZIP card I’ve never used, and I just got the Klarna credit card a couple of months ago, but haven’t used it yet either. The Klarna card is the best, tho. You don’t have to plan a purchase, just swipe it and then you have 24hrs to choose your terms or pay in full.” –u/No_Light7076

- Another user added: “Yes worth it.” – u/Silent-Orchid-1135

Negative Experiences:

- “I’ve had the Affirm physical card for years and never used it. I tried to use it twice this year, once for concert tickets and once for a hotel reservation, and both times were a nightmare. I personally don’t find any use for the card.” –u/Mavfan4114

- One commenter was even more skeptical: “Just wait until they remove your buying power and want your biometrics to restore it. 🤣🤣🔥” – u/Wrong-Ad-964

Mixed or Situational:

- “I got one even though I thought it was pointless, and it sat unused in my wallet for over a year. Then my husband hit a raccoon, and I was able to cover the insurance deductible for the repairs by setting up a plan and using the physical card. Before that, I would have said it wasn’t worth it. Now, well, you never know what emergency might pop up.” – u/RepresentativeEmu335

- Others mentioned frustration with how plans work: “Only thing I hate about Affirm card—virtual and real—is unless my bank is linked, I can’t just swipe it and then choose a plan. Have to see how much my total is and then request a plan.” –u/Expensive_Bike_8828

The takeaway: some users love the convenience and “just in case” flexibility, while others find it unnecessary, clunky, or restrictive. It really comes down to whether you need a physical card for everyday use or if the virtual option inside the Affirm app already covers your bases.

Final Verdict

The Affirm Card is a strong payment solution if you want the flexibility of a debit card that doubles as a buy-now, pay-later tool. It’s great for larger purchases where you want to see your total cost upfront and avoid compound interest.

But because every card purchase (loan) is tied to your credit report, it comes with more responsibility than Sezzle or even Klarna. If you want something that builds credit history while offering flexible installment payments, this might be a fit—as long as you stay disciplined.

If you prefer more breathing room with rescheduling, or you don’t want every loan amount reported to the bureaus, Sezzle may be the smarter choice.

FAQs

No. The card has no annual fees, balance transfer fees, or hidden charges.

Yes. Every loan through the Affirm Card is reported to the credit bureaus. On-time payments can build credit history, while late payments may hurt your score.

Yes. It’s a physical card that works anywhere Visa is accepted, including gas stations, grocery stores, and online retail purchases.

Not always. Short-term pay-in-four plans can be interest-free, while longer monthly payments may charge interest. Affirm shows you the annual percentage rate (APR) before you commit.

Missed payments may trigger late fees, reduce your purchasing power, and show up on your credit report. If your linked bank account doesn’t have funds, you could also face overdraft fees from your bank.